|

|

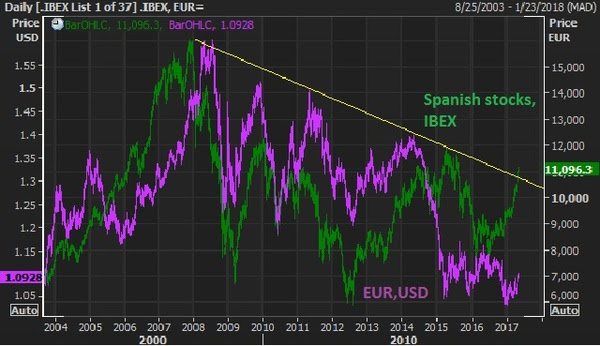

February 4, 5:00 pm EST U.S. stocks are being valued right at the long-term P/E, just under 16x forward earnings. And remember, that’s in an ultra-low interest rate environment (still). Historically, in low rate environments stocks trade north of 20 times earnings. With the Fed now on hold, and the 10-year yield back below 3%, if we continue to see this sweet spot of good economic activity and subdued inflation, we should see this multiple on stocks expand toward 20 this year. If we multiply Wall Street’s 2019 earnings estimate on the S&P 500 ($172) times a P/E of 20, we get 3,440 in the S&P 500. That’s 26% higher than current levels. Now, stocks in the U.K., Germany and Japan are all trading closer to 12x forward earnings. That’s cheap relative to long-term averages, and especially cheap relative to U.S. stocks. For perspective, Japanese stocks are recovering back toward the highest levels in more than 25 years, yet the forward P/E on Japanese stocks is closer to the lowest levels over the period. From a technical perspective, Japanese stocks should follow the lead of this big trend break in U.S. stocks…

|

|

|

Here’s a look at the Nikkei and the opportunity to see this “laggard” catch up … |

|

|

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

|

July 23, 5:00 pm EST

We have a big earnings week. The tech giants report, along with about a third of the S&P 500. And we get our first look at Q2 GDP.

As we’ve stepped through the year, we’ve had a price correction in stocks, following nearly a decade of central bank policies that propped up stocks. This correction made sense, considering central banks were finally able to make the hand-off to a U.S. led administration that had the will and appetite (and alignment in Congress) to relax fiscal constraints and force the structural reform necessary to promote an economic boom.

From there, for stocks, it became a “prove-it to me” market. Let’s see evidence of this “hand-off” is working — evidence the fiscal stimulus is working. That came in the form of first quarter earnings. This showed us clear benefits of the corporate tax cut. The earnings were hot, and stocks began a recovery.

The next steps, as fiscal stimulus works through the economy, we’ve needed to see that the uptick in sentiment (from the pro-growth policies) is translating into better demand and economic activity. So, with Q2 earnings we should start seeing better revenue growth, companies investing and hiring. And we should see positive surprises beginning to show up in the economic data.

We’re getting it. Almost nine out of ten companies reporting thus far have beat (lofty) earnings expectations. And about eight out of ten have beat on revenues. This week will be important, to solidify that picture. And though many of the economists all along the way of the past year didn’t see big economic growth coming, it has been steadily building since Trump was elected, and the Q2 number should push us to over 3% annual growth (averaging that past four quarters).

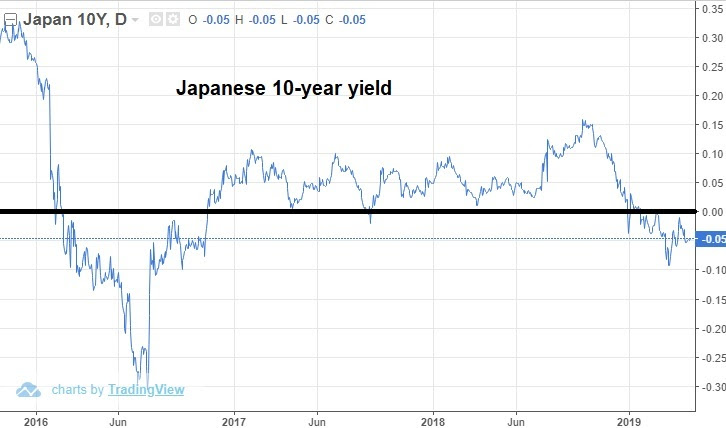

Now, let’s talk about the big mover of the day: interest rates. The 10-year yield traded to 2.96% today, closing in on 3% again.

We’ve discussed, many times, the role that Japan continues to play in our interest rate market. Despite 7 hikes by the Fed from the zero-interest-rate-era, our 10 year yield has barely budged. That’s, in large part, thanks to the Bank of Japan.

As I’ve said in the past, “Japan’s policy on pegging its 10-year yield at zero has been the anchor on global interest rates. Forcing their benchmark government bond yield back to zero, in a world where there has been upward pressure on interest rates, has meant that they can, and will, buy unlimited amounts of JGBs to get the job done. That equates to unlimited QE. When they finally signal a change to that policy, that’s when rates will finally move.”

With that in mind, there were reports over the weekend that the Bank of Japan may indeed signal a change in that “yield curve control” policy at their meeting next week. And global rates have been moving!

June 14, 5:00 pm EST

Tech stocks and small caps continue to behave like an economy that is about to take off.

The Nasdaq is now up 14% on the year. The Russell 2000 is up 10%. The S&P 500 (with more global exposure) is lagging it all, up just 4%.

Is it telling us that the investments in the U.S. are gaining more favor, relative to the rest of the world? Maybe. Is it telling us that capital is flowing toward the U.S. to align with Trump policies and away from those that may be harmed by being on the wrong side of Trump. Maybe.

With that said, we know Europe has been slowing. We know the “Italy-risk” presents another drag on that outlook. As such, the ECB followed the Fed’s hike yesterday with a rather dovish outlook this morning. Draghi laid out a timeline for following the Fed’s lead on normalization that was a little slower/ little later than expectations. That sent the dollar soaring, the euro plunging, and rates in Europe lower.

Tonight, we hear from the Bank of Japan. Remember, this is the lynchpin in keeping a lid on global interest rates. As long as they have the QE spigot wide-open, our yields (and therefore our consumer rates) will be well contained.

Japan’s policy on pegging its 10-year yield at zero has been the anchor on global interest rates. Forcing their benchmark government bond yield back to zero, in a world where there has been upward pressure on interest rates, has meant that they can, and will, buy unlimited amounts of JGBs to get the job done. That equates to unlimited QE. When they finally signal a change to that policy, that’s when rates will finally move.

June 11, 5:00 pm EST

Last week we stepped through all of the components of economic output and talked about the setup for positive surprises. Keep in mind, the economy is running at near a 3% pace already. And if Trumponomics is just in the early stages of materializing in the data on consumption, investment, government spending and exports, then we may be in for a big growth number.

On Friday we talked about the exports (i.e. the trade) component. On that note, the media was stirring over the combative tone from G7 events over the weekend. What I heard was the potential for big movement (i.e. gains on U.S. exports, which will drive gains in GDP). Trump went in and proposed taking down all trade barriers. That’s negotiating from an extreme. And that typically brings about movement. Quickly, trade partners were discussing “reducing” barriers.

With hotter than expected growth coming, how will that effect Fed policy?

We will soon see. The Fed meets this week. They continue their path of normalizing rates. They’ve hiked once in 2015, once in 2016, three times in 2017 and once, thus far, this year. The market is nearly fully pricing in a second hike for the year on Wednesday. And expectations are for another hike in September. We’ll see this week if they’re adjusting uptheir growth forecasts.

As for the rate path: Remember, Powell is a Trump appointee, and from what we’ve heard from him thus far, he sounds like someone that’s not going to risk chipping away at the recovery by jumping ahead with overly aggressive rate hikes. Unlike the last regime, he will likely take a “whites of inflation’s eyes” approach.

May 11, 3:00 pm EST

Over the past two Friday’s we’ve stepped events and conditions that have built the case that that “all-clear” signal has been given for stocks.

We are 91% through S&P 500 earnings for Q1 and the positive surprises have continued to roll in, on both earnings growth and revenue growth. Q1 GDP growth had a positive surprise, to reflect an economy that is running very close to 3% over the past three quarters. The important FAANG stocks all beat on earnings and beat on revenues for Q1. And the big jobs report last Friday did NOT come with a hot wage growth number, which keeps the inflation outlook tame.

Now we have very compelling technical confirmation that a resumption of the big secular bull trend for stocks is resuming. This correction has given everyone a long time to get on board. But it looks like the train is leaving the station.

Here’s a look at the S&P 500 ….

This bull trend in stocks from the oil-price crash induced lows of 2016 remains intact. The trendline tested and held three times in this recent correction, as did the 200-day moving average. And yesterday we had a big break of this trendline that represents this correction of the past three months. This has been textbook technical confirmation of a price correction within a strong bull trend.

Here’s the Dow chart we looked at on Wednesday …

And here’s the latest as we end the week, as the momentum from that trend break continues …

U.S. stocks are being valued right at the long-term P/E, at about 16 times forward earnings. Stocks in the UK, Germany and Japan are all trading closer to 13 times forward earnings. That’s cheap relative to long-term averages, and especially cheap (including U.S. stocks), in ultra-low interest rate environments. For perspective, Japanese stocks are recovering back toward the highest levels in more than 25 years, yet the forward P/E on Japanese stocks is closer to the lowest levels over the period. Stocks are cheap, and this correction has been a gift to get all of the onlookers on board.

January 22, 7:00 pm EST

We talked last week about the prospects of a government shutdown and the little-to-no impact it would likely have on markets.

Here we are, with a shutdown as we open the week, and stocks are on to new record highs. Oil continues to trade at the highest levels of the past three years. And benchmark global interest rates continue to tick higher.

As we look ahead for the week, fourth quarter earnings will start rolling in this week. But the big events of the week will be the Bank of Japan and European Central Bank meetings. The Bank of Japan (the most important of the two) meets tonight.

Remember, we’ve talked about the disconnect we’ve had in government bond yields, relative to the recovering global economy and strong asset price growth (led by stocks). And despite five Fed rate hikes, bond yields haven’t been tracking the moves made by the Fed either. The U.S. 10-year government bond yield finished virtually unchanged for the year in 2017.

That’s because the monetary policy in Japan has been acting as an anchor to global interest rates. Their policy of pegging their 10-year yield at zero, has created an open ended, unlimited QE program in Japan. That means, as the forces on global interest rates pulls Japanese rates higher, away from zero, they will, and have been buying unlimited amounts of Japanese Government Bonds (JGBs) to force the yield back toward zero. And they do it with freshly printed yen, which continues to prime the global economy with fresh liquidity.

So, as we’ve discussed, when the Bank of Japan finally signals a change to that policy, that’s when rates will finally move–and maybe very quickly.

If they choose, tonight, to signal an end of QE could be coming, even if it’s a year from now, the global interest rate picture will change immediately. With that in mind, here’s a look at the U.S. ten year yields going in …

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

December 19, 4:00 pm EST

Remember, the Fed met last week and hiked rates for the third time this year, and the fifth time in the post-crisis hiking cycle. But as we discussed, the big event for interest rates wasn’t last week, it’s this week.

The Bank of Japan meets on Wednesday and Thursday. Japan‘s policy on pegging their 10-year yield at zero has been the anchor on global interest rates (weighing on global interest rates). When they signal a change to that policy, that’s when rates will finally move – and maybe very quickly.

With that in mind, we have the stock market continuing to climb north of +20% on the year. Economic growth is going to get very close to 3% for the full year of 2017, and yet the benchmark longer term interest rates determined by the market are unchanged for the year. The yield on the 10 year Treasury is 2.43% this morning (ticking UP today). We came into the year at 2.43%.

Again, this is the flattening yield curve we discussed last week. For a world that is constantly looking for the next potential danger or signal for doom, the flattening of the yield curve has been the latest place they’ve been hanging their hats (as what they believe to be a predictor of recession). But those people seem happy to assume this yield curve indicator is driven by the same behaviors that have led to recessions in past economic periods, ignoring the unprecedented and coordinated global central bank manipulation that has gotten us here and continues to warp the interest rate market.

So now we have the Fed, which has been moving away from emergency policies. The ECB has signaled an end to QE next year. And the Bank of Japan is next in line — it’s a matter of when.

So how do things look going into this week’s meeting? We know the architect of Japan’s economic reform plan, Prime Minister Shinzo Abe, has just followed the American fiscal stimulus movement with a corporate tax cut of his own, but only for companies that will start raising wages for their employees. He said today that Japan is no longer in a state of deflation. The head of the Bank of Japan has said the economy is in “very good shape.” And that they would consider what is the best level of rate targets to align with changes n the economy, prices and financial conditions. The recent Tankan survey showed sentiment in the manufacturing community hitting decade and multi-decade highs.

But inflation continues to undershoot in Japan, as it is in the U.S. Japan is targeting a 2% inflation rate and is running at just 0.8% annualized.

So it’s unlikely that they will give any signal of taking the foot off of the gas this week. But that signal is probably not far off — maybe in January, after U.S. tax cuts are in effect. What does that mean? It means our market rates probably make an aggressive move higher early next year (10s in the mid 3s and rates on consumer loans probably jump 150 to 200 basis points higher).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click her

June 30, 2017, 7:00 pm EST Invest Alongside Billionaires For $297/Qtr

Without a doubt, there was a significant shift in the outlook on central bank monetary policy this week. In fact, the events of the week may represent the official market acceptance of the “end of the easy money” era.

Draghi told us deflation is over and reflation is on. Yellen told us we should not expect another financial crisis in our lifetimes. Carney at the Bank of England told us removal of stimulus is likely to become necessary, and up for debate “in the coming months.” And even the Finance Minister in Japan joined in, saying Japan was recovery from deflation.

With that, in a world where “reflation” is underway, rates and commodities lead the way.

Here’s a look at the chart on the 10-year yield again. We looked at this on Tuesday. I said, the “Bottom May Be In For Oil and Yields.” That was the dead bottom. Rates bounced hard off of this line we’ve been watching …

This reflation theme confirmed by central banks has put a bid under commodities…

That’s especially important for oil, which had been trading down to very dangerous levels, the levels that begin threatening the solvency of oil producers.

That’s a 9% bounce for oil from the lows of last week!

This all looks like the beginning of another leg of recovery for commodities and rates (with the catalyst of this central bank guidance). Which likely means a lower dollar (as we discussed earlier this week). And a quieter broad stock market (until growth data begins to reflect a break out of the sub 2% GDP funk).

Have a great weekend.

Join the Billionaire’s Portfolioto hear more of my big picture analysis and get my hand-selected, diverse stock portfolio following the lead of the best activist investors in the world.

May 8, 2017, 4:00pm EST Invest Alongside Billionaires For $297/Qtr

For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

Brexit. Russia. Trump’s protectionist threats. Trump’s inability to get policies legislated. The French election.

The bears, those looking for a recession around the corner and big slide in stocks, are losing ammunition for the story.

With the threat of instability from the French election now passed, these are two of the more intriguing catch-up trades.

Buffett essentially said at zero interest rates into perpetuity, the upside on the stock market (and any alternative asset class with return) is essentially infinite, as people are forced to find return by taking risk. Why you would buy a treasury bond that has no growth, and little-to-no yield and the same or worse balance sheet than high quality dividend stock.

This “forcing of the hand” (pushing investors into return producing assets) is an explicit objective by the interest rate policies of the Fed and the other major central banks of the world. They need us to buy stocks. They need us to spend money. They need economic growth.

If you have an brokerage account, and can read a weekly note from me, you can position yourself with the smartest investors in the world. Join us in The Billionaire’s Portfolio.