We get the big jobs report tomorrow morning.

We’ve already seen a significant decline in job openings in the JOLTS report this week — the lowest number of job openings in two years.

On Wednesday, the ADP jobs report for August (published by the private payroll company) came in at sub 200k. That’s about half of the post-pandemic monthly average.

And the “main event” of jobs reports, the government report due tomorrow, is expected to show about 170k jobs created in August. That’s below the average monthly job growth for the (slow economic growth) decade prior to the pandemic.

Bottom line: The job market seems to have normalized (finally), in no small part due to the sobering of the workforce from the many anti-work incentives of that past three years.

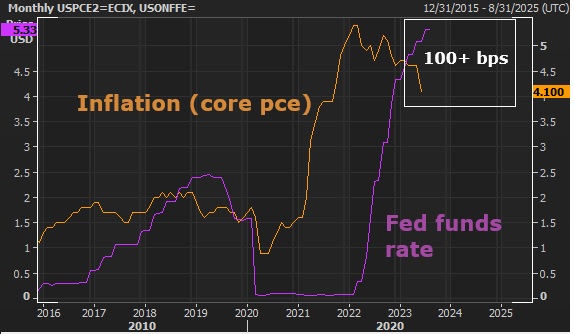

That said, while the Fed’s focus on jobs, over the past year, has been mostly about attempts to suppress wage growth, we are indeed seeing hot wage growth.

But as you can see in the chart above, the Fed tightening campaign and (moreover) the Fed’s persistent threats to destroy jobs have reversed what could have been a dangerous upward wage spiral (which would threaten a self-reinforcing price spiral).

Interestingly, in today’s small business jobs report, small business owners are expecting to raise compensation in the coming months. And they are now more concerned about retaining and attracting good talent, and much less concerned, compared to a year ago, about labor costs.

So wages are finally moving higher, to close the gap with higher prices.

What about the inflation risk from higher wages?

Importantly, we’re getting the inflationary offset of productivity gains.

Remember, we talked about this in my note last week (here). Despite some of the hottest wage gains we’ve seen in decades, the annual growth in the cost per unit of output was just 1.6%, in the most recent quarter.

That’s lower than the average unit labor cost of the 20-year period prior to the Global Financial Crisis. And it’s thanks to productivity growth.

Also remember, we are just in the early days of maybe the most productivity enhancing technological advancement of our lifetime: generative AI.

On that note, the CEO of Salesforce, which partners with 150,000 companies around the world, talked over and over again on his recent earnings call about the “incredible new levels of productivity“ its customers will see from generative AI.