|

|

|

|

February 28, 5:00 pm EST We end the month of February today, continuing the big recovery for stocks. After a decline of 10% in December. We were UP 9% in January and UP 3% in February. As we’ve discussed, the sentiment data is volatile and can take a hit when stocks fall, but it takes more sustained declines to damage the fundamental strength of the economy. Still, the media and Wall Street are good at exaggerating the downside. And with that, we’ve had expectations on economic data (as well as the earnings data) dialed down. That’s good, because it sets the table for positive surprises, and we had one this morning. The fourth quarter GDP number came in hotter, at 2.6%. The consensus view was for 2.3%. So here’s what full year 2018 looks like … Q1: 2.2% This gives us an average annualized growth of 3.1%. The average annualized growth coming out of the Great Recession (pre-Trumponomics) was just 2.2%. Below is what that growth has looked like against the long-term trend growth, dating back to 1947 (long-term trend growth = 3.2%).

|

|

|

So, we are finally approaching trend growth in 2018.

What were the experts thinking as we entered last year?

The Fed and Wall Street were looking for 2.5% growth. They undershot. For 2019, the Fed is looking for just 2.3% growth — that was adjusted down in their December projections as they were witnessing the sharp decline in stocks. A Wall Street Journal poll of economists back in December also showed a 2.3% growth forecast for 2019. Again, the bar has been set low. With that in mind, consider this: The next big pillar of Trumponomics is a trillion-dollar-plus infrastructure spend.

Just as expectations have been dialed down, this is where we could see a real economic boom kick in, especially if we get a deal on China (clearing that drag on sentiment).

We’re already well overdue for an economic boom period. Forperspective, let’s revisit this look at growth following the Great Depression and growth following the Great Recession …

|

|

|

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

|

|

|

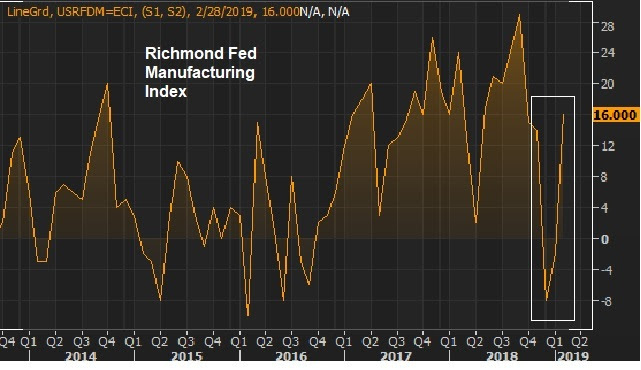

February 26, 5:00 pm EST Jay Powell (the Fed Chair) is on Capitol Hill this week, giving his semi-annual testimony to Congress. He reported today to the Senate Banking, Housing and Urban Affairs Committee. Tomorrow he will sit before the House Financial Services Committee. Remember, it was on January 4th that the Fed marched out Powell, Yellen, and Bernanke at an economic conference to reset the market expectations on monetary policy (moving from a four rate hike forecast for 2019 to a ‘wait and see’ approach). In response to the stock market drubbing of December, it was a clear message that the Fed is done raising rates. With that, there was nothing new today (nor should there be tomorrow, from Powell). The Fed will do whatever it takes to keep the economic recovery going. At the moment, that means promoting stable, low rates and a flexibility to do whatever is necessary. Remember, we’ve talked in recent weeks about some of the negative economic data hitting (from December), that reflects the souring of economic sentiment from the sharp December decline in stocks. But as I said, given the sharp V-shaped recovery in stocks we’ve seen since, we should “expect this data to bounce back just as sharply.” We’re getting a taste of it this morning. February manufacturing data from the Richmond Fed came in with a huge positive surprise. And the consumer confidence index followed a decline in January with a big upside surprise in February. We have a V in stocks. And you can see the V in the data … |

|

|

We’ll get the first look at fourth quarter GDP on Thursday (which will later be revised twice). The market has been looking for 2.5% which would give us better than 3% growth for the full year 2018. That’s “trend growth.” And for perspective, for those unable to block out the media and political noise, that’s nearly DOUBLE the average growth of the past ten years. Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment. |

|

|

February 21, 5:00 pm EST

We’re seeing some more December economic data that reflected the souring of economic sentiment from the sharp decline in stocks.

It started with retail sales last week. Stocks dipped immediately on the bad data, which proved to be a valuable buying opportunity. Today the bad number was December durable goods. These tend to be large investments that reflect optimism and these expenditures become the first to be delayed when that optimism wanes.

But less than two months later, and we have the v-shaped recovery in stocks. Expect this data to bounce back just as sharply.

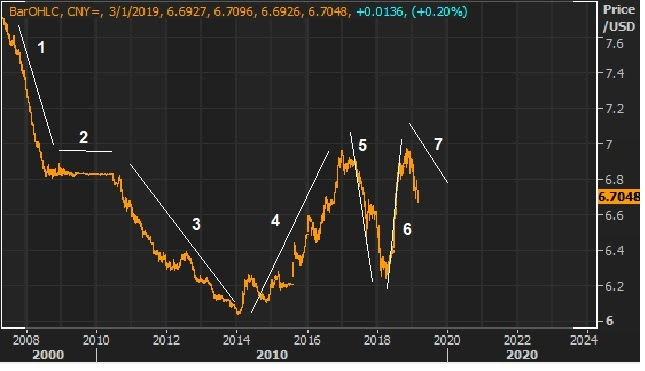

We continue to get signals that some form of agreement will come from the latest round of U.S./China talks. As we’ve discussed, some of the best signals are in the commodities markets.

Remember, to end last month, we talked about the setup for a big run in commodities this year. Crude oil was up 20% in January. It’s up another 5% already in February. Copper was up 6% in January. It’s up another 4% this month. And copper is the commodity known to be an early indicator of turning points in the economy.

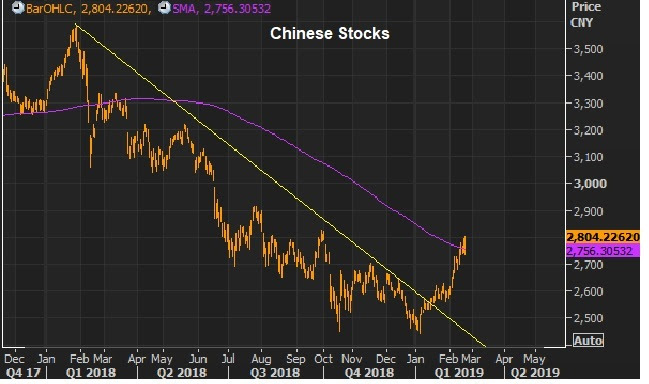

With this in mind, assuming we get resolution on China, and a continuation of trend growth in the U.S., we should expect this commodities rally to be in the early stages. And that should make emerging market stocks among the most attractive on the year. At the moment the MSCI emerging markets index is performing only in-line with the big developed stock markets.

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

|