With two big central bank meetings behind us this week, and the Fed on deck for next week, let’s remind ourselves of where the global central banks stand, more than 10 years after the crisis.

There’s one thing we know, following the events of the past decade: The global central banks will do “whatever it takes” to preserve stability and manufacture economic growth. As long as global economies remain interconnected (which they are), this is the script they (global central banks, in coordination) will follow. They crossed the line long ago. There’s no turning back.

So, with all of the continual talk in past years about another big shock or “shoe to drop,” people have failed to acknowledge the key difference between the depths of the financial crisis and now. Back then, we didn’t know how policymakers would respond. That’s a lot of uncertainty. Now we know. They will change the rules when they need to. That removes a lot of uncertainty.

With this in mind, remember on January 4th, in response to an ugly December for the stock market, the Fed marched out Bernanke, Yellen and Powell to walk back on the tightening cycle. For a world that was expecting four rote rate hikes this year, that was an official response – effectively easing, intermeeting.

Next up, the Bank of Japan. They met this week. With the ECB now done with QE, the BOJ is now the lone global economic shock absorber. Not only have they been executing on their massive QQE plan since 2013, in 2016 they crafted a plan that gave them greenlight to do unlimited QE as long as their 10-year government bond yield drifted above the zero line. So, as global yields pull Japanese yields higher, the BOJ responds by buying bonds in unlimited amounts to push it all back down. That has been the anchor on global interest rates. And given that they see inflation continuing to run well below their target of 2%, through 2020, the BOJ will be printing for the foreseeable future (remaining that anchor on global interest rates).

What about Europe? A few months ago, some thought the ECB might be following the Fed footsteps — with a first post-QE rate hike by the middle of this year. Today, Draghi put that to bed, saying risks are now to the downside, and that the market has it right pricing in a rate hike for next year – assuming all goes well. But Draghi also wants us to know that the ECB stands ready to act if the economy falters (i.e. they can/will go the other way).

So, for perspective on where the global economy stands, we still have central banks pulling the levers to keep it all together. That’s why Trump’s big and bold fiscal stimulus and structural reform was/is absolutely necessary. And that’s why the rest of the world will likely have to follow the U.S., with fiscal stimulus, if we are to ultimately and sustainably put the crisis period behind us.

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

We’ve talked this week about the pressure that rising U.S. market interest rates are putting on emerging markets.

The fear surrounding the big 3% marker for U.S. 10-year yields is that 3% may quickly become 4%. And a 4% yield, much less a quick adjustment in this key benchmark interest rate, would cause some problems.

Not only does it create capital flight out of areas of the world where rates are low, and monetary policy is heading the opposite direction of the Fed, but a quick move to a 4% yield on the 10-year would certainly cloud the U.S. economic growth picture, as higher mortgage and consumer borrowing rates would start chipping away at economic activity.

With that said, we may have a reprieve with the action today in the bond market.

As we head into the weekend, today we get a softening in the rates market. And that came with a big technical reversal pattern (an outside day).

You can see in the chart above, the engulfing range of the day. This technical phenomenon, when closing near the lows, is a very good predictor of tops and bottoms in markets, especially with long sustained trends.

I suspect we may have seen some global central bank buyers of our Treasurys today (which puts downward pressure on yields) to take a bite out of the momentum. We will see if this quiets the rate market next week, for a drift back down to 3%. That would calm some of the nerves in global currencies, and global markets in general.

We talked yesterday about the building pressure in emerging markets, driven by weakening currencies and rising dollar-denominated oil prices.

With that bubbling up as a potential shock risk, gold hasn’t exactly been telling the story of elevated risks.

You can see in this chart above, since the tax cuts were passed in late 2017, rates have been rising (the purple line). This is a hotter economy, pick-up in inflation story. And, as it should, gold stepped higher with rates all along–until the last few weeks. You can see the divergence in the chart above.

I suspect we’ll see gold snap back to reflect some increasing market risks, and especially to reflect a world where central banks are beginning to finally see inflation pressures build. The gold bugs loved gold when inflation was dead. And now that it’s building, they are surprisingly very quiet.

We’ve talked about the stock market’s discomfort with the 3% mark in rates. People have been concerned about whether the U.S. economy can withstand higher rates–the impact on credit demand and servicing. That fear seems to be subsiding.

But often the risk to global market stability is found where few are looking. That risk, now, seems to be bubbling up in emerging market currencies. We have a major divergence in global monetary policies (i.e. the Fed has been normalizing interest rates while the rest of the world remains anchored in emergency level interest rates). That widening gap in rates, creates capital flight out of low rate environments and in to the U.S.

That puts upward pressure on the dollar and downward pressure on these foreign currencies. And the worst hit in these cases tend to be emerging markets, where foreign direct investment in these countries isn’t very loyal (i.e. it comes in without much commitment and leaves without much deliberation).

You can see in this chart of the Brazilian real, it has been ugly …

Oil has become the potential breaking point here. At $40-oil maybe these countries hang in there until the global economic recovery heats up to the point where they can begin raising rates without crushing growth (and with a closing rate gap, their currencies begin attracting capital again). But at $70-oil, their weak currencies make their dollar-denominated energy requirements very, very expensive. They’ve had nearly a double in oil over the past ten months, and a 15% drop in their currency since January (in the case of Brazil).

Something to watch, as a lynchpin in this EM currency drama, is the Hong Kong dollar. Hong Kong has maintained a trading band on its currency since 2005 that is now sitting on the top of the band, requiring a fight by the central bank to maintain it. If they find that spending their currency reserves on defending their trading band is a losing proposition, and they let the currency float, then we could have another shock event for global markets, as these EM currencies adjust and their foreign-currency-denominated debt becomes a default risk. This all may force the rest of the global economy to start following the Fed’s lead on interest rates earlier then they would like to (to begin closing that rate gap, and avoid a shock event).

Remember, the Fed met last week and hiked rates for the third time this year, and the fifth time in the post-crisis hiking cycle. But as we discussed, the big event for interest rates wasn’t last week, it’s this week.

The Bank of Japan meets on Wednesday and Thursday. Japan‘s policy on pegging their 10-year yield at zero has been the anchor on global interest rates (weighing on global interest rates). When they signal a change to that policy, that’s when rates will finally move – and maybe very quickly.

With that in mind, we have the stock market continuing to climb north of +20% on the year. Economic growth is going to get very close to 3% for the full year of 2017, and yet the benchmark longer term interest rates determined by the market are unchanged for the year. The yield on the 10 year Treasury is 2.43% this morning (ticking UP today). We came into the year at 2.43%.

Again, this is the flattening yield curve we discussed last week. For a world that is constantly looking for the next potential danger or signal for doom, the flattening of the yield curve has been the latest place they’ve been hanging their hats (as what they believe to be a predictor of recession). But those people seem happy to assume this yield curve indicator is driven by the same behaviors that have led to recessions in past economic periods, ignoring the unprecedented and coordinated global central bank manipulation that has gotten us here and continues to warp the interest rate market.

So now we have the Fed, which has been moving away from emergency policies. The ECB has signaled an end to QE next year. And the Bank of Japan is next in line — it’s a matter of when.

So how do things look going into this week’s meeting? We know the architect of Japan’s economic reform plan, Prime Minister Shinzo Abe, has just followed the American fiscal stimulus movement with a corporate tax cut of his own, but only for companies that will start raising wages for their employees. He said today that Japan is no longer in a state of deflation. The head of the Bank of Japan has said the economy is in “very good shape.” And that they would consider what is the best level of rate targets to align with changes n the economy, prices and financial conditions. The recent Tankan survey showed sentiment in the manufacturing community hitting decade and multi-decade highs.

But inflation continues to undershoot in Japan, as it is in the U.S. Japan is targeting a 2% inflation rate and is running at just 0.8% annualized.

So it’s unlikely that they will give any signal of taking the foot off of the gas this week. But that signal is probably not far off — maybe in January, after U.S. tax cuts are in effect. What does that mean? It means our market rates probably make an aggressive move higher early next year (10s in the mid 3s and rates on consumer loans probably jump 150 to 200 basis points higher).

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

We have big central bank meetings this week. Let’s talk about why it matters (or maybe doesn’t).

The Fed, of course, has been leading the way in the move away from global emergency policies.

But they’ve only been able to do so (raising rates and reducing their balance sheet) because major central banks in Europe and Japan have been there to pick up where the Fed left off, subsidizing the global economy (pumping up asset prices and pinning down market interest rates) through massive QE programs.

The QE in Japan and Europe has kept borrowing rates cheap (for consumers, corporates and sovereigns) and kept stocks moving higher (through outright purchases and through backstopping against shock risks, which makes people more confident to take risk).

But now economic conditions are improving in Europe and Japan. And we have fiscal stimulus coming in the U.S., into an economy with solid fundamentals. As we’ve discussed, this sets up for what should be an economic boom period in the U.S. And that will translate into hotter global growth. So the tide has turned.

With that, global interest rates, which have been suppressed by these QE programs, will start moving higher when we get signals from the key players, that an end of QE and zero interest rates is coming. The European Central Bank has already reduced its QE program and set an end date for next September. That makes the Bank of Japan the most important central bank in the world, right now. And that makes the meeting next week at the Bank of Japan the most important central bank event.

Let’s talk a bit more about, why?

Remember, last September, the Bank of Japan revamped it’s massive QE program which gave them the license to do unlimited QE. They announced that they would peg the Japanese 10-year government bond yield at ZERO.

At that time, rates were deeply into negative territory. In that respect, it was actually a removal (a tightening) of monetary stimulus in the near term — the opposite of what the market was hoping for, though few seemed to understand the concept. But the BOJ saw what was coming.

This move gave the BOJ the ability to do unlimited QE, to keep stimulating the economy, even as growth and inflation started moving well in their direction.

Shortly thereafter, the Trump effect sent U.S. yields on a tear higher. That move pulled global interest rates higher too, including Japanese rates. The Japanese 10-year yield above zero, and that triggered the BOJ to become a buyer of as many Japanese Government Bonds as necessary, to push yields back down to zero. As growth and the outlook in Japan and globally have improved, and as the Fed has continued tightening, the upward pressure on rates has continued, which has continued to trigger more and more QE from the BOJ – which only reinforces growth and the outlook.

So we have the BOJ to thank, in a pretty large part, for the sustained improvement in the global economy over the past year.

As for global rates: As long as this policy at the BOJ appears to have no end, we should expect U.S. yields to remain low, despite what the Fed is doing. But when the BOJ signals it may be time to think about the exit doors, global rates will probably take off. We’ll probably see a 10-year yield in the mid three percent area, rather than the low twos. That will likely mean mortgage rates back well above 5%, car loans several percentage points higher, credit card rates higher, etc.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

With a Fed decision queued up for tomorrow, let’s take a look at how the rates picture has evolved this year.

The Fed has continued to act like speculators, placing bets on the prospects of fiscal stimulus and hotter growth. And they’ve proven not to be very good.

Remember, they finally kicked off their rate “normalization” plan in December of 2015. With things relatively stable globally, the slow U.S. recovery still on path, and with U.S. stocks near the record highs, they pulled the trigger on a 25 basis point hike in late 2015. And they projected at that time to hike another four times over the coming year (2016).

Stocks proceeded to slide by 13% over the next month. Market interest rates (the 10 year yield) went down, not up, following the hike — and not by a little, but by a lot. The 10 year yield fell from 2.33% to 1.53% over the next two months. And by April, the Fed walked back on their big promises for a tightening campaign. And the messaging began turning dark. The Fed went from talking about four hikes in a year, to talking about the prospects of going to negative interest rates.

That was until the U.S. elections. Suddenly, the outlook for the global economy changed, with the idea that big fiscal stimulus could be coming. So without any data justification for changing gears (for an institution that constantly beats the drum of “data dependence”), the Fed went right back to its hawkish mantra/ tightening game plan.

With that, they hit the reset button in December, and went back to the old game plan. They hiked in December. They told us more were coming this year. And, so far, they’ve hiked in March and June.

Below is how the interest rate market has responded. Rates have gone lower after each hike. Just in the past couple of days have, however, we returned to levels (and slightly above) where we stood going into the June hike.

But if you believe in the growing prospects of policy execution, which we’ve been discussing, you have to think this behavior in market rates (going lower) are coming to an end (i.e. higher rates).

As I said, the Hurricanes represented a crisis that May Be The Turning Point For Trump. This was an opportunity for the President to show leadership in a time people were looking for leadership. And it was a chance for the public perception to begin to shift. And it did. The bottom was marked in Trump pessimism. And much needed policy execution has been kickstarted by the need for Congress to come together to get the debt ceiling raised and hurricane aid approved. And I suspect that Trump’s address to the U.N. today will add further support to this building momentum of sentiment turnaround for the administration. With this, I would expect to hear a hawkish Fed tomorrow.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

As I said on Friday, people continue to look for what could bust the economy from here, and are missing out on what looks like the early stages of a boom.

We constantly hear about how the fundamentals don’t support the move in stocks. Yet, we’ve looked at plenty of fundamental reasons to believe that view (the gloom view) just doesn’t match the facts.

Remember, the two primary sources that carry the megahorn to feed the public’s appetite for market information both live in economic depression, relative to the pre-crisis days. That’s 1) traditional media, and 2) Wall Street.

As we know, the traditional media business, has been made more and more obsolete. And both the media, and Wall Street, continue to suffer from what I call “bubble bias.” Not the bubble of excess, but the bubble surrounding them that prevents them from understanding the real world and the real economy.

As I’ve said before, the Wall Street bubble for a very long time was a fat and happy one. But the for the past ten years, they came to the realization that Wall Street cash cow wasn’t going to return to the glory days. And their buddies weren’t getting their jobs back. And they’ve had market and economic crash goggles on ever since. Every data point they look at, every news item they see, every chart they study, seems to be viewed through the lens of “crash goggles.” Their bubble has been and continues to be dark.

Also, when we hear all of the messaging, we have to remember that many of the “veterans” on the trading and the news desks have no career or real-world experience prior to the great recession. Those in the low to mid 30s onlyknow the horrors of the financial crisis and the global central bank sponsored economic world that we continue to live in today. What is viewed as a black swan event for the average person, is viewed as a high probability event for them. And why shouldn’t it? They’ve seen the near collapse of the global economy and all of the calamity that has followed. Everything else looks quite possible!

Still, as I’ve said, if you awoke today from a decade-long slumber, and I told you that unemployment was under 5%, inflation was ultra-low, gas was $2.60, mortgage rates were under 4%, you could finance a new car for 2% and the stock market was at record highs, you would probably say, 1) that makes sense (for stocks), and 2) things must be going really well! Add to that, what we discussed on Friday: household net worth is at record highs, credit growth is at record highs and credit worthiness is at record highs.

We had nearly all of the same conditions a year ago. And I wrote precisely the same thing in one of my August Pro Perspective pieces. Stocks are up 17% since.

And now we can add to this mix: We have fiscal stimulus, which I think (for the reasons we’ve discussed over past weeks) is coming closer to fruition.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

The noise surrounding the Trump administration continues by the day, as the media tries desperately to prosecute the elected President at daily briefings.The chaos and dysfunction message is loud, but markets aren’t hearing it. The real story is very different. Stocks continue to surge. Stock market volatility continues to sit 10-year (pre-crisis) lows. The interest rate market is much higher than it was before the election, but now quiet and stable. Gold, the fear-of-the-unknown trade, is relatively quiet. This all looks very much like a world that believes a real economic expansion is underway, and that a long-term sustainable global economic recovery has supplanted the shaky post-crisis (central bank-driven) recovery that was teetering back toward recession.

Why is the messaging so different? Remember, the financial media and Wall Street are easily distractible. Not only do they have short attention spans, but they’ve been trained throughout their careers to find new stories to obsess about. They need to interpret, pontificate, strategize to feel valued. Approaching their jobs with the idea that a slow moving dominant theme is at work is just too boring.

This is the disconnect between markets and the narrative. We have major central banks around the world that continue to print money. These central banks buy assets with that freshly printed money. That means, stocks, bonds, commodities go higher. And now we have everyone’s fate (the global economy) tied to the outcome of new policies from the leading economy in the world – efforts to restore sustainable growth through structural reform and fiscal stimulus. That hopeful outlook does nothing but underpin the rise in asset prices (stocks, bonds, commodities, real estate).

Yesterday we got a look under the hood of the portfolios of the biggest money managers in the world, via their 13F filings (required quarterly portfolio disclosures to the SEC). It’s been clear that the biggest and best, embrace this big theme, and have been aggressively positioning to take advantage of the very bullish proposed policy tailwinds for stocks, which are: 1) a corporate tax rate cut, which will go right to the bottom line for profitable companies. Not surprisingly, which stocks have been leading the way in the climb in the indicies? The one’s that make a lot of money (Apple, Microsoft, Google). 2) a repatriation tax holiday that will bring back trillions of dollars onshore, to be paid back to shareholders and put to work in the economy through investment and projects. 3) a trillion dollar infrastructure spend that, regardless of how difficult it may be to legislate, should happen in one form or another.

Among the reports on portfolio holdings yesterday, we heard from the Swiss National Bank. As I said above, don’t forget there are still central banks deeply entrenched in QE and, beyond local government bonds, are buying foreign assets (in large amounts). Switzerland’s central bank has more freshly printed money to put to work every quarter, and has been increasing their allocation to equities dramatically – $80 billion of which is now (as of the end of Q1) in U.S. stocks! That’s a 29% bigger stake than they had at the end of 2016. The SNB is the world’s eighth biggest public investor.

So keep this big theme in mind: Central banks remain involved, but the baton has been passed, from a central bank-driven recovery to a fiscal stimulus-driven recovery. And everyone needs it to work.

Follow This Billionaire To A 172% Winner

In our Billionaire’s Portfolio, we have a stock in our portfolio that is controlled by one of the top billion dollar activist hedge funds on the planet. The hedge fund manager has a board seat and has publicly stated that this stock is worth 172% higher than where it trades today. And this is an S&P 500 stock!

Even better, the company has been constantly rumored to be a takeover candidate. We think an acquisition could happen soon as the billionaire investor who runs this activist hedge fund has purchased almost $157 million worth of this stock over the past year at levels just above where the stock is trading now.

So we have a billionaire hedge fund manager, who is on the board of a company that has been rumored to be a takeover candidate, who has adding aggressively over the past year, on a dip.

For the skeptics on the bull market in stocks and the broader economy, the reasons to worry continue to get scratched off of the list.

Brexit. Russia. Trump’s protectionist threats. Trump’s inability to get policies legislated. The French election.

The bears, those looking for a recession around the corner and big slide in stocks, are losing ammunition for the story.

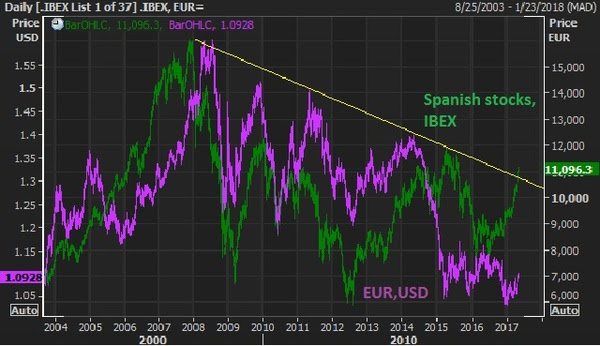

With the threat of instability from the French election now passed, these are two of the more intriguing catch-up trades.

In the chart above, the green line is Spanish stocks (the IBEX). U.S., German and UK stocks have not only recovered the 2007 pre-crisis highs but blown past them — sitting on or near (in the case of UK stocks) record highs. Not only does the French vote punctuate the break of this nine year downtrend, but it has about 45% left in it to revisit the 2007 highs. And the euro, in purple, could have a dramatic recovery with the cloud of French elections lifted, which was an imminent threat to the future of the single currency.Next … Japanese stocks. While the attention over the past five months has been diverted toward U.S. politics and policies, the Bank of Japan has continued with unlimited QE. As U.S. rates crawl higher, it pulls Japanese government bond yields with it, moving the Japanese market interest rate above and away from the zero line. Remember, that’s where the BOJ has pegged the target for it’s 10 year yield – zero. That means they buy unlimited bonds to push the yield back down. That means they print more and more yen, which buys more and more Japanese stocks.

The Nikkei has been one of the biggest movers over the past couple of weeks (up almost 10%) since it was evident that the high probability outcome in the French election was a Macron win.Again, German, U.S., and UK stocks are at or near record highs. The Nikkei has been trailing behind and looks to make another run now, with 25,000 in sight.If you need more convincing that stocks can go much higher, Warren Buffett reiterated over the weekend that this low interest rate environment and outlook makes stocks “dirt cheap.” Last year he made the point that when interest rates were 15% [in the early 1980s], there was enormous pull on all assets, not just stocks. Investors have a lot of choices at 15% rates. It’s very different when rates are zero (or still near zero). He said, in a world where investors knew interest rates would be zero “forever,” stocks would sell at 100 or 200 times earnings because there would be nowhere else to earn a return.

Buffett essentially said at zero interest rates into perpetuity, the upside on the stock market (and any alternative asset class with return) is essentially infinite, as people are forced to find return by taking risk. Why you would buy a treasury bond that has no growth, and little-to-no yield and the same or worse balance sheet than high quality dividend stock.

This “forcing of the hand” (pushing investors into return producing assets) is an explicit objective by the interest rate policies of the Fed and the other major central banks of the world. They need us to buy stocks. They need us to spend money. They need economic growth.

If you have an brokerage account, and can read a weekly note from me, you can position yourself with the smartest investors in the world. Join us in The Billionaire’s Portfolio.

With a Fed decision queued up for

With a Fed decision queued up for

The noise surrounding the Trump administration continues by the day, as the media tries desperately to prosecute the elected President at daily briefings.The chaos and dysfunction message is loud, but markets aren’t hearing it. The real story is very different. Stocks continue to surge. Stock market volatility continues to sit 10-year (pre-crisis) lows. The interest rate market is much higher than it was before the election, but now quiet and stable. Gold, the fear-of-the-unknown trade, is relatively quiet. This all looks very much like a world that believes a real economic expansion is underway, and that a long-term sustainable global economic recovery has supplanted the shaky post-crisis (central bank-driven) recovery that was teetering back toward recession.

The noise surrounding the Trump administration continues by the day, as the media tries desperately to prosecute the elected President at daily briefings.The chaos and dysfunction message is loud, but markets aren’t hearing it. The real story is very different. Stocks continue to surge. Stock market volatility continues to sit 10-year (pre-crisis) lows. The interest rate market is much higher than it was before the election, but now quiet and stable. Gold, the fear-of-the-unknown trade, is relatively quiet. This all looks very much like a world that believes a real economic expansion is underway, and that a long-term sustainable global economic recovery has supplanted the shaky post-crisis (central bank-driven) recovery that was teetering back toward recession.