If you are a regular reader of my daily notes, you’ll know we’ve been discussing the setup for positive surprises all year.

As we’re near the end of Q1 earnings season, clearly we’re getting it. With 78% of the companies in the S&P 500 now reported on Q1 earnings, 76% have beat earnings estimates.

And we’re getting positive surprises in the economic data. We had a huge positive surprise for Q1 GDP this week. And today we had a blow out jobs report.

There were 263k jobs added in April. The market was expecting just 185k. That gives us a 12-month average of 218k, well above pre-financial crisis average monthly job growth! The unemployment number was 3.6% — the lowest since 1969.

Remember, we’ve been told all year long that we were headed for both earnings and economic recession. It’s not happening.

Moreover, the two missing pieces of the economic recovery puzzle, have been productivity and wage growth. And these pieces are emerging. Wage growth has been on the move for the past 18 months, now sustaining above 3%. And we had a huge positive surprise in productivity this week.

With the above in mind, given the contrast of media narrative and reality, how are people getting it so wrong? I suspect we are seeing plenty of people make the mistake of letting politics cloud their judgement on the economy and the outlook for stocks.

The jobs report this morning continued to show an improving economy, operating with the luxury of low inflation.

I say improving because as the unemployment rate ticked higher, it represents people coming back into the work force. Those people that have been discouraged along the way, through the economic crisis and recovery, and have dropped out of the work force, are coming back, looking for work.

Remember, the missing piece of the recovery puzzle over the past decade has been wage growth. That has been the telltale sign of the job market, despite the low headline number. With little leverage in the job market to maximize potential, much less command higher wages, consumers tend not to chase prices in goods and services higher–and they tend not to take much risk. This tells you something about robustness of the economy. And that’s precisely why we’ve needed fiscal stimulus and structural reform. And it’s just in the early stages of feeding through the economy.

The other big news of the day was trade. The U.S. started implementing duties on $34 billion of Chinese imports today. On that note, the media has been focused on one specific sentence in the Fed’s minutes yesterday. After weeding through the long conversation on how well the economy was doing, they picked out this sentence to build stories around “contacts in some Districts indicated that plans for capital spending had been scaled back or postponed as a result of uncertainty over trade policy.” Plucking this one out and using it to support their scenarios of trade wars and economic implosion has to be good for reeling in readers.

But keep in mind capital goods orders (the chart below) are nearing record highs again.

Add to this: An ISM survey back in December showed that businesses were forecasting just 2.7% growth in capitalspending for 2018. But when they were asked again in May, they had revised that number UP to 10.1% growth.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

We’ve talked the past couple of days about economic growth and the likelihood that we’re just beginning to see the positive surprises from Trumponomics materialize in the economic data.

The formula for GDP is consumption + investment + government spending + net exports. So you can see in these components, the direct targeting of economic stimulus in the Trump economic plan to drive growth: tax cuts, deregulation, repatriation, infrastructure and trade negotiations.

Now, consumption makes up about two-thirds of GDP. Let’s look at consumption today, and we’ll step through the other contributors to GDP over the next few days.

First, what is the key long-term driver of economic growth over time? Credit creation. When credit is used to buy productive resources, wealth goes up. And when wealth goes up consumption tends to go up. With that in mind, in the chart below you can see the sharp recovery in consumer credit (in orange) since the depths of the economic crisis (this excludes mortgages). And you can see how closely GDP (the purple line, economic output) tracks creditgrowth.

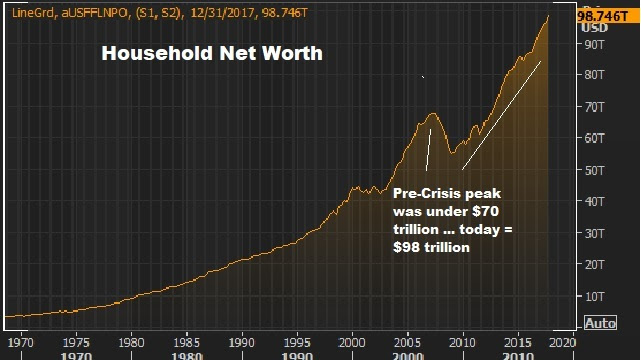

And we have well recovered and surpassed pre-crisis levels in householdnetworth — sitting at record highs now (up another $2 trillion since we last looked at it) …

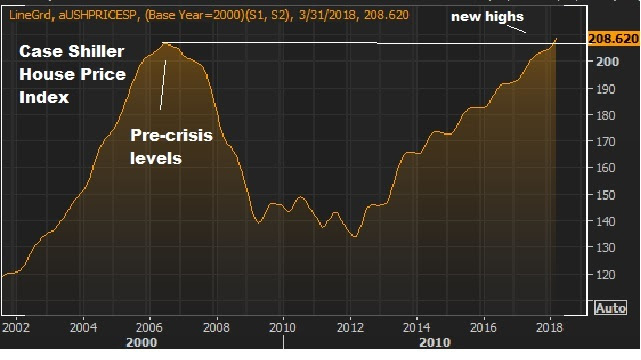

A large contributor to the state of consumption is the recovery and stability in housing. We are now back to new highs on the broad housing index …

When we consider this solid backdrop, remember, we’ve yet to have a return of ‘animal spirits’ — a level of trust and confidence in the economy that fuels more aggressive hiring, spending and investing.

And with that, as we discussed yesterday, while we are in the second longest post-War economic expansion, we’ve yet to have the aggressive bounce back in growth that is characteristic of post-recession recoveries.

But we now have the pieces in place to see the return of animal spirits and a big pop in economic growth. And that should continue to fuel for much higher stock prices. And there are stocks that will do multiples of what the broader stock market does.

We had a jobs report this past Friday. The unemployment rate is at 4.1%. We’re adding about 172k jobs a month on average, over the past twelve months. These are great looking numbers (and have been for quite some time). Yet employees, broadly speaking, still haven’t been able to command higher wages. Wage growth continues to be on the soft side.

With little leverage in the job market, consumers tend not to chase prices in goods and services higher — and they tend not to take much risk. This tells you something about the health of the job market (beneath the headline numbers) and about the robustness of the economy. And this lack of wage growth plays into the weak inflation surprise that has perplexed the Fed. And the weak growth that has perplexed all policy makers (post-crisis). That’s why fiscal stimulus is needed!

And this could all change with the impending corporate tax cut. The biggest winners in a corporate tax cut are workers. The Tax Foundation thinks a cut in the corporate tax rate would double the current annual change in wages.

As I’ve said, I think we’re in the cusp of an economic boom period — one that we’ve desperately needed, following a decade of global deleveraging. And today is the first time I’ve heard the talking heads in the financial media discuss this possibility — that we may be entering an economic boom.

Now, we’ve talked quite a bit about the run in the big tech giants through the post-crisis era — driven by a formula of favor from the Obama administration, which included regulatory advantages and outright government funding (in the case of Tesla). And we’ve talked about the risk that this run could be coming to an end, courtesy of tighter regulation.

Uber has already run into bans in key markets. We’ve had the repeal of “net neutrality” which may ultimate lead big platforms like Google, Twitter, Facebook and Uber, to transparency of their practices and accountability for the actions of its users (that would be a game changer). And we now know that Trump is considering that Amazon might be a monopoly and harmful to the economy.

With this in mind, and with fiscal stimulus in store for next year, 2018 may be the year of the bounce back in the industries that have been crushed by the “winner takes all” platform that these internet giants have benefited from over the past decade.

That’s probably not great for the FAANG stocks, but very good for beaten down survivors in retail, energy, media (to name a few).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We’re finishing the first full week under Trumponomics. And it’s been an active one.

It’s clear now that President Trump intends to follow through on his campaign promises. While that’s making waves with the media and with Washington types, it’s creating more certainty about the outlook for growth for the real economy and, therefore, for financial markets.

We close the week with the Dow above 20,000, on new record highs. And as we discussed yesterday, stock markets around the world are rallying too on the prospects of a stronger U.S. economy translating into a stronger global economy. We looked at the charts of Mexican and Canadian stocks yesterday–both of which are sitting on record highs. U.K. stocks are near record highs and German stocks are quickly closing in.

We already know that small business optimism in the U.S. has hit 12-year highs, jumping by the most in since 1980–on Trump’s pro-growth agenda. Today the consumer sentiment report showed sentiment is on the rise too–at 13-year highs.

Let’s talk about the data that we’re leaving behind. Fourth quarter GDP was reported today at just 1.9%. This, more than seven years removed from the failure of Lehman Brothers, an $800 billion stimulus package, seven years of zero interest rates and three rounds of quantitative easing, and the economy is running at about 60% of its normal pace. And even after taking the Fed’s balance sheet from $800 billion to $4.5 trillion, we have inflation running at less than 50% of its normal pace. This malaise is consistent throughout the world. And this is precisely why big, bold fiscal stimulus and structural change is desperately needed, and is being embraced by those that understand the dangers of the stall-speed global economy that has been kept alive by global central bank intervention. As I’ve said, at Dow 20,000, it’s just getting started.

Have a great weekend!

We are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Jobs, jobs everywhere there’s jobs. The President-elect yesterday said he will be the “greatest job creator God ever created.”

Since December, when the President-elect announced that Carrier, an air conditioner manufacturer in Michigan, would keep 1,000 jobs in the U.S. instead of moving them to Mexico, other companies have been lining up to announce big, bold hiring plans.

It was immediately clear that Carrier won priceless exposure and good-will. From that point, the Japanese billionaire Masayoshi Son took a visit to Trump Tower and followed with an announcement that his Softbank technology holdings company would invest $50 billion in U.S. businesses and create 50,000 new jobs. Softbank owns more than 80% of Sprint, and Sprint has followed with an announcement of 5,000 jobs to come.

Alibaba’s founder Jack Ma visited Trump Tower yesterday and left saying he would create 1 million jobs in the U.S.

Amazon, who’s CEO Jeff Bezos had a visit to Trump Tower last month, said today they plan to add 100k jobs.

Not to be outdone, Taco Bell (part of YUM Brands), said today it would add 1.6 million jobs in the U.S. Does this mean Taco Bell is about to go on a massive expansion increasing their store count by 5x — putting a Taco Bell on every corner in America?

Or, is this all just a public relations ploy? Are they all hoping to gain favor with the administration? Yes and yes. But it’s also all self-reinforcing. A better outlook for jobs is driving confidence. Confidence can drive a better outlook for jobs. More employed, more confident consumers can drive economic growth. And better growth drives more jobs.

Now, all of this said, the headline unemployment number is already down to 4.7% (near what is considered “normal”). The number that measures underemployed and those that have stopped looking is down to 9.2%. It’s much higher than the headline rate, but relative to history, it’s returning close to normal levels too. With the prospects of hotter growth coming, and new job creation, we could be headed for a very tight labor market. What does that mean? Higher wages are coming, to finally begin making up for two decades of wage stagnation.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

Over the past year we’ve had a wild ride in global yields. Today I want to take a look at the dramatic swing in yields and talk about what it means for the inflation picture, and the Fed’s stance on rates.

When oil prices made the final leg lower early last year, the Japanese central bank responded to the growing deflationary forces with a surprise cut of their benchmark interest rate into negative territory.

That began the global yield slide. By mid-year, more than $12 trillion dollars with of government bond yields across the world had a negative interest rate. Even Janet Yellen didn’t close the door to the possibility of adopting NIRP (negative interest rate policies).

So investors were paying the government for the privilege of loaning it their money. You only do that when 1) you think interest rates will go even further negative, and/or 2) you think paying to park your money is the safest option available.

And when you’re a central banker, you go negative to force people out of savings. But when people think the world is dangerous and prices will keep falling, they tend to hold tight to their money, from the fear a destabilized world.

But this whole dynamic was very quickly flipped on its head with the election of a new U.S. President, entering with what many deem to be inflationary policies. But as you can see in the chart below, the U.S. inflation rate had already been recovering, and since November is now nudging closer to the Fed’s target of 2%.

Still, the expectations of much hotter U.S. inflation are probably over done. Why? Given the divergent monetary policies between the U.S. and the rest of the world, capital has continued to flow into the dollar (if not accelerated). That suppresses inflation. And that should keep the Fed in the sweet spot, with slow rate hikes.

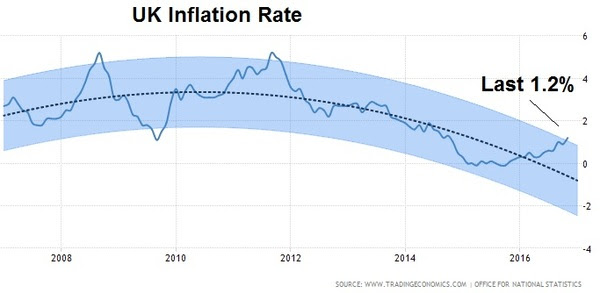

Meanwhile, there’s more than enough room for inflation to run in other developed economies. You can see in Europe, inflation is now back above 1% for the first time in three years. That, too, is in large part because of its currency. In this case, a stronger dollar has meant a weaker euro. This (along with the UK and Japan) is where the real REflation trade is taking place. And it’s where it’s needed most, because it also means growth is coming with it, finally.

You can see, following Brexit, the chart looks similar in the UK – prices are coming back, again fueled by a sharp decline in the pound, which pumps up exports for the economy.

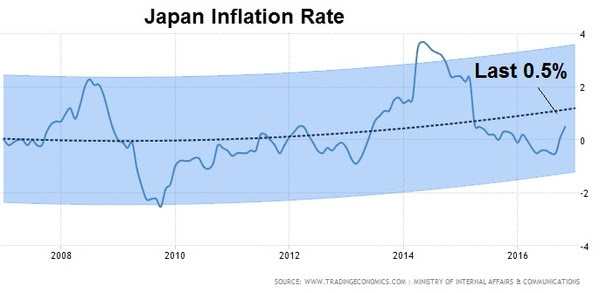

And, here’s Japan.

Japan’s deflation fight is the most noteworthy, following the administrations 2013 all-out assault to beat 2 decades of deflation. It hasn’t worked, but now, post-Trump, the stars may be aligning for a sharp recovery.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

With the Dow within a fraction of 20,000 today, and with the first week of 2017 in the books, I want to revisit my analysis from last month on why stocks are still cheap.

Despite what the media may tell you, the number 20,000 means very little. In fact, it’s amusing to watch interviewers constantly probe the experts on TV to get an anwer on why 20,000 for the Dow is meaningful. They demand an answer and they tend to get them when the lights and a camera are locked in on the interviewee.

Remember, if we step back and detach from the emotions of market chatter, speculation and perception, there are simple and objective reasons to believe the broader stock market can go much higher from current levels.

I want to walk through these reasons again for the new year.

Reason #1: To return to the long-term trajectory of 8% annualized returns for the S&P 500, the broad stock market would still need to recovery another 49% by the middle of next year. We’re still making up for the lost growth of the past decade.

Reason #2: In low-rate environments, the valuation on the broad market tends to run north of 20 times earnings. Adjusting for that multiple, we can see a reasonable path to a 16% return for the year.

Reason #3: We now have a clear, indisputable earnings catalyst to add to that story. The proposed corporate tax rate cut from 35% to 15% is estimated to drive S&P 500 earnings UP from an estimated $132 per share for next year, to as high as $157. Apply $157 to a 20x P/E and you get 3,140 in the S&P 500. That’s 38% higher.

Reason #4: What else is not factored into all of this simple analysis, nor the models of economists and Wall Street strategists? The prospects of a return of ‘animal spirits.’ This economic turbocharger has been dead for the past decade. The world has been deleveraging.

Reason #5: As billionaire Ray Dalio suggested, there is a clear shift in the environment, post President-elect Trump. The billionaire investor has determined the election to be a seminal moment. With that in mind, the most thorough study on historical debt crises (by Reinhardt and Rogoff) shows that the deleveraging of a credit bubble takes about as long as it took to build. They reckon the global credit bubble took about ten years to build. The top in housing was 2006. That means we’ve cleared ten years of deleveraging. That would argue that Trumponomics could be coming at the perfect time to amplify growth in a world that was already structurally turning. A pop in growth, means a pop in corporate earnings–and positive earnings surprises is a recipe for higher stock prices.

For these five simple reasons, even at Dow 20,000, stocks look extraordinarily cheap.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

We talked yesterday about the bad start for global markets in 2016. It was led by China. Today, it was a move in the Chinese currency that slowed the momentum in markets. Yields have fallen back. The dollar slid. And stocks took a breather.

China’s currency is a big deal to everyone. It’s the centerpiece of the tariff threats that have been levied from the U.S. President-elect. I’ve talked quite a bit about that posturing (you can see it again here: Why Trump’s Tough Talk On China May Work).

As we know, China, itself, sets the value of its currency every day. It’s called a managed float. They determine the value. And for the past two years, they’ve been walking it lower — weakening the yuan against the dollar. That’s an about face to the trend of the prior nine years. In 2005, in agreement with their major trading partners (primarily the U.S.), they began slowly appreciating their currency, in an effort to allay trade tensions, and threats of trade sanctions (tariffs).

So what happened today? The Chinese revalued its currency — pegged ithigher by a little more than a percent against the dollar. That doesn’t sound like a lot, but as you can see in the chart, it’s a big move, relative to the average daily volatility. That became big news and stoked a little bit of concern in markets, mostly because China was the sore spot at the open of last year, and the PBOC made a similar move around this time, when global marketswere spiraling.

Why did they do it? This time around, the Chinese have complained about the threat of capital flowing out of the country – it’s a huge threat to their economy in its current form. That’s where they’ve laid the blame, on the two year slide in the value of the yuan. With that, they’ve allegedly been fighting to keep the yuan stable and have been stepping up restrictions on money leaving the country. Today’s move, which included a spike in the overnight yuan borrowing rate, was a way to crush speculators that have been betting against the currency, putting further downward pressure on the currency. But it also likely Trump related – the beginning of a crawl higher in the currency as we head toward the inauguration of the new President Trump. It’s very typical for those under the gun for currency manipulation to make concessions before they meet with trade partners.

So, should we be concerned about the move today in China? No. It’s not another January 2016 moment. But the move did drive profit taking in twobig trends of the past two months: the dollar and U.S. Treasuries. With that, the first jobs report of the year comes tomorrow. It should provide more evidence that the Fed will hike a few times this year. And that should restore the climb in the dollar and in rates.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Remember this time last year? The markets opened with a nosedive in Chinese stocks. By the time New York came in for trading, China was already down 7% and trading had been halted. That started, what turned out to be, the worst opening stretch of a New Year in the history of the U.S. stock market.

The sirens were sounding and people were gripping for what they thought was going to be a disastrous year. And then, later that month, oil slid from the mid $30s to the mid $20s and finally people began to realize it wasn’t China they should be worried about, it was oil. The oil price crash was a ticking time bomb, about to unleash mass bankruptcies on the energy industry and threaten a “round two” of global financial crisis.

What happened? Central banks stepped in. On February 11th, the Bank of Japan intervened in the currency markets, buying dollars/selling yen. What did they do with those dollars? They must have bought oil, in one form or another. Oil bottomed that day. China soon followed with a move to boost bank lending, relieving some fears of a global liquidity crunch. The ECB upped its QE program and cut rates. And then the Fed followed up by taking two of their projected four rate hikes off of the table (of which they ended up moving just once on the year).

What a difference a year makes.

There’s a clear shift in the environment, away from a world on liquidity-driven life support/ and toward structural, growth-oriented change.

With that, there’s a growing sense of optimism in the air that we haven’t seenin ten years. Even many of the pros that have constantly been waiting for the next “shoe to drop” (for years) have gone quiet.

Global markets have started the year behaving very well. And despite the near tripling from the 2009 bottom in the stock market, money is just in the early stages of moving out of bonds and cash, and back into stocks. Following the election in November, we are coming into the year with TWO consecutive record monthly inflows into the U.S. stock market based on ETF flows from November and December.

The tone has been set by U.S. markets, and we should see the rest of the world start to play catch up (including emerging markets). But this development was already underway before the election.

Remember, I talked about European stocks quite a bit back in October. While U.S. stocks have soared to new record highs, German stocks have lagged dramatically and have offered one of the more compelling opportunities.

Here’s the chart we looked at back in October, where I said “after being down more than 20% earlier this year, German stocks are within 1.5% of turning green on the year, and technically breaking to the upside“…

And here’s the latest chart…

You can see, as you look to the far right of the chart, it’s been on a tear. Adding fuel to that fire, the eurozone economic data is beginning to show signs that a big bounce may be coming. A pop in U.S. growth would only bolster that.

And a big bounce back in euro zone growth this year would be a very valuabledefense against another populist backlash against the establishment (first Grexit, then Brexit, then Trump). Nationalist movements in Germany and France are huge threats to the EU and euro (the common currency). Another round of potential break-up of the euro would be destabilizing for the global economy.

With that, as we enter the year with the ammunition to end the decade long economy rut, there are still hurdles to overcome. Along with Trump/China frictions, the French and German elections are the other clear and present dangers ahead that could dull the efficacy of Trumponomics.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2017. You can join me here and get positioned for a big 2017.

Jobs, jobs everywhere there’s jobs. The President-elect yesterday said he will be the “greatest job creator God ever created.”

Jobs, jobs everywhere there’s jobs. The President-elect yesterday said he will be the “greatest job creator God ever created.”