June 21, 5:00 pm EST

As we end the week, any questions on whether or not the central banks have your back, have been answered.

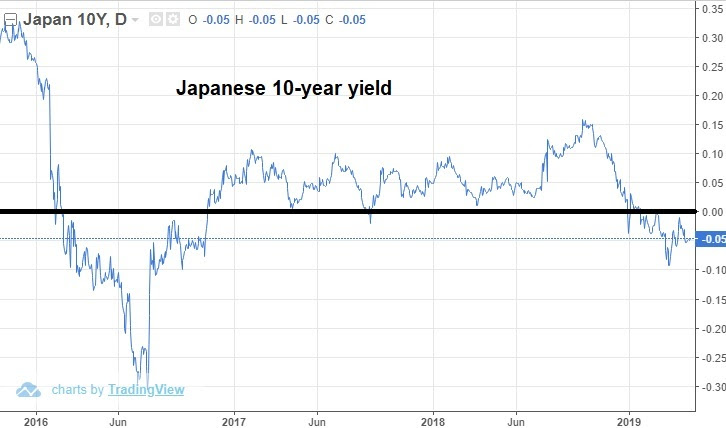

Just as they have for the better part of a decade, they have no choice but to respond to any shocks that might knock the global economic recovery off path. And as I said yesterday, the major central banks of the world have lined up, because they are unable to predict what Trump will do on trade. To maintain market confidence, they have to posture as if they assume the trade war will go on indefinitely.

On that note, it seems to be priced into the global treasury markets and the gold market that China can’t accept Trump’s deal (or at least can’t deliver on the current demands of the deal). It’s politically unpalatable and an existential threat to the Chinese Communist Party. So, the question is, will Trump end the trade dispute with more bark than bite? Will he do a deal (not the deal) and remove the overhang of uncertainty from the global economy, and an election coming next year. Next week should be interesting, as we await the Trump/Xi meeting at the G20 (scheduled for Friday 6/28 and Saturday 6/29).

As we head into this weekend, markets hang around big levels: record highs in stocks, the big 1,400 level in gold, just above 2% on the 10-year, and closing in on 10k in Bitcoin (a haven for Chinese capital flight).

May 30, 5:00 pm EST

The first revision of Q1 GDP came in this morning, in-line with expectations (at 3.1%). As yields swoon, and stocks have given back some gains for the month, this growth number today is good reminder that the state of the U.S. economy is good.

Remember, back in April, the first look at Q1 GDP came in as a huge positive surprise (at 3.2%). Many were expecting it to be a terrible quarter. Goldman Sachs thought the quarter would produce just 0.7% growth. They were wrong, and they weren’t alone. At the end of the first quarter, the Atlanta Fed’s GDP model was estimating that the economy grew at only 0.3% in Q1.

With that in mind, don’t get too caught up in the souring growth story. At the moment, the consensus view on Wall Street is for Q2 growth to come in at 1.8%. And the Atlanta Fed model is looking for 1.3%. Both are well lower than the White House envisioned 3%+ growth trend.

But, for perspective, there are some clear factors working in favor of the higher (not lower) growth case.

The job market is strong. We have monthly new jobs running at a 12-month average of 218k. That’s well above pre-financial crisis average monthly job growth. The unemployment number at 3.6% is the lowest since 1969.

Most importantly: Wage growth has been on the move for the past 18 months, now sustaining above 3%. And Q1 productivity came in at 3.6%, the hottest productivity reading in almost a decade. The economy can grow by expanding the size of the workforce or the productivity of the workforce. We’re finally getting solid productivity growth.