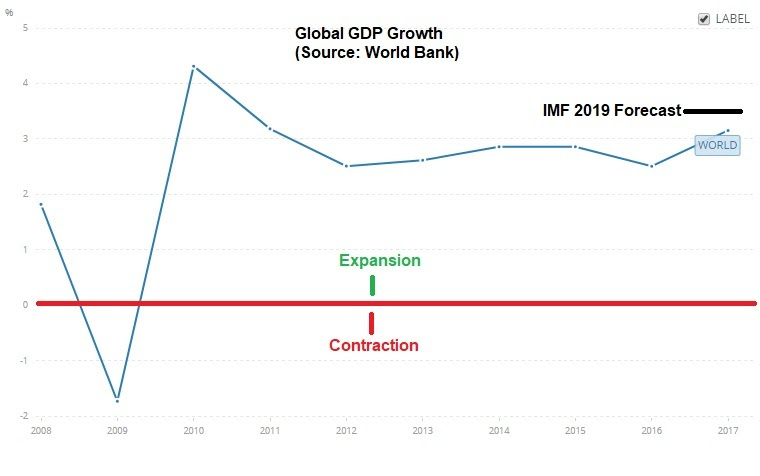

The financial media has been focused on Davos this week — the host of the World Economic Forum, which is attended by the world’s top global government and corporate leaders.

Coming off of an ugly December for global financial markets, it’s no surprise the conversation is all about “slowdown.” It’s an odd conversation, given that the U.S. economy is growing at 3%, corporate earnings are running at record levels, inflation is low and unemployment is low. Even the IMF could only justify a small markdown on their 2019 global GDP forecast — from an already high level.

For perspective, the IMF is now looking for 3.5% growth for 2019. Here’s how that looks relative to the past ten years ….

So, what’s the story?

As we discussed yesterday, it’s China, and the pressure of tariffs and reform demands on a vulnerable large economy that’s already drowning.

And the broader view is that trade is being hampered by the Trump/China standoff – and therefore dragging on growth. With that in mind, listening to some interviews from Davos, the one that stuck out to me was the DHL CEO (the world’s leading mail and logistics company). He said trade is not at all on the back foot, rather its flowing more than ever before.

So, the global growth slowdown talk is all about what might happen, not about what is happening. It’s about risk. With that, if China does make the concessions necessary to get a deal done (and they seem to have few options), we may end up getting a big upside surprise in global growth – especially given the very accomodative global monetary policy backdrop.

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

Back in May, the populist movement that gave us Grexit, Brexit and then the Trump election, gave us a new government in Italy with an “Italy first” agenda.

Italy first, means EU second. And that puts the future of the European Union and the European Monetary Union in jeopardy. Today, the new government made that clear by rejecting EU fiscal constraints, in favor of running a bigger deficit spending.

This puts the game of poker the European Union has been playing since the financial crisis erupted, front and center (again).

As we discussed back in May, this story is looking a lot like Greece, which used the threat of leaving the euro as leverage to negotiate some relief from austerity and reforms. It was messy, but it gave them a stick, in a world where the creditors (the ECB, Eurogroup and IMF) had been burying the weak economies in Europe in harsh austerity since the financial crisis.

As the third largest euro zone constituent, Italy brings a lot more leverage in negotiating, in this case, the EU rulebook. We may see this all result, finally, in a relaxing of the fiscal constraints that have suppressed the economic recovery in the euro zone in the post-Great Recession era. And Italy’s pushback may lead the way for a euro-wide fiscal stimulus campaign — following the lead of Trumponomics.

A better economy has a way of solving a lot of problems. And Europe has a lot of problems.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

We have a currency devaluation in Turkey that is shaking up markets. Let’s talk about what’s happening and why (if at all) it matters for the big picture outlook.

First, here’s a look at the Turkish lira chart (orange line moving up means a stronger U.S. dollar, weaker lira)…

Now, the problems in Turkey aren’t new. The country is economically fragile. But the collapse in the currency probably has more to do with its leadership – and the erosion of democracy in Turkey.

There are a lot of people comparing Turkey’s currency crisis to the Thai Baht devaluation in 1997 — which ultimately ignited a currency crisis in Asia, which culminated in a sovereign default in Russia. That’s the fear: a currency crisis turning into a contagion of sovereign debt defaults.

But Thailand was about economic policy – specifically, the Thai currency policy. Speculators attacked to close the valuation gap between the central bank managed currency and its economy.

This Turkey issue looks more like the collapse in the Russian Ruble in late 2014. That was geopolitically driven. Back in 2014, Putin was forcing his way into Ukraine – an affront to the Western world. This was viewed as a proxy war against the West. That led to capital flight out of Russia and speculative attack on the currency.

With this chart on the Ruble (the orange line going up means a stronger dollar and weaker ruble), Russia was quickly made vulnerable and on a sovereign debt default watch.

But like Turkey, the contagion risk was driven by Russia’s foreign currency denominated debt (primarily euro denominated debt owed to European banks).

With that said, the world wasn’t “normal” in 2014, nor is it now. Remember, the European Central Bank remains in quantitative easing mode. That means, we should expect central bank (or policy) intervention (if needed) to quell any shock risks that could come from European bank exposure to Turkish debt. So the ECB’s “ready to act” commitment of the post-financial crisis era should calm fears of contagion.

As for Turkey, the crippling effects of the currency attack should put pressure on the freshly re-elected Ergodan (i.e. should make him vulnerable to an uprising).

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

Remember, the Fed met last week and hiked rates for the third time this year, and the fifth time in the post-crisis hiking cycle. But as we discussed, the big event for interest rates wasn’t last week, it’s this week.

The Bank of Japan meets on Wednesday and Thursday. Japan‘s policy on pegging their 10-year yield at zero has been the anchor on global interest rates (weighing on global interest rates). When they signal a change to that policy, that’s when rates will finally move – and maybe very quickly.

With that in mind, we have the stock market continuing to climb north of +20% on the year. Economic growth is going to get very close to 3% for the full year of 2017, and yet the benchmark longer term interest rates determined by the market are unchanged for the year. The yield on the 10 year Treasury is 2.43% this morning (ticking UP today). We came into the year at 2.43%.

Again, this is the flattening yield curve we discussed last week. For a world that is constantly looking for the next potential danger or signal for doom, the flattening of the yield curve has been the latest place they’ve been hanging their hats (as what they believe to be a predictor of recession). But those people seem happy to assume this yield curve indicator is driven by the same behaviors that have led to recessions in past economic periods, ignoring the unprecedented and coordinated global central bank manipulation that has gotten us here and continues to warp the interest rate market.

So now we have the Fed, which has been moving away from emergency policies. The ECB has signaled an end to QE next year. And the Bank of Japan is next in line — it’s a matter of when.

So how do things look going into this week’s meeting? We know the architect of Japan’s economic reform plan, Prime Minister Shinzo Abe, has just followed the American fiscal stimulus movement with a corporate tax cut of his own, but only for companies that will start raising wages for their employees. He said today that Japan is no longer in a state of deflation. The head of the Bank of Japan has said the economy is in “very good shape.” And that they would consider what is the best level of rate targets to align with changes n the economy, prices and financial conditions. The recent Tankan survey showed sentiment in the manufacturing community hitting decade and multi-decade highs.

But inflation continues to undershoot in Japan, as it is in the U.S. Japan is targeting a 2% inflation rate and is running at just 0.8% annualized.

So it’s unlikely that they will give any signal of taking the foot off of the gas this week. But that signal is probably not far off — maybe in January, after U.S. tax cuts are in effect. What does that mean? It means our market rates probably make an aggressive move higher early next year (10s in the mid 3s and rates on consumer loans probably jump 150 to 200 basis points higher).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

Brexit. Russia. Trump’s protectionist threats. Trump’s inability to get policies legislated. The French election.

The bears, those looking for a recession around the corner and big slide in stocks, are losing ammunition for the story.

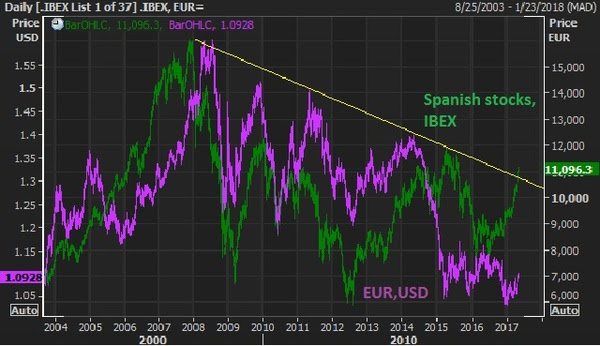

With the threat of instability from the French election now passed, these are two of the more intriguing catch-up trades.

In the chart above, the green line is Spanish stocks (the IBEX). U.S., German and UK stocks have not only recovered the 2007 pre-crisis highs but blown past them — sitting on or near (in the case of UK stocks) record highs. Not only does the French vote punctuate the break of this nine year downtrend, but it has about 45% left in it to revisit the 2007 highs. And the euro, in purple, could have a dramatic recovery with the cloud of French elections lifted, which was an imminent threat to the future of the single currency.Next … Japanese stocks. While the attention over the past five months has been diverted toward U.S. politics and policies, the Bank of Japan has continued with unlimited QE. As U.S. rates crawl higher, it pulls Japanese government bond yields with it, moving the Japanese market interest rate above and away from the zero line. Remember, that’s where the BOJ has pegged the target for it’s 10 year yield – zero. That means they buy unlimited bonds to push the yield back down. That means they print more and more yen, which buys more and more Japanese stocks.

The Nikkei has been one of the biggest movers over the past couple of weeks (up almost 10%) since it was evident that the high probability outcome in the French election was a Macron win.Again, German, U.S., and UK stocks are at or near record highs. The Nikkei has been trailing behind and looks to make another run now, with 25,000 in sight.If you need more convincing that stocks can go much higher, Warren Buffett reiterated over the weekend that this low interest rate environment and outlook makes stocks “dirt cheap.” Last year he made the point that when interest rates were 15% [in the early 1980s], there was enormous pull on all assets, not just stocks. Investors have a lot of choices at 15% rates. It’s very different when rates are zero (or still near zero). He said, in a world where investors knew interest rates would be zero “forever,” stocks would sell at 100 or 200 times earnings because there would be nowhere else to earn a return.

Buffett essentially said at zero interest rates into perpetuity, the upside on the stock market (and any alternative asset class with return) is essentially infinite, as people are forced to find return by taking risk. Why you would buy a treasury bond that has no growth, and little-to-no yield and the same or worse balance sheet than high quality dividend stock.

This “forcing of the hand” (pushing investors into return producing assets) is an explicit objective by the interest rate policies of the Fed and the other major central banks of the world. They need us to buy stocks. They need us to spend money. They need economic growth.

If you have an brokerage account, and can read a weekly note from me, you can position yourself with the smartest investors in the world. Join us in The Billionaire’s Portfolio.

This will be an interesting week. We had almost three months of optimism priced into global markets following the November 8th elections. And then the tide turned when Trump gave his speech to the join sessions of Congress.

This is the buy-the-rumor sell-the-fact phenomenon we’ve discussed. People bought on anticipation of a big policy shift. And now they’re taking profit (raising cash) waiting to see it all executed — the prove-it-to-me phase.

I think we’re beginning to see the same phenomenon unfold in the Brexit saga. Brexit came before Trump, but the cycle has been slower and longer. Much like the Trump trend, the Brexit news started with an initial “sell everything” on the fear of the unknown, but soon thereafter, the “buy on anticipation of something better” prevailed. But it’s looking very vulnerable now to a turn in the tide.

On Friday, we looked at this next chart. This trend higher in UK stocks looks much like the Trump trend in U.S. stocks – a nice 45 degree climb from June of last year.

But as we discussed on Friday, the “prove-it-to-me” phase looks set to arrive this week in the Brexit story. With that, here’s what the chart looks like today …

This nine-month trend line in UK stocks gave way today – in part because of the softening in expectations about Trump policies, but largely because the UK Prime Minister is expected to officially notify the European Union on Wednesday, of the UK’s exit from the EU. Again, this would start the clock on the two year wind-down of the UK constituency in the EU. And the official negotiations will begin, on what the UK/EU relationship will look like – namely, on trade.

Expect the negotiations to be ugly in the early stages. Why? Because there is a lot to lose if it looks too easy. The future of the European Union and the common currency (the euro) hang in the balance on these negotiations. The most important job of EU officials, at this stage, is keeping other EU members from hitting the eject button, following the lead of the UK. A domino effect of exits would kill the EU and it would be the end of the euro. And that would have huge, destabilizing global ramifications.

With all of this in mind, it’s very likely that after long period of ultra-low volatility in markets, things will be a little more dicey in the months ahead. That should keep pressure on yields and should keep the correction in U.S. stocks intact.

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

One of the best investors on the planet, David Tepper, was on CNBC this morning. Let’s talk about how he sees the world and how he is positioned.

What I appreciate about Tepper: He’s a common sense guy.

And his common sense view of the world happens to be in alignment with the view and themes we discuss here every day. So he agrees with me – another thing I appreciate about him.

As you know, Wall Street and the media are always good at overcomplicating the investment environment with their day-to-day hyper analysis. Because of that, they tend to forge a path that moves further and further away from the simple realities of the big picture. That’s actually good. Because it creates opportunity for those that can avoid those distractions.

Right now, as we’ve discussed, the big picture is straight forward. We have a President that wants deregulation, tax cuts and a big infrastructure spend. And we have a Congress in place that can approve it. And this all comes at a time when the world has been in a decade long economic slog following the global financial crisis – in desperate need of growth. With that, we have a Fed that still has rates at very, very low levels. And the ECB and BOJ are still priming the pump with QE.

This is precisely Tepper’s view. He says the bowl is still full, i.e. the stimulus from the monetary policy side is still full, and now we get stimulus coming in from the fiscal side. What more could you ask for (my words) to pump up growth and asset prices, which will likely spill over into a pop in global growth. Still, people are underestimating it. And as he says, the Fed is underestimating it.

Are there risks? Yes. But the probability of growth, with the above in mind, well outweighs the probable downside scenarios. What about execution risk? Even if tax reform and infrastructure are slow to come, Tepper says deregulation is a done deal. It drives earnings and “animal spirits.”

He likes stocks. He likes European stocks. And I think he really likes Japanese stocks, but he stopped short of talking about it (my deduction).

Among the risks: Inflation picking up too fast, which would require the Fed to move faster, which could choke off growth (undo or neutralize fiscal stimulus).

This is why, among other reasons, Tepper’s favorite trade is short bonds. – i.e. higher interest rates. If he’s right and economic growth has a big pop, he wins. If the risk of hotter inflation materializes and rates move faster, he wins.

For context, this is the guy that literally changed global investing sentiment in late 2010 when he sat in front of a camera on CNBC, in a rare high profile TV interview (maybe first), when investing sentiment was all but destroyed by the global financial crisis and the various landmines that kept popping up. Tepper said in a very confident voice that the Fed, by telegraphing a second round of QE, had just given us all a free put on stocks (i.e. the Fed is protected the downside, it’s a greenlight to buy stocks). For all of the market jockeys that were constantly focusing on the many problems in the world, that commentary from Tepper, for some reason, woke them up.

For perspective on Tepper: Here’s a guy that is probably the best investor in the modern era. He’s returned between 35%-40% annualized (before fees) for more than 20 years. He made $7.5 billion in 2009 betting on financial stocks that most people thought were going bankrupt. And he was telling everyone that what the Fed is doing will make ‘everything’ go up. It sparked, in 2010, what is known as the “Tepper rally” in stocks.

When Tepper speaks it’s often smart to listen. And he likes the Trump effect!

In our Billionaire’s Portfolio, we’re positioned in a portfolio of deep value stocks that all have the potential to do multiples of what broader stocks do — all stocks owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and we’ll send you our recently recorded portfolio review that steps through every stock in our portfolio, and the opportunities in each.

Yesterday we looked at the slide in yields (U.S. market interest rates — the 10-year Treasury yield). That continued today, in a relatively quiet market.

Let’s take a look at what may be driving it.

If you take a look at the chart below, you can see the moves in yields and gold have been tightly correlated since election night: gold down, yields up.

As markets began pricing in a wave of U.S. growth policies, in a world where negative interest rates were beginning to emerge, the benchmark market-interest-rate in the U.S. shot up and global interest rates followed. The German 10-year yield swung from negative territory back into positive territory. Even Japan, the leader of global negative interest rate policy early last year, had a big reversal back into positive territory.

And as growth prospects returned, people dumped gold. And as you can see in the chart above of the “inverted price of gold,” the rising line represents falling gold prices.

Interestingly, gold has been bouncing pretty aggressively since mid December. Why? To an extent, it’s pricing in some uncertainty surrounding Trump policies. And that would also explain the slow down and (somewhat) slide in U.S. yields. In fact, based on that chart above and the gold relationship, it looks like we could see yields back below 2.10%. That would mean a break of the technical support (the yellow line) in this next chart …

Another reason for higher gold, lower yields (i.e. higher bond prices), might be the capital flight in China. Where do you move money if you’re able to get it out in China? The dollar, U.S. Treasuries, U.S. stocks, Gold.

The data overnight showed the lowest levels reached in the countries $3 trillion currency reserve stash in 6 years. That, in large part, comes from the Chinese central banks use of reserves to slow the decline of their currency, the yuan. Of course a weakening yuan only inflames U.S. trade rhetoric.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

We ended last week with a very strong jobs report, yet the measure of wage pressure was soft. That, for the near term, reduces expectations on how aggressive the Fed might be (but not a lot).

Still, the 10-year yield has drifted lower to start the week. It was 2.50% Friday afternoon. Today it’s closer to 2.40%. When the 10-year yield drifts lower, mortgage rates drift a little lower, back very close to 4% today. This all helps two of the most important tools the Fed has been focused on for the past eight years to drive economic recovery: stocks and housing.

The Trump administration, like the Fed, will need both stocks and housing to continue higher to maintain confidence in the economy, and in the agenda.

Now, on Friday I said Trump was hosting Japan’s Prime Minister Abe in Florida over the weekend for a round of golf at Mar-a-Lago. It looks like it’s this coming weekend, instead.

Interestingly, this comes as the Trump administration made a conscious effort on Friday to refocus the messaging from a protectionist narrative to an economic growth narrative.

Abe will be entering this meeting with President Trump under some peripheral scrutiny about trade imbalances. Japan runs about a $60 billion surplus with the United States. That’s about on par with Mexico, which has become a target for Trump in recent weeks. Still, as I said last week, it’s peanuts compared to China, and that’s where the Trump administration’s real attention lies.

Nonetheless, Abe is expected to come in with a plan to balance trade with the U.S., which includes working together on a big U.S. infrastructure program. And there is still considerable sensitivity surrounding the value of the yen (the Japanese currency).

As we know, under Abenomics, the yen has devalued by about 40% against the dollar. But as China has done often over the past decade, as they have headed into big meetings with global leaders, Japan seems to be walking its currency up in the days heading into the Abe/Trump meeting.

You can see in the chart above, the dollar has been in decline against the yen this year (the orange line falling represents a weaker dollar, stronger yen). The top in the USD/JPY exchange rate this year came when Trump’s chief trade negotiator was named on January 3rd. Robert Lighthizer worked in the Reagan administration and happened to be behind stiff tariffs imposed on Japan during that era on electronics.

Trump’s tough talk on trade, and the market’s continued focus on upcoming elections in Europe (that threaten to continue the trend of nationalism and protectionism) have stocks in Japan and Europe diverging from the strength we’re seeing in U.S. stocks. The Dow is above 20k. Meanwhile, Japanese stocks are still 10% off of the 2015 highs. German stocks are 7% off of 2015 highs.

But as I’ve said, growth solves a lot of problems. In addition to the underlying current of a better performing U.S. economy (with the pro-growth agenda in the pipeline), the data is already improving in both Germany and Japan. I suspect that Europe and Japan will soon be cleared from the fray of the trade protectionist rhetoric, and we’ll start seeing major European stock markets and the Japanese stock market climbing, and ultimately putting up a big number in 2017.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

The Trump agenda continues to dominate the market focus as we entered the second week of Trumponomics.

To this point the market focus has been on the pro-growth agenda. With that, stocks have been higher, yields have been higher, the dollar has been higher, and global commodities have been broadly rising. Meanwhile, gold (the fear trade) has been falling and the VIX has been falling, toward ultra-low levels. The VIX, like gold, is a good market indicator of uncertainty and/or fear.

Let’s talk about the VIX…

The VIX measures the implied volatility of options on the S&P 500. This is a key component in the price investors pay for downside protection on their portfolios.

So what is implied volatility? Implied volatility measures both actual volatility and the options market maker community’s expectations (or perception of certainty) about future volatility. When market makers feel confident about the stability in markets, implied vol is lower, which makes the price of options cheaper. When they aren’t confident in stability, implied vol goes up, which makes the price of an option go up. To compensate those that are taking the other side of your trade, for the lack of predictability, you pay a premium.

With that in mind, on Friday, the VIX traded to the lowest levels since the days before the failure of Lehman Brothers. That indicates that the market had (or has) become a believer that pro-growth policies, combined with ultra-easy central bank policies have created a buffer against the downside in stocks. But that perception of downside risk is changing today, with the more vocal uprising against Trump social policies. You can see the spike (in the far right of the chart) today…

So as big money managers were closing the week last Friday, looking at Dow 20,000+ and a VIX sliding toward levels not too far from pre-crisis levels, buying downside protection was dirt cheap. This morning, they’re paying quite a bit more for that protection.

With that said, this pop in the VIX and the Dow trading off by more than 100 points today gets a lot of attention. But is there justification to think that market turbulence will begin to reflect the turbulence and division in public opinion toward Trump policies? Just gauging the extent of the market reaction from the VIX today, it’s unlikely. The chart below is the longer term view of the VIX.

My observations: The VIX has had a small bounce from very, very low levels. On an absolute basis, vol is still very cheap. When there is real fear in the air, real uncertainty about the future, you can see from the spikes in the longer term chart above, the premium for the unknown gets priced in quickly and aggressively. Given that there has been virtually no risk premium priced into the market for any falter in the Trump Presidency, or the execution of Trump policies, the moves today have been very modest. And gold (as I write) is barely changed on the day.

We are likely entering an incredible era for investing, which will be an opportunity for average investors to make up ground on the meager wealth creation and retirement savings opportunities of the past decade. For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

This will be an interesting week. We had almost three months of optimism priced into global markets following the November 8th elections. And then the tide turned when Trump gave his speech to the join sessions of Congress.

This will be an interesting week. We had almost three months of optimism priced into global markets following the November 8th elections. And then the tide turned when Trump gave his speech to the join sessions of Congress.