|

|

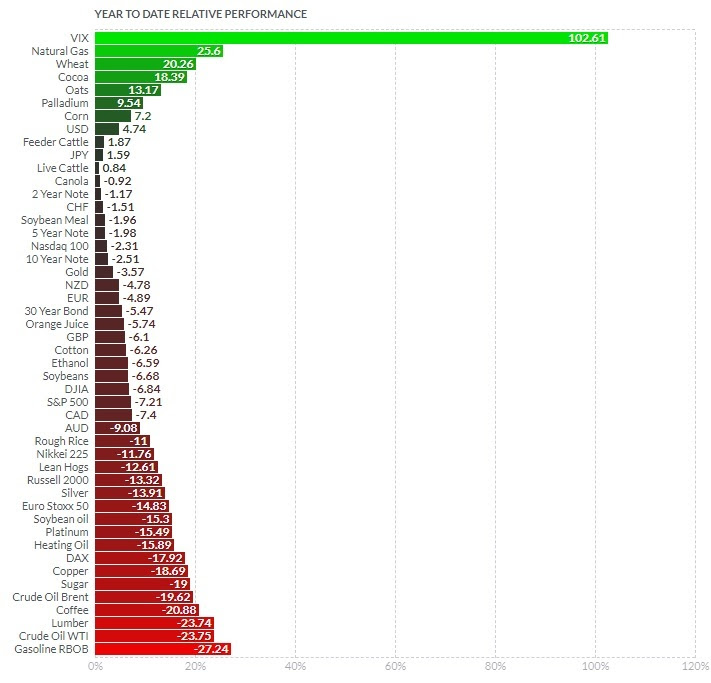

December 21, 5:00 pm EST As we head into the holidays and the end of the year, let’s take a look at the 2018 performance for the world’s biggest asset classes, currencies and commodities. |

|

|

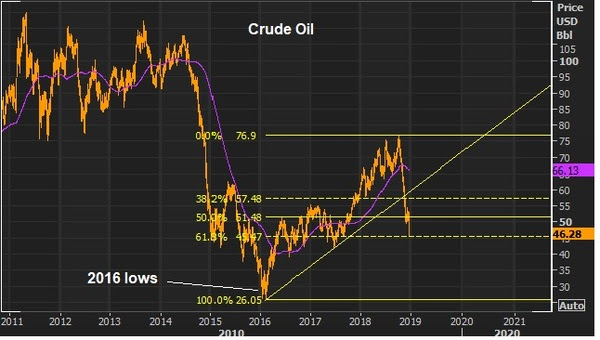

As you can see, there’s a lot of red. Global stocks are down. Bonds are down. Major commodities, down. Gold, down. Foreign currencies, down. Now, as we’ve discussed, major moves in markets are often triggered by a very specific catalyst, and then prices tend to drive sentiment change, and sentiment then tends to exacerbate the move in markets. There are always plenty of stories, at any given time, that can sound like rational explanations to fit to the price. In the case of the declines across asset classes this year, we’ve heard many viewpoints from very smart and accomplished investors over the past week, with concerns about the Fed, debt, deficits, slowdown, the end of an expansionary cycle, etc. With all of this said, often times the driver behind these moves in markets is specific capital flows (forced liquidations), not an economic narrative. With that, in rear view mirror, a lot of times (historically) all of the pontifications surrounding markets like these end up looking very silly. For example, let’s take a look at the run-up in oil prices back in 2007-08. Oil prices ran from $50 to almost $150 in about 18 months. Everyone was telling the world was running out of oil — “peak oil.” Did everyone get supply and demand so wrong that the market was adjust with a three-fold move that quickly? The reality: the price of oil was being driven by nefarious activities (manipulation). A major oil distributor was betting massively on lower oil prices and ran out of cash to meet margin requirements, as they were consequently squeezed (forced to liquidate) by predatorial traders that pushed the market higher. Among the predatorial traders, the largest oil trading company in the world, Vitol, was found to have been essentially controlling the oil futures market. When the CFTC (the regulators) finally came knocking to investigate, that was the top in oil prices. In the case of recent declines, the catalyst looks to be geopolitical (not economic), which then has given way to an erosion in sentiment (which can become self-fulfilling). The geopolitics: We’ve talked about the timeline of the top in stocks back in January, and how it aligns perfectly with the release of very wealthy Saudi royal family members and government officials, after being detained by the Crown Prince for three months on corruption charges. And then the decline from the top on October 3rd (both stocks and oil prices) aligns, to the hour, with the news that the Crown Prince would be implicated in the Khashoggi murder. These two events look like clear forced liquidations by the Saudis to retrieve assets invested in U.S. (and global) markets (assets that are vulnerable to asset seizures or sanctions). Beyond this selling, we also have a party that might have an interest in seeing the U.S. stock market lower: China. Trump has backed them into a corner with demands they can’t possibly fully agree to. If they did, their economy would suffer dramatically, and the ruling party would be highly exposed to an uprising. Could China be behind the persistence in the selling. Quite possibly. Bottom line: The lower stock market has put pressure on the Trump agenda, which makes it more likely that concessions will be made on China demands. My bet is that a deal on China would unleash a massive global financial market rally for 2019, and lead to a big upside surprise in global economic growth. Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

|

December 20, 5:00 pm EST

In recent days we’ve discussed the parallels between this year and 1994. In ’94 the Fed was hiking rates into a low inflation, recovering economy.

The Fed has done the same this year, methodically raising rates into a low inflation, recovering economy. And like in 1994, the persistent tightening of credit has sent signals that the Fed is threatening economic growth. Asset prices have swooned, and we have a world where cash is the best performing asset class (just as we experienced in 1994).

But remember, the Fed was forced to stop and reverse by early 1995. Stock prices exploded 36% higher that year.

With this in mind, over the past couple of weeks, several of the best investors in the world have publicly commented on the state of markets.

Among them, was billionaire Paul Tudor Jones. Jones is one of the great global macro traders of all-time. He’s known for calling the 1987 crash, where he returned over 125% (after fees). And he’s done close to 20% a year (again, after fees) spanning four decades.

Let’s take a look at what Jones said in an interview on December 10th …

He said the Fed has gone too far (tightened too aggressively). But he thinks the Fed is near the end of its tightening cycle.

With that, he expected to see more swings in stocks. He said he thinks we could be down 10% or up 10% from the levels of December 10th. But historically when the Fed ends a tightening cycle, after going too far, he says it has been a great time to be in the stock market.

The sentiment that the Fed has gone “too far” increased dramatically across the market this week — in the days up to yesterday’s Fed meeting. As such, because the Fed followed through with another hike yesterday, and telegraphed more next year, stocks continued to slide today. In fact, stocks have now/already declined 9.4% from the levels where Paul Tudor Jones made his comments about down 10%/up 10%. Again, he made those comments just 10 days ago.

With the above in mind, here’s what he said he would do if he saw itdown 10%: “I’m going to buy the hell out of ten percent lower, for sure. To me, that’s an absolute lay-up.”

|

|

December 14, 5:00 pm EST

We’ve talked about the struggling Chinese economy this week.

As I’ve said, much of the key economic data in China is running at or worse than 2009 levels (the depths of the global economic crisis).

And the data overnight confirmed the trajectory: lower.

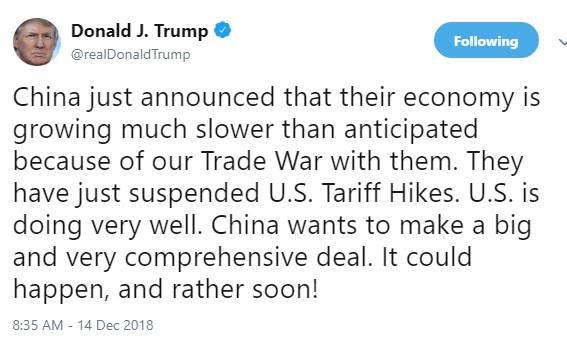

As we’ve discussed, this lack of bounce in the Chinese economy (relative to a U.S. economy that is growing at better than 3%) has everything to do with Trump squeezing China.

He acknowledged it today in a tweet ….

The question: Has China retaliated with more than just tit-for-tats on trade? Have they been the hammer on U.S. stocks? It’s one of the few, if not only, ways to squeeze Trump. As we discussed last week, when the futures markets re-opened (at 6pm) on the day of mourning for the former 41st President, there was a clear seller that came in, in a very illiquid period, with an obvious motive to whack the market. It worked. Stocks were down 2% in 2 minutes. The CME (Chicago Mercantile Exhange) had to halt trading in the S&P futures to avert a market crash at six o’clock at night.

Now, cleary stocks have a significant influence on confidence. You can see confidence wane, by the day, as stocks move lower. And, importantly, confidence fuels the decisions to spend, hire and invest. So stock market performance feeds the economy, just as the economy feeds stock market performance. The biggest threat to a fundamentally strong economy, is a persistently unstable stock market. In addition, sustaining 3% growth in the U.S. will be difficult if the rest of the world isn’t participating in prosperity.

With that in mind, in my December 1 note, I said “it may be time for Trump to get a deal done (with China) and solidify the economic momentum needed to get him to a second term, where he may then readdress the more difficult structural issues with China/U.S. relations.” That seems even more reasonable now.

We have two 12% declines in stocks this year. And you can see the fear beginning to set in. With that, the best investors in the world have made their careers by “being greedy when others are fearful” (Warren Buffett) or “buying when most people are selling and selling when most people are buying” (Howard Marks). There is clear value in stocks right now.

December 12, 5:00 pm EST

We talked about the China trade story yesterday.

In a nutshell, Trump has capitalized on an aligned Congress (in the first half of the mid-term) to stoke the U.S. economy. And that has strengthened the leadership position of the U.S. coming out of the decade long post-global economic crisis period.

With that, Trump has used the leverage of global economic leadership (in a vulnerable global economic period) to force change in China. And as we observed yesterday (in the charts of Chinese GDP, industrial production, domestic investment and retail sales), he’s getting movement because the Chinese economy was sputtering before the trade crackdown, and is now running out of gas. Much of the key economic data in China is running at or worse than 2009 levels (the depths of the global economic crisis). We get new data on industrial production, domestic investment and retails sales out of China tonight. This should provide more information on how the Chinese economy is being squeezed.

As for stocks, we have eleven trading days remaining for the year. The S&P 500 finishes today down about 1% for the year, and down 3.4% month-to-date. On the quarter, stocks are down 9% — the worst fourth quarter since 2008. If we look back at monthly returns, dating back to 1950, stocks have finished UP in December 75% of the time, for an average gain of 1.5%. Only two times have stocks has worse December performance over the near 70 year period (2002 and 1957).

And remember, as we discussed earlier this week, it’s not just stocks. It’s a zero (or near zero) return year for all major asset classes this year. Stocks, bonds, gold, real estate … nothing is working. The winner on the year has been cash.

|

December 11, 5:00 pm EST We’ve talked about the market volatility the past few days. Let’s take a look at a chart of the many swings in stocks for the year. |

|

|

|

|

You can see we’ve had seven significant declines this year. A clear observation in this chart is that the declines are fast. As they say, the market goes up on an escalator and down in an elevator. We’ve had a 12% decline over six days. A 5% decline in three days. A 9% decline in thirteen days. An 8% decline in six days (to open October). A 7.8% decline in eight days. A 6.8% decline in ten days. And, this recent, 8.2% decline in five days (assuming yesterday was the bottom). So, the seven declines of the year have averaged 8%, over a period of seven days. This argues that we probably have, indeed, seen the low on this recent sharp slide. And that leaves us, at today’s close, with a stock market trading at 15 times earnings — among the cheapest valuation we’ve seen only two times in the past 26 years. What stocks do you buy? Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment. |

December 10, 5:00 pm EST

On Friday we talked about the rise in market volatility, and what’s driving it.

It’s regime change. For the better part of a decade we had an economy driven by monetary stimulus (and loads of central bank intervention to absorb any potential shocks to markets). And since the election, we now have an economy driven by fiscal stimulus and structural reform.

But as I said Friday, with dramatic change, the pendulum can often swing a little too far in the opposite direction at first (from little-to-no volatility to a lot, in this case).

As it stands, stocks are now down about 1% on the year. In normal times you would see other alternative asset classes (to stocks) performing well. Bonds would be the obvious winner — but if you owned 10-year notes you would be down about 3% on the year (about flat after the yield). When stocks are down, and uncertainty is rising, gold tends to do well. Not this year. Gold is down 4.5% on the year. What about real estate. The Dow Jones Real Estate index is up, but small (+1.8%). Among the best investments of the year is cash. If you owned 1-month T-bills all year, you would be up close to 2%. I suspect this dynamic of little-to-no return asset class alternatives will change very soon.

December 7, 5:00 pm EST

Last year, the stock market broke a 21-year old record of the most consecutive days without a 3% intraday drawdown — some 240+ straight days.

We’ve now had a 3% intraday drawdown (open to low) three times since just early October.

So, what is responsible for the rise in volatility? Why such a contrast from last year?

It’s regime change. After nine years of zero interest rates and trillions of dollars of QE, the torch was passed this year. We entered the year with big tax cuts to implement.

This was the official transition from a monetary policy-driven economic recovery, to a fiscal stimulus-driven recovery. The Fed passed the economic stimulus torch to the White House.

Now, there was good reason that volatility remained subdued under the Fed’s emergency level zero-interest-rate policy. Why? The Fed told us, explicitly, that they (and other major global central banks) stood “ready to act” against any potential shocks that could disrupt the global economic recovery. That was an explicit promise to absorb risks so that investors (businesses, consumers, etc) would keep economic activity moving, by spending, hiring and investing.

The Fed (and other central banks, namely the ECB) had to be the backstop, so that people would pursue higher risk/return assets, in a world where risk-free assets yielded nothing. That was good enough to secure an economic recovery, but only at stall-speed levels of growth.

With that, as we entered the year, the U.S. economy was, for the first time in more than nine years, removing the central bank backstop (removing the life support for the economy). The gameplan: To replace low interest rates and QE with a $1.5 trillion fiscal stimulus package to catapult the economy out of the economic rut of 1% growth, and back toward sustainable 3% (trend) growth. And with that influence, the economy might have a chance to sustainably mend and breath on its own again.

So far we’ve gotten the growth (whether or not it’s sustainable has yet to be seen). But this regime change has also introduced uncertainty (and shock risks) back into the economy and markets. That resets the scale on volatility. And I think that adjustment has been underway.

With that said, the pendulum often swings a little too far in the opposite direction at first (from little-to-no volatility to a lot, in this case).

What stocks do you buy? Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.