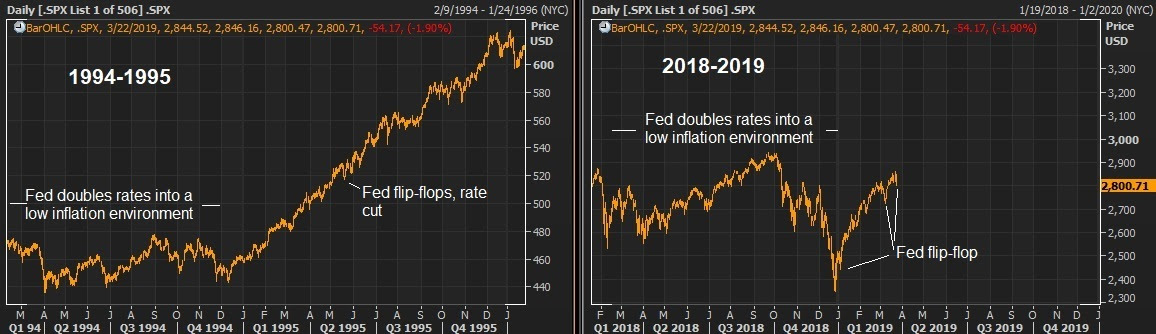

|

April 11, 5:00 pm EST As we came into the week, the economic, political and corporate calendar was relative light. With that, I suspected markets would be relatively quiet. Of course we have had an ECB meeting and minutes from the Fed. Often, these would be market moving events. Not this week. As we discussed yesterday, we clearly know where they stand. So, what’s next? Earnings. First quarter earnings season kicks off next week. We’ll hear from the major banks. Earnings will be the catalyst for where stocks go from here – and banks will set the tone. The building theme has been “earnings recession.” After 20%+ earnings growth in 2018, following a historic corporate tax cut, anyone would expect earnings growth to be less hot than last year. Some were even predicting that the hot numbers of last year would be a peak in earnings growth. After all, under ordinary circumstances (in a stable economic environment) we’re very unlikely to see the U.S. stock market grow earnings by excess of 20%. That’s not much of a story . But the media loved the shock value of the phrase “peak earnings” last year, and ran it in headlines, conveniently excluding the word “growth.” Peak earnings is very different than peak earnings growth. Still, the broad market sentiment on future corporate earnings eroded through the end of 2018, and has continued to erode through 2019. And both Wall Street and corporate America are more than happy to ride the coattails of lower sentiment by lowering the expectations bar on earnings. When sentiment is leaning that way already, there is little-to-no penalty for lowering the bar. That just sets the table for positive surprises. They did it for Q4 2018 earnings. And they beat expectations. And they have set the table for positive surprises for Q1 2019 earnings. Just how low has the bar been set for Q1? Before stocks unraveled in December, Wall Street was looking for 8.3% earnings growth for 2019. Now they are looking for less than half that. Moreover, they have projected earnings to contract in Q1 compared to the same period a year ago (i.e. at least a short-term peak in earnings).

Will they be right?

Well, the Atlanta Fed’s real-time model for estimating GDP has Q1 GDP coming in at 2.3%. The economy added on average 173,000 jobs a month over the first quarter. Both manufacturing and services PMIs expanded in the quarter, and stocks fully recovered the losses from December. That’s a formula for earnings growth, no contraction.

|

|

If you haven’t signed up for my Billionaire’s Portfolio, don’t delay … we’ve just had another big exit in our portfolio, and we’ve replaced it with the favorite stock of the most revered investor in corporate America — it’s a stock with double potential. Join now and get your risk free access by signing up here. |