On this day a year ago the stock market posted the all-time high.

If you recall, coming into 2022, the Fed, staring down the barrel of 7% inflation, told us that they would tame inflation, and land close to their target of 2% by the end of 2022. And, they told us that they would do so while producing a 4% growth economy (well above trend) at 3.5% unemployment (near record levels) — all while keeping the Fed Funds rate under 1%.

What did they do? They took rates above 4%, crushed growth (induced a technical recession) and didn’t get near their inflation target.

As I said in my Pro Perspectives note last year this time, a new year can often come with regime change in markets.

We had the extreme of regime change.

Not only did we go from an easing to a tightening cycle, for global monetary policy. But we went from a long-era of low inflation, and ultra-easy money, to a high inflation, and inflation fighting policy.

We went from a fed that was a fervent defender of financial market stability, and promoter of economic prosperity, to a Fed that explicitly attacked jobs and demand, and went to great lengths to talk down the stock market (in effort to tighten financial conditions).

With that about face, for anyone looking to earn investment returns, much less preserve buying power against inflation, there were few places to hide. Not only did stocks do poorly, but bonds did worse — an outcome with few historical reference points in down stock markets and higher uncertainty environments.

The good news: The rate-of-change in monetary policy tightening will slow dramatically this year (and could possibly be a zero rate-of-change, which would be a positive surprise for markets). The rate-of-change in the fiscal policy madness will be zero, with a split Congress (= gridlock). The latter takes pressure off of the Fed.

Remember, the Fed was ready to pause on rates at 2.25% back in July. That was before the Biden White House and democrat-controlled Congress decided to greenlight another $1 trillion-plus spending binge. The Fed won’t get sideswiped with any more ofthese surprises, with a split Congress.

On a related note, remember, going back to 1950, there has never been a 12-month period, following a midterm election, in which stocks were down. And the average one-year return following the eighteen midterm elections of the past seventy years was 15% (about double the long-term average return of the S&P 500).

Keep in mind, markets have priced in a lot of negative expectations (from the rate path, to earnings erosion, to recession). That sets up for positive surprises. Stocks like positive surprises.

What is among the best performing asset coming out of a bear market in stocks? Small cap value stocks. That’s precisely what we hold in our Billionaire’s Portfolio (with the extra kicker of a catalyst, often from the direct influence of a billionaire investor). We significantly outperformed broader markets in 2022, and are positioned to have an explosive bounce in 2023 (perhaps similar to what we saw in 2016, where we bounced 40 percentage points from the low point of the broader market correction — outpacing the S&P by 2 to 1).

Click here to join me, and get your portfolio in line with ours.

Stocks continued the big bounce today into technical support.

Let’s take an updated look at the S&P 500 chart …

So, we had a 5.5% decline in this benchmark index to start the year, and now we have a sharp bounce of nearly 3% from this big technical trendline, which comes in from the election day lows of November 2020 (an important marker).

We heard from Jay Powell today, in his renomination hearings before the Senate. He did nothing to change the expectations on the Fed’s guidance on the rate path. Whether it be three or four hikes this year, we’ve just finished a year with around 10% nominal growth and over 5% inflation.

The coming year may be more of the same, and yet we have a market and Fed posturing and speculating over how close to 1% the Fed Funds rate might be by year end. That dynamic only adds fuel to the inflation and growth fire.

On that note, we’ve been watching three key spots that should be on the move with this policy outlook: bonds (down), gold (up) and the dollar (down).

Gold was up 1.25% today, making another run at this 1830-50 level. If that level gives way, the move in gold should accelerate. As you can see in the chart, we would get a breakout from this big corrective trend that comes down from the August 2020 all-time highs.

On a related note (dollar down, commodities up), the dollar looks vulnerable to a breakdown technically …

We kick off fourth quarter earnings this week. We’ll hear from the big banks on Friday: JP Morgan, Citi and Wells Fargo.

Bank of America and Goldman Sachs earnings will come early next week.

Last year, across the broad market, the table was set for positive earnings surprises, against a backdrop of deliberately dialed down expectations. And those low expectations were against a low base of 2020, pandemic/lockdown numbers.

With that, we’ve had positive earnings surprises throughout the first three quarters of 2021. The expectation is for 21% earnings growth for Q4, which would give us four consecutive quarters of 20%+ earnings growth and 40% earnings growth on the year.

That said, of the nearly 100 S&P 500 companies that have issued guidance for Q4, 60% are negative. That’s straight from the corporate America playbook: Using the cover of the Omicron news from late November to lower expectations, to position themselves to manufacture positive earning surprises OR withhold some earnings power for next quarter.

So, in addition to the changing interest rate cycle, could the slide in stocks to open the year have something to do with weaker Q4 earnings? Maybe.

On that note, let’s take a look at the big technical support hit today …

In the chart above, the S&P 500 hit this big trendline that comes in from election day. This rise in stocks, of course, has everything to do with an agenda that entailed even more massive fiscal spending programs — AND a central bank that remained in an ultra-easy stance.

Indeed, we’ve since had another $1.9 trillion spend passed in late January of last year, plus a $1.2 trillion infrastructure package later in 2021.

Now we have a Fed that has flipped the script, and the additional bazooka agenda-driven fiscal package has been blocked — and we get a test of this big trendline.

The good news: The line held today, and stocks bounced aggressively (about 100 S&P points) into the close.

As you can see in the chart below, we have a similar line in the Nasdaq, dating back to the election. This breached but closed back above the line today.

With the above in mind, we should expect the banks to continue putting up big numbers to kick off the earnings season later this week. That will be fuel for stocks.

Remember, the banks set aside a war chest of loan loss reserves early in the pandemic, and they have been moving those reserves to the bottom line since, at their discretion. As an example, both Citi and JP Morgan have another $5 billion to release, to bring their loan loss reserves back in line with pre-pandemic levels. That’s $5 billion (each) that will be turned into earnings.

Two months ago a short selling research firm alleged that there was misreporting of financials at the Chinese coffee giant, Luckin Coffee. The company denied the report as unsubstantiated speculation with malicious intent.

This morning the company reported that it has suspended its COO and several other employees for misconduct related to fabricating transactions. These are precisely the claims that were made two months ago.

The stock was down more than 80% this morning.

Who was the biggest loser?

It’s the top shareholder and angel investor in Luckin, the Chinese billionaire Lu Zhengyao.

Zhengyao is a serial entrepreneur. He founded the rental car company Car Inc. in 2007 and took it public in 2014 on the Hong Kong Stock Exchange. His former COO is credited with founding the Starbucks competitor, Luckin Coffee in 2017. In 2019, the company IPO’d on the Nasdaq.

Zhengyao was the angel investor behind the company and holds 484 million shares. At yesterday’s close, that stake was valued at over $12 billion. At the lows this morning, it was valued at $2.2 billion. Learn more about the stakes of billionaire investors here.

Predictably, Trump extended the timeline on new tariffs in his meeting with China’s President Xi over the weekend.

This is kicking the trade war can down the road. That extends the timeline on the trade war and resets the opportunity to force the Fed’s hand this coming month–to get a rate cut at the July 30-31 Fed meeting.

As we’ve discussed, with a rate cut under his belt, this would clear the way for Trump to, then, claim victory on the China trade war by doing ‘a’ deal, giving himself enough runway into the 2020 elections to have a booming stock market and booming economy.

Since December, we’ve been talking about the parallels between the current period and the 1994-1995 period. It’s worth repeating again. The script continues to play out. In 1994, an overly aggressive Fed raised rates into a recovering, low inflation economy. By 1995, they were cutting. That led to a 36% rise in stocks in 1995. And it led to 4% growth in the economy through late 2000–18 consecutive quarters of more than 4% growth. Stocks tripled over the five-year period.

Think about that, and then remove the overhang of a trade war with the two biggest economies of the world and you can see the path to some very good times ahead. Moreover, if the above scenario plays out, Trump would then likely turn back to Congress and green-light a $2 trillion infrastructure plan.

While many have been predicting economic bust, this is a formula for an economic boom!

We end the week, month and quarter today. Stocks are up 17% year-to-date.

With the big Trump/Xi meeting coming over the weekend, let’s talk about how Fed policy has flipped from a headwind (adding to the risks), to a tailwind (backstopping against the risks – an implicit “put”).

And that’s why the chart on the S&P 500 looks like this …

Of course we’ve had big geopolitical risks along the timeline of this chart, that include an historic trade war (which continues) and potential sanctions against Saudi Arabia (late last year).

The geopolitics have consumed the markets attention. But maybe it’s all about the Fed, and their ability to interpret (or lack thereof) the impact of trade disputes and structural reform in the global economy – and position correctly.

If we look back at the timeline, the tops and bottoms in these V-shaped moves in the chart above all align perfectly with Fed speak.

Stocks topped on October 3rd and proceeded to drop 20% through the end of December. What happened on October 3rd? The Fed chair, Jay Powell, did a sit down interview with PBS, where he said, after raising rates three times for the year, that they remain far away from the ‘neutral’ rate. And he said they may go past neutral. Why? He thought tariffs and the uptick in wage growth would feed into inflation. He was wrong.

With that view of tighter and tighter monetary policy into a low inflation and recovering economy, with hurdles of trade reform in the path, the markets started signaling the contra-viewpoint: the trade war weighs on global growth, and within that context, rising U.S. rates are a killer for emerging market economies, and for the slow recovering developed markets.

Powell’s comments started the decline, which ultimately led to a big decline. Yet, the tone-deaf Fed raised rates in December, again, right into a falling stock market. Moreover, following the December Fed meeting, the Fed made it clear that they were prepared to mechanically keep raise rates — another four times in 2019.

When did it turn? It turned the day (January 4th) the Fed marched out Powell, Bernanke and Yellen, (tails between their legs) to tell the world ‘no more rate hikes/ the Fed is done.’

Stocks bottomed, on that day, and did a perfect ‘V’ back to the record highs over the following months.

When did it top again? May 1. What happened on May 1? The Fed met and Jay Powell had his post-meeting press conference. After months of running Fed officials out in the media to tell us the Fed’s got your back, Powell fumbled.

The interest rate market (10-year yields) had fallen 75 basis points from the highs of just six months prior, giving a very clear message to the Fed that, at the very least, the December hike was a policy mistake. But Powell was unwilling to show any leaning toward a rate cut. In fact, he said the risks that precipitated their “pause” on the rate path (China and European growth, Brexit risks, and trade negotiations), have been largely improving. Again, the Fed was tone-deaf and unwilling to take a defensive stance against the unknowns of geopolitical risks. Stocks go down.

A few days later, U.S./China trade talks come to a standstill. Stocks continue on for a 7% decline.

When did stocks bottom? June 3rd. What happened? A voting Fed member, Jim Bullard said that a Fed cut may be “warranted soon” to “provide some insurance” in case of a sharper slowdown. That was a primer for a June 4th speech by Jay Powell. Powell came out of the gates, in a prepared speech that morning, telling us they “will act as appropriate to sustain the expansion.” That spurred the second “V-shaped recovery” on the above chart.

The conversation at the Fed has now, finally, turned to rate cuts. And the market is now expecting a 100% chance the Fed will cut at the July 31 meeting.

Perhaps now the Fed is in the right position, trade deal or no trade deal. And that should be very good for stocks.

Remember, the last time the Fed was in this position in 1994, they cut rates and that led to a huge year for stocks — and stocks and the economy boomed through the end of the nineties.

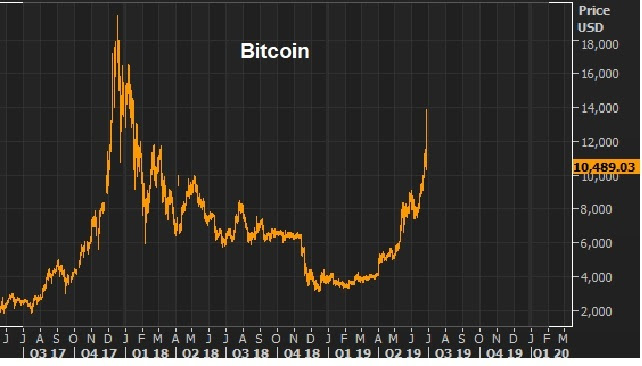

Bitcoin has had another huge move over the past three months — more than tripling. And then late yesterday afternoon, it collapsed 15% in just minutes. It lost 25% in value on the day.

The first rise and fall in Bitcoin, from $1,000 to $19,000 and back to $3,000, took place from early 2017 to early 2018. Most of the move was over just four months.

Here’s a look at the chart. You can see the first run-up and this most recent run-up …

Remember, this first run-up had everything money moving out of China, and less to do with Silicon Valley genius/ global monetary system disruption.

In late 2016, with rapid expansion of credit in China, growing non-performing loans, a soft economy and the prospects of a Trump administration that could put pressure on China trade, capital was moving aggressively out of China. That’s when the government stepped UP capital controls — better policing movement of capital out of China, from transfers to foreign investment (individuals can move just $50,000 out of the country a year).

Of course, resourceful Chinese still found ways to move money. Among them, buying Bitcoin. And that’s when Bitcoin started to really move (from sub-$1,000). China cryptocurrency exchanges were said to account for 90% of global bitcoin trading. Capital flows were confused with Silicon Valley genius.

But in September of last year China crackdown on Bitcoin – with a total ban. A few months later, Bitcoin futures launched, which gave hedge funds a liquid way to short the madness. Bitcoin topped the day the futures contract launched. And a few months later it was worth 1/6th of its value at the top.

Is this time different? Is this real traction for Bitcoin, or is this just Chinese capital flows looking for a parking place, again? Likely, the latter. It’s probably no coincidence that as the prospects of a ‘no deal’ with China have elevated in recent months, Bitcoin has again been on the move. As we’ve discussed, if Trump holds firm on his demands, it seems impossible that China can do his deal. It’s political suicide for the Chinese Communist Party. With that, they fight tariffs with a devaluation of the yuan.

With those prospects, if you have money in China, you have been getting it out! While cryptocurrency exchanges have been banned in China, owning and buying Bitcoin in China is not banned. The Bitcoin futures market and off-exchange (peer-to-peer) trading are liquidity sources for Chinese citizens to respond to potential devaluation in the yuan.

With the above in mind, this round of Bitcoin bubble may not deflate until/unless Trump makes concessions to do a deal (which seems unlikely until, at least, we get past the July Fed meeting).

If you haven’t signed up for my Billionaire’s Portfolio, don’t delay … we’ve just had another big exit in our portfolio, and we’ve replaced it with the favorite stock of the most revered investor in corporate America — it’s a stock with double potential.

Join now and get your risk free access by signing up here.

This morning Mnuchin was interviewed by CNBC. He was the headline of the day, despite saying nothing new.

When trade talks broke down in early May, the Trump administration said they were 90% of the way to a deal. But China balked and reneged on concessions. Mnuchin said the same thing today (we were 90% there), and the media presented it as if he said progress was made this week, heading into the meetings. That’s not what he said.

Let’s talk about the backdrop heading into the weekend negotiations. Remember, Trump is in the driver’s seat in this negotiation. He can’t force a good deal, but he can claim victory on the trade front just by doing ‘a’deal.

With that in mind, as we’ve discussed over the past month, he seems to be attempting to surgically optimize the economy heading into next year’s election. He’s been fighting for a Fed rate cut, and through introducing heightened risks of a standstill on trade, he’s gotten what looks like Fed compliance coming down the pike (for a July cut).

The timeline set up perfectly for a June rate cut, and then for Trump to settle on a China deal at the G20 meeting. The economy would have launched like a rocket-ship. The Fed didn’t comply.

With that, at this weekends Trump/Xi meeting, let’s see if Trump extends the timeline on new tariffs, to get through the July Fed meeting (in hopes of getting his Fed fuel for the economy). At this point, the market has backed the Fed into the corner, with high expectations of not just 25 bps, but a 50 bps cut. Without an extension of trade uncertainty, those expectations will sustain if not grow.

Now, we’ve discussed over the past month, the prospects for this trade war with China ending with a grand and coordinated currency agreement — perhaps a big depreciation of the dollar, similar to the 80s “Plaza Accord.”

As I said a couple of weeks ago, we may wake up one day and find a similar agreement has been made between the U.S. and major global trading partners (which may include China, or not). It might be a deal between the U.S. and China to “revalue” the yuan (i.e. strengthen it). Or it may exclude China (just G3 economies). An interesting takeaway from this morning’s interview with Mnuchin: Mnuchin did make a point to emphasize that they look forward to many bi-lateral meetings at the G-20 — not just with China.

How do you position for a dollar devaluation? Buy commodities. Is that what the move in gold is telling us (and Bitcoin)? Maybe.

If you haven’t signed up for my Billionaire’s Portfolio, don’t delay … we’ve just had another big exit in our portfolio, and we’ve replaced it with the favorite stock of the most revered investor in corporate America — it’s a stock with double potential.

Join now and get your risk free access by signing up here.

Remember, last year was the first year since 1994 that cash was the best producing asset class (among stocks, real estate, bonds, gold).

This year, as it did in 1995, the pendulum has swung.

Stocks are up 16% year-to-date. The Dow Jones Real Estate Index is up 19%. Gold is up 11%.

As you can see below, there is a lot of green on the year for global asset prices …

As we’ve discussed for much of the year, what else is similar between the current and 1994-1995 period? We had an overly aggressive Fed, that tightened into a low inflation, recovering economy. In 1995, they did an about face, cutting rates at their July meeting. And now we head into the July Fed meeting with expectations of a 50bps cut.

On that note, we heard from the Fed just days ago, signaling that they were ready to act if conditions deteriorated. And as I said following the meeting: “What is clear, from Powell’s press conference, is that this is all about the China trade deal. If it drags out, sentiment continues to erode. When sentiment erodes, the economic momentum will erode. If that’s the case, they will be reactive, with stimulus (rate cuts and/or slowing the runoff of Treasuries on the Fed balance sheet).”

Today, Jerome Powell was again on a stage talking about monetary policy, at a conference on the Economic Outlook and Monetary Policy at the Council on Foreign Relations. He had a prepared speech and did a Q&A. So what message was he trying to send to markets?

He did a lot of talking. But I suspect his posturing doesn’t matter at this point. This less about him, or the economy, and more about Trump. If Trump were to back off the hardline demands and signal a deal with China over the weekend, the Fed would be off the hook — no rate cut. If the meeting comes and goes, and it’s a clear kick the can down the road, or no deal –we get a cut by the Fed come July (whatever size and scope is necessary).

Let’s take a look at gold as we head into the Trump/Xi meeting scheduled to take place at the end of the week’s G20 meeting.

Gold has been sold all along as an “inflation hedge.” But unless you have Weimar Republic-like hyperinflation, you’re unlikely to get the inflation-hedge value out owning it.

Remember, gold went on a tear from sub-$700 to above $1,900 following the onset of global QE (led by the Fed). Gold ran up as high as 182%. That was pricing in 41% annualized inflation at one point (as a dollar for dollar hedge). Of course, inflation didn’t comply. Still, ten years after the Fed’s first round of QE and massive global responses, we’ve been able to muster just a little better than 1% annualized inflation.

If you bought gold at the top in 2011, the value of your “investment” was cut in half just four years later. That’s a lot of risk to take for the prospect of “hedging” against the loss of purchasing power in the paper money in your wallet.

So, gold isn’t a hedge against inflation, it’s a hedge against the worst-case scenario. It’s for sovereign wealth and anyone else that can take delivery, own and control the storage. For almost everyone else, it’s a speculative trade.

Join now and get your risk free access by signing up here.