Back in July, we talked about the significance of the President of the European Commission coming to Washington to make a deal on trade. That was a big day for Trump’s fight to level the playing field on global trade.

Why? Because concessions out of Europe paved the way to more concessions globally.

That’s what we’re getting. Fast forward a little less than a month and now we have China (the center of the global trade dispute universe) coming back to the table on trade negotiations with the U.S.

This is what happens when you negotiate from a position of strength. Trump has the leverage of a strong economy, and the credibility to act on tough threats. And that is bringing about progress. Trading partners risk being left behind in the global economic recovery if they don’t play ball.

So we should expect “movement” from China. And movement equals success.

With that, as I said, I suspect that will be the catalyst to get stocks back on the path toward double-digit gains by year-end.

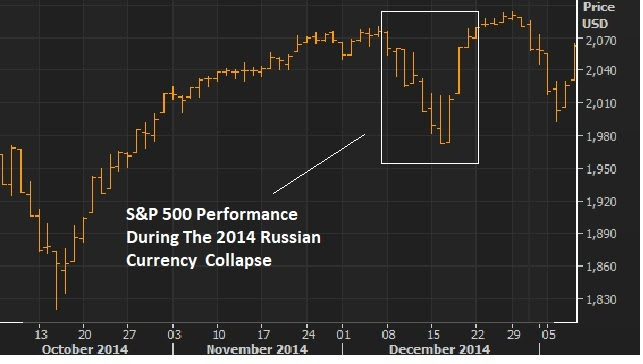

On Tuesday, we looked at the similarities between the recent currency collapse in Turkey, and the 2014 collapse of the Russian ruble.

And we looked at this chart of how the S&P 500 behaved back in 2014.

The S&P 500 is the proxy on global market stability. And stocks were shaken on Russia back in 2014. When the ruble collapsed, U.S. stocks lost 5% of its value in just 7 days.

But the decline was fully recovered in just 3 days.

Given the similarities of these two currency crises (a currency attack on a bad behaving leader), I thought we might see the same behavior in stocks this time. And that’s what we appear to be getting – a shallower decline but a swift recovery.

So, why the quick recovery?

As we also discussed on Tuesday, while the Turkish lira has been the center of attention in the financial media, the real reason global markets were shaking had more to do with China.

If a currency crisis that started in Turkey ended in China, there would be big geopolitical fallout.

As we’ve discussed over the past month, the biggest risk from China is a big one-off devaluation. That would stir up a response from other big trading partners (i.e. Europe and Japan), where they would likely coordinate to blocktrade from China all together. That’s where things would get very ugly and likely (ultimately) culminate in a military war.

But the probability of that outcome was reduced yesterday. We had news that a China delegation would travel to the U.S. to re-open trade negotiations. They’re coming back to the table.

So we should expect concessions from China. That’s good news for the globlal economy and for global stability. And that news drove the big bounce in stocks yesterday, which continued today. I suspect this will be the catalyst to get stocks back on the path toward a double-digit gains by year-end.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

We talked yesterday about the sharp currency devaluation in Turkey over the past few days. The Lira bounced aggressively today, which soothes some fears in global markets.

As I said, many have made comparisons to the Asian currency crisis of the late 90s, and have speculated on the potential for the events in Turkey to ultimately destabilize global markets. But as we discussed yesterday, this looks more like the 2014 currency attack on the Russian ruble — a geopolitically-driven crippling of an economy with bad behaving leadership.

With that in mind, here’s what happened to U.S. stocks back in 2014, when the ruble lost 5% of its value (vs the dollar) in just 7 days. But the decline was fully recovered in just 3 days.

U.S. stocks have been the proxy for global market stability throughout the past decade (the crisis and post-crisis era). So, for perspective on just how shaky the Turkey influence is being perceived, the S&P 500 sits just one percent off of all-time highs at today’s close.

Remember, the ECB stands ready to plug any holes necessary in European bank exposure to Turkish debt. That euro-denominated debt has been the risk people immediately homed in on.

The real question is, will this (currency crisis) ultimately end in China, with a revaluation of the yuan, or perhaps a free-floating yuan?

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

We have a currency devaluation in Turkey that is shaking up markets. Let’s talk about what’s happening and why (if at all) it matters for the big picture outlook.

First, here’s a look at the Turkish lira chart (orange line moving up means a stronger U.S. dollar, weaker lira)…

Now, the problems in Turkey aren’t new. The country is economically fragile. But the collapse in the currency probably has more to do with its leadership – and the erosion of democracy in Turkey.

There are a lot of people comparing Turkey’s currency crisis to the Thai Baht devaluation in 1997 — which ultimately ignited a currency crisis in Asia, which culminated in a sovereign default in Russia. That’s the fear: a currency crisis turning into a contagion of sovereign debt defaults.

But Thailand was about economic policy – specifically, the Thai currency policy. Speculators attacked to close the valuation gap between the central bank managed currency and its economy.

This Turkey issue looks more like the collapse in the Russian Ruble in late 2014. That was geopolitically driven. Back in 2014, Putin was forcing his way into Ukraine – an affront to the Western world. This was viewed as a proxy war against the West. That led to capital flight out of Russia and speculative attack on the currency.

With this chart on the Ruble (the orange line going up means a stronger dollar and weaker ruble), Russia was quickly made vulnerable and on a sovereign debt default watch.

But like Turkey, the contagion risk was driven by Russia’s foreign currency denominated debt (primarily euro denominated debt owed to European banks).

With that said, the world wasn’t “normal” in 2014, nor is it now. Remember, the European Central Bank remains in quantitative easing mode. That means, we should expect central bank (or policy) intervention (if needed) to quell any shock risks that could come from European bank exposure to Turkish debt. So the ECB’s “ready to act” commitment of the post-financial crisis era should calm fears of contagion.

As for Turkey, the crippling effects of the currency attack should put pressure on the freshly re-elected Ergodan (i.e. should make him vulnerable to an uprising).

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

The Nasdaq continued to slide today. Stock indices tend to go down a lot faster than they go up. The tech giant-driven Nasdaq was up over 15% year-to-date, just a few days ago, and has now given up more than 4% from the highs.

Not surprisingly, as people run for the exit doors on the big tech giants (taking profits), we’re seeing money rotate into the blue-chip value stocks.

The Dow and S&P 500 did much better than the Nasdaq today, which continues to slowly correct the big performance gap of the year (where the Nasdaq was up 15% at one point, while the DJIA was flat on the year).

Now, the biggest event of the week for markets may take place tonight. We hear from the Bank of Japan on monetary policy. We’ve discussed, many times, the role that Japan continues to play in our interest rate market.

Despite seven hikes by the Fed from the zero-interest-rate-era, our 10-year yield has barely budged. That’s, in large part, thanks to the Bank of Japan. Japan’s policy on pegging its 10-year yield at ZERO has been the anchor on global interest rates.

As I’ve said, when they finally signal a change to that policy, that’s when (our) rates will finally move. And that may be tonight. There is speculation that they may adjust UP that target on their 10-year yield. That would represent a dialing back of the BOJ’s QE program, which would signal the initial steps of exiting the crisis-era QE program.

What would that do? If the BOJ does indeed adjust their “yield curve control” policy, it should send global interest rates higher. That would put our ten-year yields back above 3%, which has been a level that has caused some uneasiness in markets. This time around, a move back above three percent would reflect a steepening U.S. yield curve which may be perceived as a positive, especially for those that have been concerned about the potential of seeing an inverted yield curve (i.e. a recession indicator).

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

As we end the week, let’s take a look at a few charts ….

We had the first look at Q2 GDP today. Here’s an updated look at the chart of the average four-quarter annualized growth rate we looked at

yesterday ….

This number will be formally revised two more times, but the “advance” number came in at 4.1%. Yesterday we talked about the prospects for the highest four-quarter annualized growth rate since 2006. We just missed it, in this first reading. But the Q1 number was revised UP to 2.2%, so adding in today’s Q2 number, and we get 3.1% four-quarter average annualized growth. Only for a moment, in 2010, was it better (at 3.15%).

I suspect we will see a bigger number in the coming Q2 revisions. And if sentiment on trade indeed bottomed out on Wednesday, with the EU concessions, we will likely have a big Q3 growth number coming.

That steadily rising trend, since the election, in the four-quarter average growth rate is a big deal. With that, I would call the above chart, the most important chart of the week…

Let’s look at the second most important chart of the week ….

I’ve been making the case that the massive Nasdaq outperformance, relative to the Dow, would begin correcting. In the chart above, you can see that it’s starting (Dow moving up, Nasdaq moving down). And it’s being led by strength in the blue chips following strong Q2 earnings, and weakness in two of the big tech giants (Netflix and Facebook) following big misses. With that, Facebook has quickly revisited levels of early May (which should give us all perspective on how aggressive this run in the tech giants has been over the past two months).

The question: Is it “peak Zuck?”

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

Tomorrow we get the second quarter GDP number. We’ve gone from a consensus view that didn’t believe in the economic momentum, or in the value of fiscal stimulus, to a consensus view that is now looking for more than 4% annualized growth for the second quarter. The switch has flipped in just the past few months.

As a goal for the economy, we hear the 3% growth number thrown around quite a bit. That’s right around long-term trend growth (trend growth is a little higher). But the GDP report that gets the most attention is a quarterly annualized number, which is more of a reflection of what the economy would look like if we moved forward over the next few quarters with similar economic activity. That can be a very volatile number. And we can see big numbers, in good economies and in bad economies. This is where the politicians like to find ambiguity to argue over. The pro-Trumpers will say we’re growing at 3%, something Obama never achieved. And the Obama defenders will point to several 3%+ annualized quarters in the Obama era.

What’s more informative is the average annualized growth over the past four quarters. That’s where you can see smoother trends and considerable improvements in the Trumponomics world.

On that note, we may finally hit that 3% number tomorrow. If the GDP number comes in tomorrow at the Atlanta Fed’s expectations (4.5%), we will have the hottest growth since June 2006.

A 4.5% second quarter number would put the four-quarter average annualized growth at 3.175%–the highest since the pre-financial crisis days. You can also see in the chart, the steady improvement in growth since the election, first driven by the optimism of pro-growth policies, and now driven by policy execution, as deregulation and tax cuts are working through the system.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

Last week Larry Kudlow, the White House Chief Economic Advisor, hinted that Jean-Claude Juncker (head of European Commission) would be coming to Washington with some concessions on trade.

As I write, we’ve yet to hear the results of the Trump/Juncker meeting today, but this could be a major turning point in the perception of the U.S. trade offensive. Movement equals success. And in that case, concessions out of Europe may pave the way to more concessions globally. That signal could trigger a big rally in global markets.

One particular market to watch is copper. Copper is the first place you should look if you think the world is escaping the slugglish post-crisis growth period, and possibly entering an economic boom period. It has been sensitive to the global trade disputes. A clearing of that, would resume what should be a multi-year bull market in copper.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

As we’ve discussed, tech and small-caps (the Nasdaq and the Russell 2000) have been big outperformers on the year, compared to blue-chip stocks. But today seemed like an exhaustive move in that divergence.

There was a clear rotation out of the small-caps (which finished down on the day) and into the blue chips (the Dow finished up nicely on the day). And the red-hot Nasdaq reversed from new record highs to finish flat.

Trump tweeted this morning that tariffs are bringing trade parters to the negotiating table. He seems to be confident that his meeting with EU Chief Jean-Claude Juncker tomorrow will result in concessions from Europe. And there seems to be movement on a new NAFTA deal too. Add this to more good earnings hitting from second quarter earnings season, and it’s enough to get big investment managers moving back into the blue-chip multinationals.

Remember, we’ve been watching this chart. The Dow still has a long way to go, to recover the record highs of earlier this year. But the technical breakout of this corrective downtrend has broken.

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

We have a big earnings week. The tech giants report, along with about a third of the S&P 500. And we get our first look at Q2 GDP.

As we’ve stepped through the year, we’ve had a price correction in stocks, following nearly a decade of central bank policies that propped up stocks. This correction made sense, considering central banks were finally able to make the hand-off to a U.S. led administration that had the will and appetite (and alignment in Congress) to relax fiscal constraints and force the structural reform necessary to promote an economic boom.

From there, for stocks, it became a “prove-it to me” market. Let’s see evidence of this “hand-off” is working — evidence the fiscal stimulus is working. That came in the form of first quarter earnings. This showed us clear benefits of the corporate tax cut. The earnings were hot, and stocks began a recovery.

The next steps, as fiscal stimulus works through the economy, we’ve needed to see that the uptick in sentiment (from the pro-growth policies) is translating into better demand and economic activity. So, with Q2 earnings we should start seeing better revenue growth, companies investing and hiring. And we should see positive surprises beginning to show up in the economic data.

We’re getting it. Almost nine out of ten companies reporting thus far have beat (lofty) earnings expectations. And about eight out of ten have beat on revenues. This week will be important, to solidify that picture. And though many of the economists all along the way of the past year didn’t see big economic growth coming, it has been steadily building since Trump was elected, and the Q2 number should push us to over 3% annual growth (averaging that past four quarters).

Now, let’s talk about the big mover of the day: interest rates. The 10-year yield traded to 2.96% today, closing in on 3% again.

We’ve discussed, many times, the role that Japan continues to play in our interest rate market. Despite 7 hikes by the Fed from the zero-interest-rate-era, our 10 year yield has barely budged. That’s, in large part, thanks to the Bank of Japan.

As I’ve said in the past, “Japan’s policy on pegging its 10-year yield at zero has been the anchor on global interest rates. Forcing their benchmark government bond yield back to zero, in a world where there has been upward pressure on interest rates, has meant that they can, and will, buy unlimited amounts of JGBs to get the job done. That equates to unlimited QE. When they finally signal a change to that policy, that’s when rates will finally move.”

With that in mind, there were reports over the weekend that the Bank of Japan may indeed signal a change in that “yield curve control” policy at their meeting next week. And global rates have been moving!

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.