We’ve talked about the set up for positive surprises in the data. We’ve looked at the first two components of GDP (consumption and investment) both of which are set up for positive surprises. Today let’s look at government spending.

It’s typical for debt to balloon in economic downturns. Not only did our debt/gdp ratio balloon in the U.S. but it ballooned everywhere. With that, as the global economy was being propped up by central banks, for the better part of the past decade, the politicians were reluctant to help on the fiscal side. Instead, they went the other way. They went the path of austerity. They focused on debt when the economy desperately needed growth.

Fiscal tightening in a widespread global recession is a recipe for tipping it all into depression. That required the central banks to do more, and more, and more to keep the economy from entering into a deflation spiral — fighting the drag of fiscal belt tightening. And it all began tipping over the edge in mid-2016.

But that changed with Trump election. Trumponomics has been all about restoring growth and breaking from the rut of economic stagnation. And a key pillar in that plan has been infrastructure and government spending.

On that note, he’s been pushing for a trillion dollar infracture spend over 10 years. And as we’ve discussed, while adding debt isn’t popular for the politicians to approve, natural disasters last year gave them an excuse to approve spending packages. Fast foward just six months and we’ve had more than $200 billion in aid approved from Congress. And now we’ve had an increase of $400 billion in government spending as part of the lastest government budget.

So the government spending piece has been in motion. And expect the rest of the world to follow. As we’ve discussed in recent weeks, we’ve seen the populist push back across the world, from Grexit, to Brexit, to the Trump vote, and now to the “Italy first” movement. The real fight in the “populist movement” is against economic stagnation. And much of that is due to mistakes on policy in response to the global economic crisis. And the core mistake has been austerity. Growthsolves a lot of problems.

What about the debt?

The media loves to talk about the $20 trillion dollar debt load, as if we are going to default and/or the rest of the world is going to dump our Treasuries and send interest rates skyrocketing and implode our economy.

Government debt and deficits are judged (by global trade partners, allies, global allocators of capital) on a relative basis – size relative to GDP. Again, our debt relative to GDP has ballooned since the global financial crisis. But it also has for everyone else in the world. That’s why people/countries are still plowing money into our Treasury market for virtually no return, because lending the U.S. money is still the safest place and way to preserve wealth.

The only alternative in this post global financial crisis environment is to focus on growth. Growth can solve a lot of problems, including the debt and deficit relative to GDP problems. As growth goes up, our debt relative to size of the economy goes down.

If we get the economy back on a sustainable growth path, then, in good times, we can work on the structural flaws that led us to the crisis. That’s the only option.

So, when we look at the components of GDP, the policy execution in Washington has been driving lift-off in all of the components. And yet the experts have still underetimated the potential for a growth boom. We’ve talked about the positive surprises that are coming down the pike in consumption, investment and govenment spending. Tomorrow, we’ll take a look at the trade piece.

Stocks are sliding more aggressively today. Wall Street and the media always have a need to assign a reason when stocks move lower. There have been plenty of negatives and uncertainties over the past seven months — none of which put a dent in a very strong opening half for stocks.

But markets don’t go straight up. Trends have retracements. Bull markets have corrections. And despite what many people think, you don’t need a specific event to turn markets. Price can many times be the catalyst.

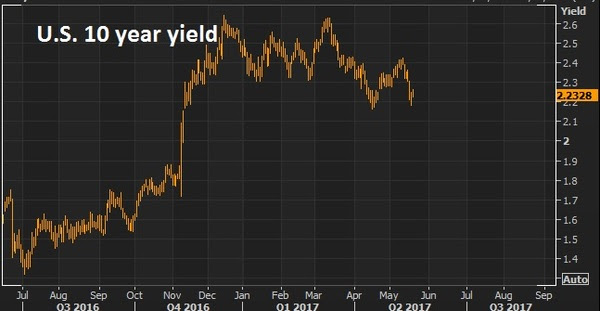

If we look across markets, it’s safe to say it doesn’t look like a market that is pricing in nuclear war. Gold is higher, but still under the highs of a month ago. The 10 year yield is 2.21%. Two weeks ago, it was 2.22%. That doesn’t look like global capital is fleeing all parts of the world to find the safest parking place.

Now, on the topic of North Korea, the media has found a new topic to obsess about– and to obsessively denounce the administration’s approach. With that, let’s take a look at the Trump geopolitical strategy of calling a spade a spade.

As we know, Mexico was the target heading into the election. Trump’s tough talk against illegal immigration and drug trafficking drew plenty of scrutiny. People feared the protectionist threats, especially the potential of alienating the U.S. from its third biggest trading partner. We’re still trading with Mexico. And the U.S. is doing better. So is Mexico. Mexican stocks are up 11% this year. The Mexican currency is up 13% this year.

China has been a target for Trump. He’s been tough on China’s currency manipulation and, hence, the lopsided trade that contributed heavily to the credit crisis. Despite all of the predictions, a trade war hasn’t erupted. In fact, China has appreciated its currency by 5% this year. That’s a huge signal of compliance. That’s among the fastest pace of currency appreciation since they abandoned the peg against the dollar more than 12 years ago (which was China’s concession to threats of a 30% trade tariff that was threatened by two senators, Schumer and Graham, back in 2005). And even in the face of a stronger currency (which drags on exports, a key driver of the economy), stocks are up 5% in China through the first seven months of the year.

Bottom line: It’s fair to say, the tough talk has been working. There has been compromise and compliance. So now Trump has stepped up the pressure on North Korea, and he has been pressuring China, to take the side of the rest of the world, and help with the North Korea situation – and through China is how the North Korea threat will likely get resolved.

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

Stocks continue to bounce back today. But the technical breakdown of the Trump Trend on Wednesday

still looks intact. As I said on Wednesday, this looks like a technical correction in stocks (even considering today’s bounce), not a fundamental crisis-driven sell-off.

With that in mind, let’s take a look at the charts on key markets as we head into the weekend.

Here’s a look at the S&P 500 chart….

For technicians, this is a classic “break-comeback” … where the previous trendline support becomes resistance. That means today’s highs were a great spot to sell against, as it bumped up against this trendline.

Very much like the chart above, the dollar had a big trend break on Wednesday, and then aggressively reversed Thursday, only to follow through on the trend break to end the week, closing on the lows.

On that note, the biggest contributor to the weakness in the dollar index, is the strength in the euro (next chart).

The euro had everything including the kitchen sink thrown at it and it still could muster a run toward parity. If it can’t go lower with an onslaught of events that kept threatening the existence of the euro, then any sign of that clearing, it will go higher. With the French elections past, and optimism that U.S. growth initiatives will spur global growth (namely recovery in Europe), then the European Central Bank’s next move will likely be toward exit of QE and extraordinary monetary policies, not going deeper. With that, the euro looks like it can go much higher. That means a lower dollar. And it means, European stocks look like, maybe, the best buy in global stocks.

A lower dollar should be good for gold. As I’ve said, if Trump policies come to fruition, inflation could get a pop. And that’s bullish for gold. If Trump policies don’t come to fruition, the U.S. and global growth looks grim, as does the post-financial crisis recovery in general. That’s bullish for gold.

This big trendline in gold continues to look like a break is coming and higher gold prices are coming.

With all of the above, the most important chart of the week is probably this one …

The 10 year yield has come all the way back to 2.20%. The best reason to wish for a technical correction in stocks, is not to buy the dip (which is a good one), but so that the pressure comes out of the interest rate market (and off of the Fed). The run in the stock market has clearly had an effect on Fed policy. And the Fed has been walking rates up to a point that could choke off the existing economic recovery momentum and, worse, neutralize the impact of any fiscal stimulus to come. Stable, low rates are key to get the full punch out of pro-growth policies, given the 10 year economic malaise we’re coming out of.Invitation to my daily readers: Join my premium service members at Billionaire’s Portfolio to hear more of my big picture analysis and get my hand-selected, diverse portfolio of the most high potential stocks.

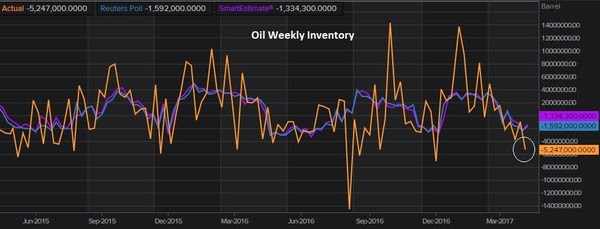

Oil has been on the move the past few days. Was this recent dip a gift to buy?The oil inventory report yesterday showed a big drawdown on oil inventories. The market expectation was for about a drawdown of 1.5 million barrels. It came in at 5 million.

That has oil on a big bounce for the week. It’s trading about 8% higher than it was at the lows of last Friday. But we still sit below the 200 day moving average and below the key $50 level (the comfort zone for those producers, namely the shale industry, to fire back up idle capacity).

The weakness in oil has a lot to do with weakness across broader commodities. And broader commodities typically correlates well with what Chinese stocks are doing.

You can see in the chart above, how closely the two track. This bottom in commodities has/had everything to do with the outlook for a big infrastructure spend out of the Trump administration. It’s yet to bubble up toward the top of the action list. With that, the momentum has either stalled on this trade, or it’s a pause before another leg higher in this early stage multi-year rebound. My bet is on the latter. Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.

Those that oppose it warn that it will lead to another financial crisis. On that note, I want to revisit my take from earlier this year on the cause of the crisis that almost destroyed the global economy.

“With all of the complexities of the housing bubble and the subsequent global financial crisis, it can seem like a web of deceit. But it all boils down to one simple actor. It wasn’t Wall Street. It wasn’t hedge funds. It wasn’t mortgage brokers. These entities were operating, in large part, from the natural force of economics: incentives.

It wasn’t even the government’s initiative to promote home ownership that led to the proliferation of mortgages being given to those that couldn’t afford them.

So who was the culprit?

It was the ratingsagencies.

Housing prices were driven sky high by the availability of mortgages. Mortgages were made easily available because the demand to invest in mortgages, to fund those mortgages, was sky high.

But what drove that demand to such high levels?

When the mortgages were combined together in a package (securitized as a mix of good mortgages, and a lot of bad/higher yielding mortgages), they were bought, hand over fist, by the massive multi-trillion dollar pension industry, banks and insurance companies. Yes, the guys that are managing your pension funds, deposit accounts and insurance policies were gobbling up these mortgage securities as fast as they could, but ONLY because the ratings agencies were stamping them all with a top AAA rating. Who would encourage such a thing? Congress. In 1984 they passed a law making it okay for banks, pension funds and insurance companies to buy/treat high rated secondary mortgages like they would U.S. Treasuries.

So as investment managers, in the business of building the best performing risk-adjusted portfolio possible, and in direct competition with their peers, they couldn’t afford NOT to buy these securities. They came with the safest ratings, and with juicy returns. If you don’t buy these, you’re fired.

To put it all very simply, if these securities were not AAA rated, the pension funds would not have touched them (certainly not to the extent). With that, if the there’s no appetite to fund the mortgages (no money chasing it), then the ultra-easy lending practices never happen, and housing prices never skyrocket on unwarranted and unsustainable demand. The housing bubble doesn’t build, doesn’t bust, and the financial crisis doesn’t happen.

That begs the question: Why did the ratings agencies give a top rating to a security that should have received a lower rating, if not much lower?

First, it’s important to understand that the ratings agencies get paid on the products they rate BY the institutions that create them. That’s right. That’s their revenue model. And only a group of these agencies are endorsed by the government, so that, in many cases, regulatory compliance on a financial product requires a rating from one of these endorsed agencies.”

Keep this in mind as the fear mongering over the talk of repeal of rework of Dodd Frank heats up.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.

The last data point for everyone to obsess about going into next week’s Fed meeting will be this Friday’s jobs report.

But as I’ve said for quite a while, the jobs data has been good enough in the Fed’s eyes for quite some time. Nonetheless, they’ve had many, many balks along the path of normalizing rates over the past couple of years. Here’s a look at a chart of the benchmark payrolls data we’ll be seeing Friday.

You can see in this chart, the twelve-month moving average is 195k. The three-month moving average is 182k. The six-month moving average is 182k. This is all fairly consistent with historical/pre-crisis levels.

So the numbers have been solid for quite some time, even meeting and exceeding the Fed’s targets, especially when it comes to the unemployment rate (4.7% last). However, when the Fed’s targets have been met, the Fed has moved the goal posts. When those goal posts were then exceeded, the Fed found new excuses to justify their decisions to avoid the path of aggressive hikes/normalization of rates that they had guided.

Among those excuses: When jobs were trending at 200k and unemployment breached 5%, the Fed started to acknowledge underemployment. Then the lack of wage growth became the focus. Then it was macro issues. To name a few: It’s been soft Chinese economic data, a Chinese currency move, Russian geopolitical tensions, collapsing oil prices, Brexit and weak productivity.

And just prior to the election last year, the Fed became, confusingly, less optimistic about the U.S. economic outlook, which was the justification to ratchet down the aggressive projected path for rates.

I suspected last year, when they did this that they were making a strategic pivot, to set expectations for a much easier path for rates, in hopes to keep people spending, borrowing and investing — instead of promoting a tighter path, which proved for the better part of two years (prior to the election) to create the opposite effect.

Remember, Bernanke (the former Fed Chair) even wrote a public piece on this last August, criticizing the Fed for being too optimistic in its projections for the path of interest rates. By showing the market/the world an expectation that rates will be dramatically higher in the coming months, quarters and years, Bernanke argued in his post that this “guidance” has had the opposite of the desired effect – it’s softened the economy.

A month later, in September, in Yellen’s post-FOMC press conference, she said this in response to why they didn’t raise rates: “the decision not to raise rates today and to wait for some further evidence that we’re continuing on this course is largely based on the judgment that we’re not seeing evidence that the economy is overheating.” Safe to argue, the economy isn’t overheating, still.

Again, as I said on Friday, the only difference between now and then, is the prospects of major fiscal stimulus, which is precisely what the Fed claims to be ignoring/leaving out of their forecasts – a believe it when I see it approach, allegedly.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

Yesterday we talked about the warning signal flashing from the German bond market. That continues today.

While global stocks and commodities are reflecting broad optimism about the new pro-growth government in the U.S., the yield on 2-year German government bonds is sending a negative message — it hit record lows yesterday, and again today — trading to negative 90 basis points. You pay almost 1% to loan the German government money for two years.

Here’s a longer term look at German yields, for perspective…

And here’s the divergence since the election between German and U.S. 2 year yields…

This divergence is partially driven by rising U.S. yields on optimism about the outlook, about inflationary policies, and about the Fed’s response. On the other hand, German yields have gone the other way because 1) the ECB is still outright buying government bonds through its QE program (bond prices go up, yields go down), and 2) capital flows into bonds, in search of safety, because a Trump win makes another populist vote in Europe more likely when the French elections role around in May.

So that bleed to new lows in the German 2-year yield sends a warning signal to global markets. Today we have a few more reasons to think this could be a signal that the optimism being priced into U.S. markets at the moment could take a breather here.

Trump’s Secretary of Treasury, Mnuchin, was doing his first rounds on financial TV this morning and gave us some guidance on a timeline for policies and impact. Most importantly, he says we’ll see limited impact from Trump policies in 2017, and that the growth impact won’t come until 2018.

Let’s consider how that can impact where the Fed stands on their forecasts for monetary policy.

Remember, they spent the better part of 2016 walking back on the promises they had made for 4 rate hikes last year. And then, when they finally moved for thefirst time this past December, following the election and a rallying stock market, they reversed course on all of the dovish talk of the past months, and re-upped on another big rate hiking plan for 2017.

Though they don’t like to admit it, we can only assume that when they considered a massive fiscal stimulus package coming, like any human would, they became more bullish on the economy and more hawkish on the inflation outlook.

So now as Mnuchin tells us not to expect a growth impact from Trump policies until next year, maybe the Fed lays off the tightening rhetoric for a while.

With all of this in mind, another interesting dynamic in markets today, the Dow shrugged off some weakness early on to trade higher most of the day, posting another new record high. Meanwhile small caps diverged, trading weaker all day. And gold traded to the highest level since November 11. Remember this chart we’ve looked at, which looks like higher gold to come (a lower purple line), and lower yields.

This would all project a calming for the inflation outlook, which would be good for the health of markets. Among the biggest risk to Trumponomics is hot inflation, too fast, and a race higher in interest rates to chase it.

To peek inside the portfolio of Trump’s key advisor, join me in our Billionaire’s Portfolio. When you do, I’ll send you my special report with all of the details on Icahn, and where he’s investing his multibillion-dollar fortune to take advantage of Trump policies. Click here to join now.

Remember, it wasn’t too long ago that the world was sitting on every word uttered by a central banker. Those days are likely over — at least to the extreme extent of the past decade. For now, Trump has supplanted central bankers as the most powerful policy maker in the world.

Still, the Fed will meet following their rate hike last month, the second in their very slow hiking cycle – 1/4 point hike twelve months apart. They’ll do nothing this week, but the data tends to be going as desired by the Fed, and other major central banks for that matter (aside from Japan) — meaning, inflation has recovered and is nearing the target zone.

Remember, this time last year, the world was staring down the barrel of DE-flation again. Inflation, central bankers have tools to combat. Deflation is far more difficult, and far less predictable. It can spiral and grind economies to a halt. When consumers are convinced prices will be cheaper in the future, they wait. When they wait, economic activity stalls. With that, deflation tends to create more deflation. The fear of that scenario, and the potential of an irreversible spiral, is why central bankers were cutting rates to negative territory last year.

Where was the imminent deflationary threat coming from? Slow economic activity, but mostly a crash in oil prices.

Central bankers have the tendency to change the rules of the game when it suits them. When inflation is running hot, they may hold off on tightening money by pointing to hot “food and energy” prices. These are temporary influences, as they say. Interestingly, they are much more aggressive, though, when oil prices are creating a deflationary threat – as they did last year.

With that, oil prices have doubled from the lows of last February. So it shouldn’t be too surprising that inflation numbers are rising, and getting close to the desired targets (around 2%) of the central bankers of the U.S., Europe and England.

So will we see a turning point for global central banks (not just the Fed) in the months ahead? The world has already been pricing in the likelihood that the pro-growth policies coming from the Trump administration will take the burden of manufacturing economic recovery off of the central banks.

But we may find that “transitory oil prices” will be the excuse for more inaction by the Fed, and continued QE from the ECB and BOE in the months ahead, which may result in a slower pace of rate hikes than both the Fed projected in December and the market has been anticipating.

Higher rates at this stage: 1) creates problems for the housing recovery, 2) promotes more capital flight from emerging markets like China (which means more dollar strength),and 3) threatens to neutralize the fiscal stimulus and reform coming down the pike for the U.S.

In December, the Fed dialed back their talk about letting the economy run hot (i.e. staying well behind the curve on inflation to make sure recovery is robust). We’ll see if they switch gears again and start explaining away the inflation numbers to oil prices.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

This morning we got a report that small business optimism hit the highest level since 2004, on the biggest jump since 1980. This follows a big jump in December, which obviously follows the November elections.

Small business owners that have survived the storm over the past nine years, most likely have had credit lines pulled, demand for their products and services crushed, and have slashed their workforce. If they were able to piece it together to continue on, they’ve operated as lean as possible, and they’ve slowly seen it all recover. And finally, over the past couple of years, they’ve likely had banks calling offering them money again. But, given the scars of the financial crisis, taking on debt again (or more debt) in an uncertain world, many have turned it down.

But if you’re going to dip a toe in the water again, take on some risk to grow your business (to expand, to hire, to build inventories), small business owners are saying now is the time. They are buying into what the Trump agenda is promising–a “dynamic booming economy.”

You can see that reflected in this chart…

The survey shows that 50% of small business owners expect the economy to improve. That’s the most in 15 years. With that, they think it’s a good time to expand. And they expect higher sales coming down the pike, so they’ve been building inventories.

As we know, in the recovery that was manufactured by the Fed (and other central banks), Main Street didn’t participate–trillions of dollars spent and little impact on the real economy. But this survey shows that the Trump effect is already doing what nine years, and trillions of dollars of monetary stimulus and intervention, couldn’t do. Most of the small business sentiment data has now returned to pre-crisis levels, just on the pent up demand that has been unleashed by the prospects of a return to prosperity.

This number tends to correlate highly with consumer confidence numbers. Consumer confidence numbers drive consumption. And consumption contributes about two-thirds of GDP. By restoring confidence, the Trump effect on growth can be self-fulfilling.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

In the middle of June we have perhaps the two biggest events of the year. On June 15 the Fed will decide on rates. And hours later, that Wednesday night, the Bank of Japan will follow with its decision on policy.

This is really the perfect scenario for the Fed. The biggest impediment in its hiking cycle/”rate normalization process” is instability in global financial markets. Market reactions can lead to damage to consumer sentiment, capital flight and tightening in credit—all the things that can spawn the threat of a global economic shock, which can derail global recovery. Clearly, they are very sensitive to that. On that note, the Brexit risk, while a hot topic in the news, is priced by experts as a low probability.

So, the Fed has been setting expectations that a second hike in its tightening cycle could be coming this month. But the market isn’t listening. The market is pricing in just a 23% chance of a hike in June. But as we’ve said, markets can get it wrong, sometimes very wrong. We think they have it wrong this time. We think there is a much better chance. Why? Because they know the BOJ is right behind them. If they do hike, any knee jerk hit to financial markets can be quelled by more easing from the BOJ.

Remember, as we’ve discussed quite a bit in our daily notes, central banks remain in control. The recovery was paid for by a highly concerted effort by the world’s top economic powers and central banks. And despite the perceived hostility over currency manipulation, the powers of the world understand that the U.S. is leading the way out of recovery, and that Europe and Japan are critical pieces in the global recovery. The ECB and BOJ have been passed the QE torch from the Fed to both fuel recovery and promote global economic stability. And playing a major role in that effort is a weaker euro and a weaker yen.

The Bank of Japan is operating with one target in mind, create inflation. Now three years into their massive program, they haven’t posted a positive monthly inflation number since December. Inflation is still dead, just as it has been for the past two decades. So, not only do they have the appetite and global support to do more, but the data more than justifies more action.

Don’t Miss Out On This Stock

In our Billionaire’s Portfolio we followed the number one performing hedge fund on the planet into a stock that has the potential to triple by the end of next month.

This fund returned an incredible 52% last year, while the S&P 500 was flat. And since 1999, they’ve done 40% a year. And they’ve done it without one losing year. For perspective, that takes every $100,000 to $30 million.

We want you on board. To find out the name of this hedge fund, the stock we followed them into, and the catalyst that could cause the stock to triple by the end of the month, click here and join us in our Billionaire’s Portfolio.

We make investing easy. We follow the guys with the power and the influence to control their own destiny – and a record of unmatchable success. And you come along for the ride.

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.

As we’ve discussed, we’re in a world where the baton has been passed from a central bank driven economy (post-financial crisis) to a fiscal and public policy driven economy (Trumponomics).One of the pillars of the Trump plan is deregulation. On that note, there’s been plenty of carnage across industries since the financial crisis, but no area has been crushed more and been crushed more by regulation more than Wall Street. And under the Trump administration, those regulations look like they are going to be slashed.Dodd-Frank and the fiduciary rule are bubbling up toward the top of the administrations confrontation list. With a former Goldman president heading the economic team for the President and a former Goldman guy running Treasury, I suspect they will give proprietary risk taking back to banks. The bank’s trading businesses will be back on-line and it will be restoring a huge profit engine.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.

It’s jobs week. Thanks to 1) Trump’s reminder to the country in his address to Congress last week that big economic stimulus was coming, and 2) Yellen’s remarks last week that all but promised a rate hike this month, the market is about as close to fully pricing in a rate hike as possible for March 15.