The Treasury Secretary nominee was being “grilled” by Congress today. I want to talk a bit about this hearing because it brings up the subject of the housing crisis. The who and the whys.

First, Mnuchin is a Wall Street guy. Even worse, he’s a hedge fund and Goldman Sachs guy. That’s like blood in the water for the sharks in Congress. They get to put on a show with live TV cameras in the room, publicly showing disgust for Mnuchin (and those like him), to cozy up the less informed segment of the country. And they get to project the blame for many things in life on the rich and their “bottom-line” business world.

This is a stark contrast to a decade ago. The media, especially, was in the business of making guys like this out to be super heroes. They wrote about them as mythical creatures – the world’s gene pool winners: the best and the brightest.

But times have changed.

In the hearing today, Mnuchin was accused of everything from tax evasion to unfairly kicking an 80-year old woman out of her house in Florida. Sounds like a really bad guy.

Though it appears that he had IRS compliant offshore accounts (not tax evasion, but tax compliant). And his company had purchased defaulted mortgages, claimed the collateral (the house) and sold the collateral for a profit.

So, just as you and me may take a tax deduction for our children, and just as an individual may sell his/her house for a profit, perhaps Mnuchin made rational financial decisions and followed the laws that were created by Congress.

So if we can’t blame Mnuchin and Goldman Sachs for nearly blowing up the global economy, who can we blame.

With all of the complexities of the housing bubble and the subsequent global financial crisis, it can seem like a web of deceit. But it all boils down to one simple actor. It wasn’t Wall Street. It wasn’t hedge funds. It wasn’t mortgage brokers. These entities were operating, in large part, from the natural force of economics: incentives.

It wasn’t even the government’s initiative to promote home ownership that led to the proliferation of mortgages being given to those that couldn’t afford them.

So who was the culprit?

It was the ratings agencies.

Housing prices were driven sky high by the availability of mortgages. Mortgages were made easily available because the demand to invest in mortgages, to fund those mortgages, was sky high.

But what drove that demand to such high levels?

When the mortgages were combined together in a package (securitized as a mix of good mortgages, and a lot of bad/higher yielding mortgages), they were bought, hand over fist, by the massive multi-trillion dollar pension industry, banks and insurance companies. Yes, the guys that are managing your pension funds, deposit accounts and insurance policies were gobbling up these mortgage securities as fast as they could, but ONLY because the ratings agencies were stamping them all with a top AAA rating. Who would encourage such a thing? Congress. In 1984 they passed a law making it okay for banks, pension funds and insurance companies to buy/treat high rated secondary mortgages like they would U.S. Treasuries.

So as investment managers, in the business of building the best performing risk-adjusted portfolio possible, and in direct competition with their peers, they couldn’t afford NOT to buy these securities. They came with the safest ratings, and with juicy returns. If you don’t buy these, you’re fired.

To put it all very simply, if these securities were not AAA rated, the pension funds would not have touched them (certainly not to the extent).

With that, if the there’s no appetite to fund the mortgages, the ultra-easy lending practices never happen, and housing prices never skyrocket on unwarranted and unsustainable demand. The housing bubble doesn’t build, doesn’t bust, and the financial crisis doesn’t happen.

That begs the question: Why did the ratings agencies give a top rating to a security that should have received a lower rating, if not much lower?

First, it’s important to understand that the ratings agencies get paid on the products they rate BY the institutions that create them. That’s right. That’s their revenue model. And only a group of these agencies are endorsed by the government, so that, in many cases, regulatory compliance on a financial product requires a rating from one of these endorsed agencies.

So as I watched the grilling session of Mnuchin today by Congress, these are the things that crossed my mind.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

This morning we got a report that small business optimism hit the highest level since 2004, on the biggest jump since 1980. This follows a big jump in December, which obviously follows the November elections.

Small business owners that have survived the storm over the past nine years, most likely have had credit lines pulled, demand for their products and services crushed, and have slashed their workforce. If they were able to piece it together to continue on, they’ve operated as lean as possible, and they’ve slowly seen it all recover. And finally, over the past couple of years, they’ve likely had banks calling offering them money again. But, given the scars of the financial crisis, taking on debt again (or more debt) in an uncertain world, many have turned it down.

But if you’re going to dip a toe in the water again, take on some risk to grow your business (to expand, to hire, to build inventories), small business owners are saying now is the time. They are buying into what the Trump agenda is promising–a “dynamic booming economy.”

You can see that reflected in this chart…

The survey shows that 50% of small business owners expect the economy to improve. That’s the most in 15 years. With that, they think it’s a good time to expand. And they expect higher sales coming down the pike, so they’ve been building inventories.

As we know, in the recovery that was manufactured by the Fed (and other central banks), Main Street didn’t participate–trillions of dollars spent and little impact on the real economy. But this survey shows that the Trump effect is already doing what nine years, and trillions of dollars of monetary stimulus and intervention, couldn’t do. Most of the small business sentiment data has now returned to pre-crisis levels, just on the pent up demand that has been unleashed by the prospects of a return to prosperity.

This number tends to correlate highly with consumer confidence numbers. Consumer confidence numbers drive consumption. And consumption contributes about two-thirds of GDP. By restoring confidence, the Trump effect on growth can be self-fulfilling.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Over the past year we’ve had a wild ride in global yields. Today I want to take a look at the dramatic swing in yields and talk about what it means for the inflation picture, and the Fed’s stance on rates.

When oil prices made the final leg lower early last year, the Japanese central bank responded to the growing deflationary forces with a surprise cut of their benchmark interest rate into negative territory.

That began the global yield slide. By mid-year, more than $12 trillion dollars with of government bond yields across the world had a negative interest rate. Even Janet Yellen didn’t close the door to the possibility of adopting NIRP (negative interest rate policies).

So investors were paying the government for the privilege of loaning it their money. You only do that when 1) you think interest rates will go even further negative, and/or 2) you think paying to park your money is the safest option available.

And when you’re a central banker, you go negative to force people out of savings. But when people think the world is dangerous and prices will keep falling, they tend to hold tight to their money, from the fear a destabilized world.

But this whole dynamic was very quickly flipped on its head with the election of a new U.S. President, entering with what many deem to be inflationary policies. But as you can see in the chart below, the U.S. inflation rate had already been recovering, and since November is now nudging closer to the Fed’s target of 2%.

Still, the expectations of much hotter U.S. inflation are probably over done. Why? Given the divergent monetary policies between the U.S. and the rest of the world, capital has continued to flow into the dollar (if not accelerated). That suppresses inflation. And that should keep the Fed in the sweet spot, with slow rate hikes.

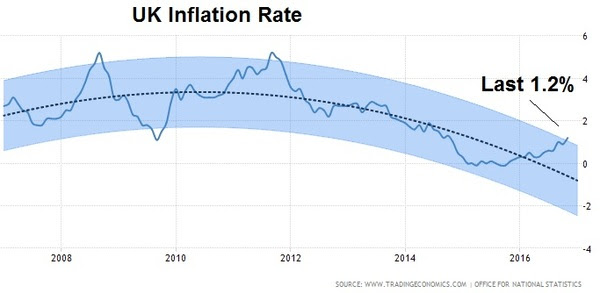

Meanwhile, there’s more than enough room for inflation to run in other developed economies. You can see in Europe, inflation is now back above 1% for the first time in three years. That, too, is in large part because of its currency. In this case, a stronger dollar has meant a weaker euro. This (along with the UK and Japan) is where the real REflation trade is taking place. And it’s where it’s needed most, because it also means growth is coming with it, finally.

You can see, following Brexit, the chart looks similar in the UK – prices are coming back, again fueled by a sharp decline in the pound, which pumps up exports for the economy.

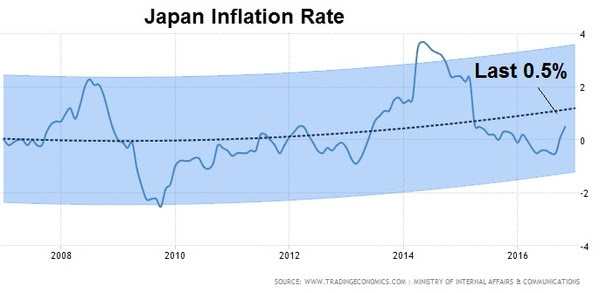

And, here’s Japan.

Japan’s deflation fight is the most noteworthy, following the administrations 2013 all-out assault to beat 2 decades of deflation. It hasn’t worked, but now, post-Trump, the stars may be aligning for a sharp recovery.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

With the Dow within a fraction of 20,000 today, and with the first week of 2017 in the books, I want to revisit my analysis from last month on why stocks are still cheap.

Despite what the media may tell you, the number 20,000 means very little. In fact, it’s amusing to watch interviewers constantly probe the experts on TV to get an anwer on why 20,000 for the Dow is meaningful. They demand an answer and they tend to get them when the lights and a camera are locked in on the interviewee.

Remember, if we step back and detach from the emotions of market chatter, speculation and perception, there are simple and objective reasons to believe the broader stock market can go much higher from current levels.

I want to walk through these reasons again for the new year.

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 49% by the middle of next year. We’re still making up for the lost growth of the past decade.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year.

Reason #3: We now have a clear, indisputable earnings catalyst to add to that story. The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 38% higher.

Reason #4: What else is not factored into all of this simple analysis, nor the models of economists and Wall Street strategists? The prospects of a return of ‘animal spirits.’ This economic turbocharger has been dead for the past decade. The world has been deleveraging.

Reason #5: As billionaire Ray Dalio suggested, there is a clear shift in the environment, post President-elect Trump. The billionaire investor has determined the election to be a seminal moment. With that in mind, the most thorough study on historical debt crises (by Reinhardt and Rogoff) shows that the deleveraging of a credit bubble takes about as long as it took to build. They reckon the global credit bubble took about ten years to build. The top in housing was 2006. That means we’ve cleared ten years of deleveraging. That would argue that Trumponomics could be coming at the perfect time to amplify growth in a world that was already structurally turning. A pop in growth, means a pop in corporate earnings–and positive earnings surprises is a recipe for higher stock prices.

For these five simple reasons, even at Dow 20,000, stocks look extraordinarily cheap.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

We talked yesterday about the bad start for global markets in 2016. It was led by China. Today, it was a move in the Chinese currency that slowed the momentum in markets. Yields have fallen back. The dollar slid. And stocks took a breather.

China’s currency is a big deal to everyone. It’s the centerpiece of the tariff threats that have been levied from the U.S. President-elect. I’ve talked quite a bit about that posturing (you can see it again here: Why Trump’s Tough Talk On China May Work).

As we know, China, itself, sets the value of its currency every day. It’s called a managed float. They determine the value. And for the past two years, they’ve been walking it lower — weakening the yuan against the dollar. That’s an about face to the trend of the prior nine years. In 2005, in agreement with their major trading partners (primarily the U.S.), they began slowly appreciating their currency, in an effort to allay trade tensions, and threats of trade sanctions (tariffs).

So what happened today? The Chinese revalued its currency — pegged ithigher by a little more than a percent against the dollar. That doesn’t sound like a lot, but as you can see in the chart, it’s a big move, relative to the average daily volatility. That became big news and stoked a little bit of concern in markets, mostly because China was the sore spot at the open of last year, and the PBOC made a similar move around this time, when global marketswere spiraling.

Why did they do it? This time around, the Chinese have complained about the threat of capital flowing out of the country – it’s a huge threat to their economy in its current form. That’s where they’ve laid the blame, on the two year slide in the value of the yuan. With that, they’ve allegedly been fighting to keep the yuan stable and have been stepping up restrictions on money leaving the country. Today’s move, which included a spike in the overnight yuan borrowing rate, was a way to crush speculators that have been betting against the currency, putting further downward pressure on the currency. But it also likely Trump related – the beginning of a crawl higher in the currency as we head toward the inauguration of the new President Trump. It’s very typical for those under the gun for currency manipulation to make concessions before they meet with trade partners.

So, should we be concerned about the move today in China? No. It’s not another January 2016 moment. But the move did drive profit taking in twobig trends of the past two months: the dollar and U.S. Treasuries. With that, the first jobs report of the year comes tomorrow. It should provide more evidence that the Fed will hike a few times this year. And that should restore the climb in the dollar and in rates.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Remember this time last year? The markets opened with a nosedive in Chinese stocks. By the time New York came in for trading, China was already down 7% and trading had been halted. That started, what turned out to be, the worst opening stretch of a New Year in the history of the U.S. stock market.

The sirens were sounding and people were gripping for what they thought was going to be a disastrous year. And then, later that month, oil slid from the mid $30s to the mid $20s and finally people began to realize it wasn’t China they should be worried about, it was oil. The oil price crash was a ticking time bomb, about to unleash mass bankruptcies on the energy industry and threaten a “round two” of global financial crisis.

What happened? Central banks stepped in. On February 11th, the Bank of Japan intervened in the currency markets, buying dollars/selling yen. What did they do with those dollars? They must have bought oil, in one form or another. Oil bottomed that day. China soon followed with a move to boost bank lending, relieving some fears of a global liquidity crunch. The ECB upped its QE program and cut rates. And then the Fed followed up by taking two of their projected four rate hikes off of the table (of which they ended up moving just once on the year).

What a difference a year makes.

There’s a clear shift in the environment, away from a world on liquidity-driven life support/ and toward structural, growth-oriented change.

With that, there’s a growing sense of optimism in the air that we haven’t seenin ten years. Even many of the pros that have constantly been waiting for the next “shoe to drop” (for years) have gone quiet.

Global markets have started the year behaving very well. And despite the near tripling from the 2009 bottom in the stock market, money is just in the early stages of moving out of bonds and cash, and back into stocks. Following the election in November, we are coming into the year with TWO consecutive record monthly inflows into the U.S. stock market based on ETF flows from November and December.

The tone has been set by U.S. markets, and we should see the rest of the world start to play catch up (including emerging markets). But this development was already underway before the election.

Remember, I talked about European stocks quite a bit back in October. While U.S. stocks have soared to new record highs, German stocks have lagged dramatically and have offered one of the more compelling opportunities.

Here’s the chart we looked at back in October, where I said “after being down more than 20% earlier this year, German stocks are within 1.5% of turning green on the year, and technically breaking to the upside“…

And here’s the latest chart…

You can see, as you look to the far right of the chart, it’s been on a tear. Adding fuel to that fire, the eurozone economic data is beginning to show signs that a big bounce may be coming. A pop in U.S. growth would only bolster that.

And a big bounce back in euro zone growth this year would be a very valuabledefense against another populist backlash against the establishment (first Grexit, then Brexit, then Trump). Nationalist movements in Germany and France are huge threats to the EU and euro (the common currency). Another round of potential break-up of the euro would be destabilizing for the global economy.

With that, as we enter the year with the ammunition to end the decade long economy rut, there are still hurdles to overcome. Along with Trump/China frictions, the French and German elections are the other clear and present dangers ahead that could dull the efficacy of Trumponomics.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Happy New Year! We’re off to what will be a very exciting year for markets and the economy. And make no mistake, there will be profound differences in the world this year, with the inauguration of a new, pro-growth U.S. President, at a time where the world desperately needs growth.

I’ve talked a lot about the “Trump effect.” Clearly, when you come in slashing the corporate tax rate, creating incentives for trillions of dollars of capital to come home, and eliminating overhead and hurdles associated with regulation, you’ll get hiring, you’ll get spending, you’ll get investment and you’ll get growth.

But there’s more to it. Ray Dalio, one of the richest, best and brightest investors in the world has said, there is a clear shift in the environment, “from one that makes profit makers villains with limited power, to one that makes them heroes with significant power.”

The latter has been diminished over the past 10 years.

Clearly, we entered the past decade in an economic and structural mess. But while monetary policy makers were doing everything in their power (and then some) to avert the apocalypse and, later, fuel a recovery, it was being undone by law makers and a lack of fiscal support, swinging the pendulum too far in the direction of punishment and scapegoating.

With that, despite the continued wealth creation of the 1% over the past decade, and the widening of the inequality gap, the power of the wealth creators has been diminished in the crisis period – certainly, the public’s favor toward the rich has diminished. And most importantly, the incentives for creating value and creating wealth have been diminished.

With all of the nuances of change that are coming, and the many opinions on what it all means, that statement by billionaire Ray Dalio might be the most simple and clear point made.

Another good point that has been made by Dalio, as he’s reflected on the “Trump effect.” It’s the element that economists and analysts can’t predict, and can’t quantify. The prospects of the return of “animal spirits.” This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mis-trust of the system.

All along the way, throughout the recovery period, and throughout a tripling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindset appears to finally be underway. And that gives way to a return of animal spirits, which haven’t been calibrated in all of the forecasts for 2017 and beyond.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Over the past two days, we’ve looked back at a couple of the six marketthemes I expected to dominate in 2016. Back in January, I said “central banks are in control, be long stocks.” That was theme number one. And I thought “China’s currency manipulation would come home to roost.” That was theme number six. Both have clearly materialized. As for China, its currency manipulation has become center stage with the incoming President Trump.

Among the six themes we discussed back in January, I also expected the dollar to continue on a big run. I said…

“The dollar is in a long term bull cycle—Be Long Dollars

When we look back at the long term cycles of the dollar over the past 40 years, we see five distinct cycles for the dollar. And these cycles have lasted, on average, about seven years. The most recent cycle is a bull cycle, started in March 2008, yet has underperformed the average of the past six cycles. While the bull cycle appears to be long–in–the–tooth, in terms of duration, the fundamentals for dollar strength have just recently swung massively in favor of the dollar. We have an historic divergence in the monetary policy path of the U.S. relative to Europe and Japan—a very rare occurrence to have the Fed going one direction (toward raising rates) and two major economic powers going the opposite direction, aggressively.

This huge monetary policy divergence dynamic creates the potential for a sharp extension in the dollar over the coming months.”

The dollar has indeed been strong, but only after a correction earlier in the year. In the past week, the dollar index has reached a 14–year high.

With the Fed projecting three hikes next year and Europe and Japan still going the opposite direction (full bore QE), the dollar trend doesn’t look like it will slow anytime soon. And despite what many are warning about what a stronger dollar might do to growth, a strong dollar tends to accompanystrong growth historically (and it doesn’t kill it). On the other hand, it should be fuel for the rest of the world, as cheaper foreign currencies give the weaker global economies a chance to export their way out of an economic rut.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio is up 24% since we started it in December. Join me here.

Dow 20,000 get’s a lot of people excited. But as we discussed on Friday, there are rational reasons to expect stocks will continue to climb to much higher levels.

Yesterday we looked back on China’s currency manipulation which has escalated to a big geopolitical risk with the incoming Trump administration. Remember, at the beginning of the year I talked about the six big global market themes for 2016. China’s currency was one.

Given that we’re reaching the 20k level in the Dow, let’s revisit the first theme I talked about back in January. “Theme #1: The central banks are in control — Be Long Stocks…

We know that the global financial and economic crisis was driven by a credit bubble and, therefore, overindebtedness. We know more than 60 countries around the world were simultaneously in recession.

If you grasp this reality (Theme #1), and are firmly rooted in the context within which the global economy is operating, respecting the role that central banks played in rescuing the world from an apocalyptic collapse, then there hasn’t been much more to talk about or to debate for quite some time, when it comes to the outlook for markets, risks, scenarios, etc. Central Banks have proven to be able to influence confidence and asset prices. Both of which are critical tools in creating recovery and continuing recovery.”

Now, remember, it wasn’t very long ago (as recent as last month!) that the outlook for the world was gloomy, and the bond markets were pricing in deflation forever. But up to that point, central banks had continued to supply liquidity to the world and fought off crises that threatened to derail the recovery. The central banks gave us a green light to buy stocks, especially when you consider that the Fed, the ECB and the BOJ (the three most powerful central banks in the world) wanted and needed stocks higher.

Of course, we now have a hand off. We’ve had a diver chained under water, and monetary authorities keeping the diver alive, scrambling to replenish the oxygen in the tank. And now we have broad sweeping fiscal and structural policy change coming, which cuts the diver’s chain and oxygen is just above the surface. It’s a recovery that can be driven by fundamental change, which has the chance to become a sustainable recovery. That means you can no longer evaluate the market and economic outlook with the same lens you used just a little more than a month ago.

When you get fundamental change in a stock, you can see huge revaluations. That’s precisely why activist investors have some of the best investment records in history, and have achieved some of the biggest returns overtime (like billionaire Carl Icahn, who has compounded money at nearly 30% for 50 years). They take a controlling stake in a stock. They fire bad CEOs, shake up irresponsible boards, cut costs, sell off underperforming assets — they step into deeply distressed companies and create change through their influence. And that change is the recipe for unlocking value in a stock. The outlook completely changes, so does the valuation.

The Trump administration is approaching policy like a distressed activist investor — targeting a suppressed economy and deeply depressed industries and unlocking value through change, to drive economic growth. When the fundamentals change, when the rules change, the outlook becomes completely different. Just the idea that these changes are coming makes the world a very different place than what we’ve seen for the past ten years (at the inception of the global economic crisis).

For help building a high potential portfolio following the influence of activist investors, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio is up 24% this year. You can join me here and get positioned for a big 2017.

The last big market event of the year will be Wednesday, when the Fed decides on rates.

As we’ve discussed, from the bottom in rates earlier this year, the interest rate market has had an enormous move. That has a lot of people worried about 1) a tightening that has already taken place in the credit markets, and 2) the potential drag it may have on what has been an improving recovery. But remember, we headed into the Fed’s first post-crisis rate hike, last December, with the 10 year yield trading at 2.25%.

And while rates have since done a nearly 100 basis point round trip, we’ll head into this week’s meeting with the 10 year trading around 2.50%. With that, the market has simply priced-in the rate hike this week, and importantly, is sending the message that the economy can handle it.

However, what has been the risk, going into this meeting, is the potential for the Fed to overreact on the interest rate outlook in response to the pro-growth inititiaves coming from the Trump administration. As we found last year, overly optimistic guidance from the Fed has a tightening effect in this environment. People began bracing ealier this year for a slower economy, if not a Fed induced recession, after the Fed projected four rate hikes this year.

The good news is, as we discussed last week, the two voting Fed members that were marched out in front of cameras last week, both toed the line of Yellen’s communications strategy, expressing caution and a slow and reactive path of rate hikes (no hint of a bubbling up of optimism). Again, that should keep the equities train moving in the positive direction through the year end.

In fact, both equities and oil look poised to take advantage of thin holiday markets. We may see a few more percentage points added to stocks before New Years, especially given the catalyst of the Trump tweet. And we may very well see a drift up to $60 in oil in a thin market.

We’ve had the first production cut from OPEC in eight years. And as of this weekend, we have an agreement by non-OPEC producers to cut oil production too. That gapped oil prices higher to open the week, and has confirmed a clean long term technical reversal pattern in oil.

This is a classic inverse head and shoulders pattern in oil. The break of the neckline today projects a move to $77. Some of the best and most informed oil traders in the world have been predicting that area for oil prices since this past summer.

Follow me and look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio is up more than 27% this year. You can join me here and get positioned for a big 2017.