As we’ve discussed, the proxy on the “tech dominance” trade is Amazon. That’s the proxy on the stock market too. And it’s not going well. The President hammered Amazon again over the weekend, and again this morning.

Here’s what he said …

Remember, we had this beautiful heads-up on March 13, with the reversal signal in Amazon.

That signal we discussed in my March 13 note has now predicted this 15.8% decline in the fourth largest publicly traded company. And it’s dictating the continued correction in the broader market.

If you’re a loyal reader of this daily note, you’ll know we’ve been discussing this theme for the better part of the last year. The regulatory screws are tightening. And the tech giants, which have been priced as if they are, or would become, perfect monopolies, are now in the early stages of repricing for a world that might have more rules to follow, hurdles to overcome and a resurrection of the competition they’ve nearly destroyed.

As we know, Uber has run into bans in key markets. We’ve had the repeal of “net neutrality” which may ultimate lead big platforms like Google, Twitter, Facebook and Uber, to transparency of their practices and accountability for the actions of its users. Trump is going after Amazon, as a monopoly and harmful to the economy. Tesla, a money burning company, is being scrutinized for its inability to mass produce — to deliver on promises. For Tesla, if sentiment turns and people become unwilling to continue plowing money into a company that’s lost $6 billion over the past five years (while contributing to the $18 billion wealth of its CEO), it’s game over.

With that said, this all creates the prospects for a big bounce back in those industries that have been damaged by tech “disruption.” And this should make a stock market recovery much more broad-based than we’ve seen.

With the sharp decline in stocks today, we’ve retested and broken the 200-day moving average in the S&P 500. And we close, sitting on this huge trendline that describes the rise in stocks from the oil-crash induced lows of 2016.

Today we neared the lows of the sharp February decline. I suspect we’ll bottom out near here and begin the recovery. And that recovery should be fueled by very good Q1 earnings and a good growth number — brought to us by the big tax cuts.

We’ve talked quite a bit over the past year about this $100 oil thesis from the research-driven commodities investors Goehring and Rozencwajg.

As they said in their recent letter, “we remain firmly convinced that oil-related investments will offer phenomenal investment returns. It’s the buying opportunity of a lifetime.”

With that, let’s take a look at some favorite energy stocks of the most informed and influential billionaire investors:

David Einhorn of Greenlight Capital has about 5% of his fund in Consol Energy (CNX). Mason Hawkins of Southeastern Asseet Management is also in CNX. He has 9% of his fund in the stock, his third largest position. The last time oil was $100, CNX was a $36 stock. That’s more than a double from current levels.

Carl Icahn’s biggest position is in energy. He has 12% of his fund in CVR Energy. The last time oil was $100, CVI was $49. That’s 58% higher than current levels.

Paul Singer of Elliott Management’s third largest position is an oil play: Hess Corp. (HES). It’s a billion-dollar stake, and the stock was twice as valuable the last time oil prices were $100.

Andreas Halvorsen of Viking Global Investors has the biggest position in his $16-billion fund in EnCana Corp. (ECA). The stock was around $25 last time oil was $100. It currently trades at $14.

If you are hunting for the right stocks to buy, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers. You can add these stocks at a nice discount to where they were trading just a week ago.

With the big decline and wild swings in the stock market, earnings season has gotten little attention.

We’ve now heard from 80% of the companies in the S&P 500 on Q4. According to FactSet, 75% of the companies have beat on earnings. And 78% have had positive revenue surprises.

Now, earnings estimates are made to be broken. And they tend to be beaten at a rate of about 70% of the time. But the same cannot be said for revenues. This has been a key missing piece in the economic recovery. Companies have been cutting costs, refinancing and trimming headcount, all in an effort to manufacture margins and profitability. But revenues, the true gauge of business activity and demand, had been dead for the better part of the past decade.

It was just last year that we finally saw some decent revenue growth coming in from the earnings reports. And this most recent quarter, revenue growth is running at the hottest rate since FactSet has been keeping records. That’s a very good sign for the economic outlook.

And corporate earnings are running 15.2% higher than the same period the year prior. That’s the hottest earnings growth we’ve seen since 2011. More importantly, that’s four percentage points higher than analysts were projecting at the end of the year–with knowledge of the tax cut legislation.

With that said, remember, just last Friday, we had a moment during the day when the forward P/E on the S&P 500 hit 16.2. But if the fourth quarter is any indication, those forward earnings (estimates) will likely get ratcheted UP over the coming quarters, but will still undershoot. That will keep downward pressure on the P/E. Stocks are cheap.

If you are hunting for the right stocks to buy, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers. You can add these stocks at a nice discount to where they were trading just a week ago.

On Friday, stocks bottomed into two big technical levels: 1) the two-year rising trendline that represented the recovery from the lows of 2016, which were induced by the oil price crash, and 2) the 200-day moving average.

We’ve since seen a 5.5% bounce off of the bottom.

Interestingly, the market that has had so many people concerned over the past two weeks–interest rates–were tame and lower on the day. But only after printing a new high (at 2.90%, which is the highest since January of 2014).

That climb in rates, of course, has had everyone uptight about the inflation outlook. But the market you would expect to reflect inflation fears hasn’t been telling the inflation story at all. I’m talking about the price of gold. And gold has been lower, not higher, since stocks have fallen.

Here’s a look at that chart …

With this in mind, the psychology always changes when stocks go down. People search for stories to fit the price–for trouble to fit the price. Even some of the more rational market practitioners were succumbing to this over the weekend, trying to conjure up a negative scenario unfolding for markets.

Having been involved in markets for 20 years, I’ve seen, within both short- and long-term cycles, thousands of turning points, trend changes, phases of a cycles, trends and corrections of trends. Markets can and do have technical corrections. And they can and do correct for no reason, other than price.

So, for perspective, things are good. We will have the hottest economy this year that we’ve seen in a decade. The benchmark 10-year yield, at 2.90%, remains very low relative to history. That means, although borrowing costs are ticking higher, money is still cheap. Gas is cheap. Consumer and corporate balance sheets are as good as they’ve been in a long time. And we’ve just gotten a blue light special on stocks–marking down prices from 18 times to something closer to 16 times earnings. And with the prospects for earnings to come in better than expected, given influence of tax cuts, we are probably looking at a P/E on the S&P 500 forward earnings closer to 15.

If you are hunting for the right stocks to buy, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers. You can add these stocks at a nice discount to where they were trading just a week ago.

Two weeks ago there were signals that a correction was underway. First we had a swing back into positive yield territory for the German 5-year government bond. That was a significant marker for the end of the negative interest rate era and the end of global QE.

And with the outlook for rate normalization formalizing in the market, we should expect stock market growth to be driven from that point by earnings and dividends, and therefore economic growth. And then we had a perfect trigger lining up to set off the correction: earnings from the big tech giants. On script, Google missed. Apple disappointed on guidance, and the broad market sell-off began.

With that, when stocks broke down on February 2nd, we remembered that the stock market has had about a 10% decline on average, about once a year, over the past 70 years.

Then on Monday, the sell-off accelerated, and for a target in the S&P 500 we looked at this chart, which projected a reasonable spot to think we might find a bottom–around 2,560. We hit that on Friday and traded through to the 200-day moving average (2,539)–and we got an aggressive bounce.

Now, I’ve said a decline like this would make stocks cheap–“maybe something closer to 15 times forward earnings.” That sounded crazy two weeks ago. But guess what? We’re pretty darn close. At the lows on Friday, the P/E on earnings forecasted over the next four quarters was 16.2!

But as we know, Wall Street has a long history of underestimating earnings. That’s why about 70% of companies beat on earnings every quarter. And in this case, we’re talking about a huge earnings bump coming in the first quarter from the tax cuts. And Wall Street has barely bumped earnings expectations to incorporate that.

As said earlier this week, when the tax cut was in proposal stages, Citigroup estimated it would add $2 to S&P 500 earnings for every 1 percentage point cut in the tax rate. We’ve gone from 35% to 21%. With that, the forward four-quarter estimate for S&P 500 earnings, before the tax bill (in late November) was around $142.

If we add $28 in tax savings, we get $170. At the lows today in the S&P 500 that puts the P/E on a $170 in S&P 500 forward earnings at 14.8! That’s cheap relative to the long run historical P/E on stocks. And it’s extremely cheap in a world of low rates. And rates are still very low relative to history. And the low-rate environment will continue to motivate investors to seek higher returns in stocks–and pay higher valuations as stocks rebound. With hotter earnings and multiple expansion from here, we could reasonably see a 20%-30% rebound in stocks by year end.

Remember, the psychology always changes when stocks go down. People search for stories to fit the price–for trouble to fit the price. Rather than one of these stories leading to another major fallout, it’s a much higher probability that we are in the early innings of an economic boom, and stocks will be much higher than here in a year’s time. It’s time to be greedy while others are getting fearful.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

For the first time in a decade, the mood at the World Economic Forum in Davos was of optimism and opportunity. And Trump economic policies have had a lot to do with it.

That optimism has continued to drive markets higher this year: global stocks, global interest rates, global commodities – practically everything.

The S&P 500 is up nearly 7% on the year now — just a little less than a month into the New Year. And we’ve yet to see the real impact of tax incentives hit earnings and investment.

But, with the rising price of oil (now above $65), and improving consumption (on the better outlook), we will likely start seeing the inflation numbers tick up.

Now, what will be the catalyst to cap this very sharp run higher in stocks to start the year? It will probably be the first “hotter than expected” inflation number.

That would start the speculation that the Fed might need to move rates faster, and it might speed-up the exit talks from QE in Europe and Japan.

If the inflation outlook triggers a correction (which would be healthy), that would set the table for hotter earnings and hotter economic growth (coming down the pike) to ultimately drive the remainder of stock returns for the year.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

Yesterday we talked about the commodities bull market and the move underway in natural gas.

That all continued today, thanks in part to a comment by the U.S. Treasury Secretary, saying “obviously a weaker dollar is good for us.” When the dollar goes down, commodities prices tend to go up, since they are largely priced in dollars. As such, commodities were the top performers of the day – beginning to gain more momentum at multi-year highs.

But as we’ve seen from this chart, this recovery in commodities, which has dramatically lagged in the reflation trade, has a long way to go.

While the markets reacted as if Mnuchin, the Treasury Secretary, was talking down the dollar, the dollar is already in a long-term bear market cycle.

Remember, we looked at this chart (below) of the long-term dollar cycles back in June…

And I said, “if we mark the top of the most recent cycle in early January, this bull cycle has matched the longest cycle in duration (at 8.8 years) and comes in just shy of the long-term average performance of the five complete cycles. The most recent bull cycle added 47%. The average change over a long-term cycle has been 56%. This all argues that the dollar bull cycle is over. And a weaker dollar is ahead. That should go over very well with the Trump administration.”

The dollar is down about 8% since then and is breaking down technically now.

The dollar index is now down 14% in this new bear cycle. And these are the early innings. Based on the dollar cycle, it has a long way to go, and should last for another 5 to 7 years.

So, this dollar outlook is further support for the case for a big run in commodities we’ve been discussing. And as we observed yesterday, in the case of Chesapeake Energy (CHK), the second largest producer of natural gas in the country, the commodities stocks are still extremely underpriced if this scenario for commodities plays out.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

We talked last week about the prospects of a government shutdown and the little-to-no impact it would likely have on markets.

Here we are, with a shutdown as we open the week, and stocks are on to new record highs. Oil continues to trade at the highest levels of the past three years. And benchmark global interest rates continue to tick higher.

As we look ahead for the week, fourth quarter earnings will start rolling in this week. But the big events of the week will be the Bank of Japan and European Central Bank meetings. The Bank of Japan (the most important of the two) meets tonight.

Remember, we’ve talked about the disconnect we’ve had in government bond yields, relative to the recovering global economy and strong asset price growth (led by stocks). And despite five Fed rate hikes, bond yields haven’t been tracking the moves made by the Fed either. The U.S. 10-year government bond yield finished virtually unchanged for the year in 2017.

That’s because the monetary policy in Japan has been acting as an anchor to global interest rates. Their policy of pegging their 10-year yield at zero, has created an open ended, unlimited QE program in Japan. That means, as the forces on global interest rates pulls Japanese rates higher, away from zero, they will, and have been buying unlimited amounts of Japanese Government Bonds (JGBs) to force the yield back toward zero. And they do it with freshly printed yen, which continues to prime the global economy with fresh liquidity.

So, as we’ve discussed, when the Bank of Japan finally signals a change to that policy, that’s when rates will finally move–and maybe very quickly.

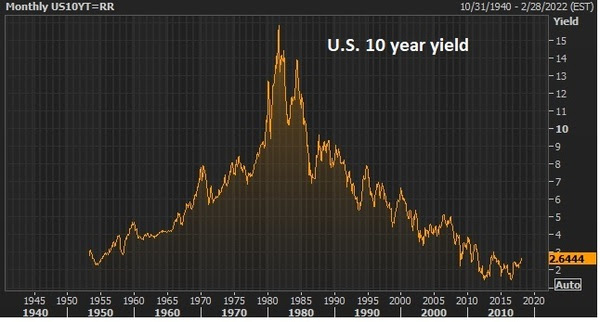

If they choose, tonight, to signal an end of QE could be coming, even if it’s a year from now, the global interest rate picture will change immediately. With that in mind, here’s a look at the U.S. ten year yields going in …

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

With a government shutdown over the weekend, today I want to revisit my note from last month (the last time we were facing a potential government shutdown) on the significance of the government debt load.

The debt load is an easy tool for politicians to use. And it’s never discussed in context. So the absolute number of $19 trillion is a guarantee to conjure up fear in people – fear that foreigners may dump our bonds, fear that we may have runaway inflation, fear that the economy is a house of cards. So that fear is used to gain negotiating leverage by whatever party is in a position of weakness. For the better part of the past decade, it was used by the Republican party to block policies. And now it’s being used by the Democratic party to try to block policies.

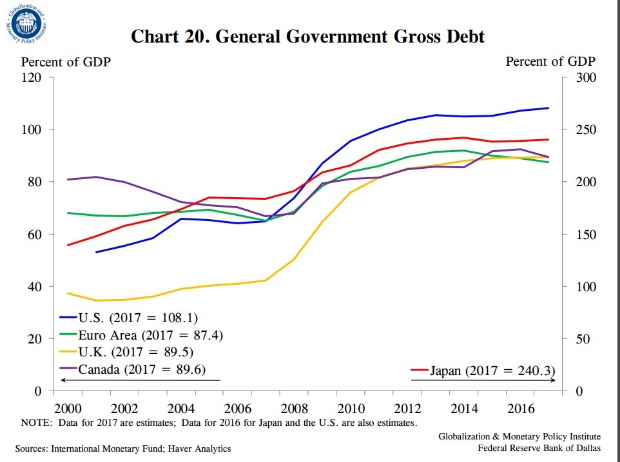

Now, the federal debt is a big number. But so is the size of our economy – both about $19 trillion. And while our debt/GDP has grown over the past decade, the increase in sovereign debtrelativetoGDP, has been a global phenomenon, following the financial crisis. Much of it has to do with the contraction in growth and the subsequent sluggish growth throughout the recovery (i.e. the GDP side of the ratio hasn’t been carrying its weight).

You can see in the chart below, the increasing debt situation isn’t specific to the U.S.

Now, we could choose to cut spending, suck it up, and pay down the debt. That’s called austerity. The choice of austerity in this environment, where the economy is fragile, and growth has been sluggish for the better part of ten years, would send the U.S. economy back into recession. Just ask Europe. After the depths of the financial crisis, they went the path of tax hikes and spending cuts, and by 2012 found themselves back in recession and a near deflationary spiral – they crushed the weak recovery that the European Central Banks (and global central banks) had spent, backstopped and/or guaranteed trillions of dollars to create.

The problem, in this post-financial crisis environment: if the major economies in the world sunk back into recession (especially the U.S.), it would certainly draw emerging markets (and the global economy, in general) back into recession. And following a long period of unprecedented emergency monetary policies, the global central banks would have limited-to-no ammunition to fight a deflationary spiral this time around.

Now, all of this is precisely why the outlook for the U.S. and global economy changed on election night in 2016. We now have an administration that is focused on growth, and an aligned Congress to overwhelm the political blocking. That means we truly have the opportunity to improve our relative debt-load through growth.

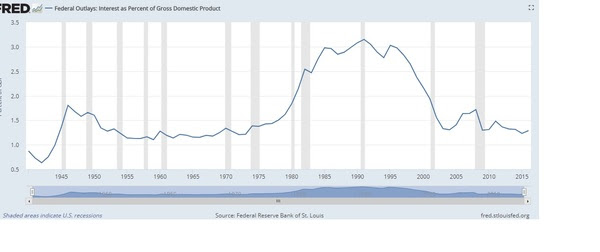

In the meantime, despite all of the talk, our ability to service the debt load is as strong as it’s been in forty years (as you can see in the chart below). And our ability to refinance debt is as strong as it’s been in sixty years.

For help building a high potential portfolio, follow me in our Forbes Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.

government shutdown, washington, wall street, economy

Last week we talked about the big adjustment we should expect to come in the inflation picture. With oil above $60 and looking like much higher prices are coming, and with corporate tax cuts set to fuel the first material growth in wages we’ve seen in a long time (if not three decades), this chart (inflation expectations) should start moving higher…

And with that, market interest rates should finally make a move. As we discussed last week, we will likely have a 10-year yield with a “3” in front of it before long.

Yields have already popped nearly a quarter point since the beginning of the year. But that’s just (finally) reflecting the December Fed rate hike. What hasn’t been reflected in rates, as it has in stocks, is the different growth and wage pressure outlook this year, thanks to the tax cut. Last year, people could argue it wasn’t going to happen. This year, it’s in motion. And the impact is already showing up. We should expect it to show in the inflation data, sooner rather than later.

With that, today we’re knocking on the door of a big breakout in rates (as you can see in the chart below) — which comes in at 2.65%…

As we’ve discussed, the anchor for the benchmark U.S. 10-year yield (and for global rates), even in the face of a more optimistic global economic growth outlook, has been Japan’s unlimited QE (driven by its policy to peg its 10-year at a yield of zero). On that note, last week, the former head of the central bank in India, Raghuram Rajan (a highly respected former central banker), said he thinks both Europe and Japan will exit emergency policies sooner than people think. That’s a positive statement on the global economy and a warning that global rates should finally start moving.

For help building a high potential portfolio, follow me in our Billionaire’s Portfolio subscription service, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio of highest conviction, billionaire-owned stocks is up close to 50% over the past two years. You can join me here and get positioned for a big 2018.