For much of last summer, we talked about the building bull market in commodities.

The price of crude oil has nearly doubled since that time. But broader commodities have yet to take off.

Remember, we’ve looked at this chart of commodities versus stocks quite a bit.

You can see the clear divergence in these two key asset classes over the past five years.

As we’ve discussed, the only two times commodities have been this cheap relative to stocks were at the depths of the Great Depression in the early 30s and at the end of the Bretton Woods currency system in the early 70s.

And from deeply depressed valuations, commodities went on a tear, both times.

Now, since last summer, the trajectory of commodities has been up. But so have stocks. Still, this gap has narrowed a bit. Stocks are up 13% in the past year. The CRB index is up 17%.

The big difference between this year and last year, is the level on the 10-year yield. Last year this time, yields were 2.20%. Today, yields are closer to 3%. That’s because the economy is hotter, and inflation is finally reaching the Fed’s target of 2%.

What asset class should perform the best in a rising inflation environment? Commodities. As we’ve discussed in recent weeks, the data on the economy is lining up for some big positive surprises. That will be fuel for commodities prices.

If you are hunting for the right stocks to buy, in my Forbes Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers.

Watching the media and expert community digest the Fed decision is always interesting.

They are all programmed to home in on the worst-case scenario. It’s very similar to the way they parse politics.

In this case, the Fed projected an extra rate hike this year. They were projecting three hikes for 2018. Now they are projecting four hikes for the year (two of which are now in the rear-view mirror). Why an extra hike? Is it because they want to disrupt the recovery and undo all of their efforts of the past decade to manufacture that recovery? No. It’s because they think the economy is good! In fact, Powell (the Fed Chair) said “the main takeaway is that the economy is doing very well.”

And when asked about the impact of tax cuts, he said, we’ve yet to see the benefits. But, it should “provide significant support to demand over the next three years … encourage greater investment … and drive productivity.” This is exactly what we stepped through last week in my Pro Perspective notes (here). We laid out the components of GDP (consumption, investment, government spending and net exports) and we talked about the setup for positive surprises feeding into an economy that’s already running at near 3% growth — because pro-growth policies are just beginning to show up in the data!

With that, it should be no surprise that the Fed feels more comfortable telegraphing another hike, from what is still very low levels of interest rates.

Now, what is the negative scenario the pundits have been harping on? The yield curve. With the Fed gradually walking up short term rates (rates they set), the benchmark market interest rates (namely the 10-year government bond yield) has been soft. That creates yield curve flattening, which gets the bears excited that a yield curve inversion could be coming (a good historical predictor of recession).

Why is the 10 year yield soft? As we’ve discussed, the two major central banks that are still in the QE game have been anchoring longer term interest rates through their outright purchases of global government bonds (including lots of U.S. Treasuries, which keeps a cap on yields).

On that note, we have the ECB tomorrow. And the Bank of Japan will meet on monetary policy tomorrow night. The trajectory of global monetary policy is UP. And the more the Fed does, the more it forces that timeline elsewhere in the world to follow the Fed’s path on normalizing rates. The ECB will be following the Fed normalization path soon. And the Bank of Japan will be last. And when we get hints that it’s coming sooner rather than later, the yield curve will start steeping, and the bears will have a very hard time justifying their “sky is falling” view.

Last week we stepped through all of the components of economic output and talked about the setup for positive surprises. Keep in mind, the economy is running at near a 3% pace already. And if Trumponomics is just in the early stages of materializing in the data on consumption, investment, government spending and exports, then we may be in for a big growth number.

On Friday we talked about the exports (i.e. the trade) component. On that note, the media was stirring over the combative tone from G7 events over the weekend. What I heard was the potential for big movement (i.e. gains on U.S. exports, which will drive gains in GDP). Trump went in and proposed taking down all trade barriers. That’s negotiating from an extreme. And that typically brings about movement. Quickly, trade partners were discussing “reducing” barriers.

With hotter than expected growth coming, how will that effect Fed policy?

We will soon see. The Fed meets this week. They continue their path of normalizing rates. They’ve hiked once in 2015, once in 2016, three times in 2017 and once, thus far, this year. The market is nearly fully pricing in a second hike for the year on Wednesday. And expectations are for another hike in September. We’ll see this week if they’re adjusting uptheir growth forecasts.

As for the rate path: Remember, Powell is a Trump appointee, and from what we’ve heard from him thus far, he sounds like someone that’s not going to risk chipping away at the recovery by jumping ahead with overly aggressive rate hikes. Unlike the last regime, he will likely take a “whites of inflation’s eyes” approach.

We’ve talked about the set up for positive surprises in the data. We’ve looked at the first two components of GDP (consumption and investment) both of which are set up for positive surprises. Today let’s look at government spending.

It’s typical for debt to balloon in economic downturns. Not only did our debt/gdp ratio balloon in the U.S. but it ballooned everywhere. With that, as the global economy was being propped up by central banks, for the better part of the past decade, the politicians were reluctant to help on the fiscal side. Instead, they went the other way. They went the path of austerity. They focused on debt when the economy desperately needed growth.

Fiscal tightening in a widespread global recession is a recipe for tipping it all into depression. That required the central banks to do more, and more, and more to keep the economy from entering into a deflation spiral — fighting the drag of fiscal belt tightening. And it all began tipping over the edge in mid-2016.

But that changed with Trump election. Trumponomics has been all about restoring growth and breaking from the rut of economic stagnation. And a key pillar in that plan has been infrastructure and government spending.

On that note, he’s been pushing for a trillion dollar infracture spend over 10 years. And as we’ve discussed, while adding debt isn’t popular for the politicians to approve, natural disasters last year gave them an excuse to approve spending packages. Fast foward just six months and we’ve had more than $200 billion in aid approved from Congress. And now we’ve had an increase of $400 billion in government spending as part of the lastest government budget.

So the government spending piece has been in motion. And expect the rest of the world to follow. As we’ve discussed in recent weeks, we’ve seen the populist push back across the world, from Grexit, to Brexit, to the Trump vote, and now to the “Italy first” movement. The real fight in the “populist movement” is against economic stagnation. And much of that is due to mistakes on policy in response to the global economic crisis. And the core mistake has been austerity. Growthsolves a lot of problems.

What about the debt?

The media loves to talk about the $20 trillion dollar debt load, as if we are going to default and/or the rest of the world is going to dump our Treasuries and send interest rates skyrocketing and implode our economy.

Government debt and deficits are judged (by global trade partners, allies, global allocators of capital) on a relative basis – size relative to GDP. Again, our debt relative to GDP has ballooned since the global financial crisis. But it also has for everyone else in the world. That’s why people/countries are still plowing money into our Treasury market for virtually no return, because lending the U.S. money is still the safest place and way to preserve wealth.

The only alternative in this post global financial crisis environment is to focus on growth. Growth can solve a lot of problems, including the debt and deficit relative to GDP problems. As growth goes up, our debt relative to size of the economy goes down.

If we get the economy back on a sustainable growth path, then, in good times, we can work on the structural flaws that led us to the crisis. That’s the only option.

So, when we look at the components of GDP, the policy execution in Washington has been driving lift-off in all of the components. And yet the experts have still underetimated the potential for a growth boom. We’ve talked about the positive surprises that are coming down the pike in consumption, investment and govenment spending. Tomorrow, we’ll take a look at the trade piece.

We’ve talked the past couple of days about economic growth and the likelihood that we’re just beginning to see the positive surprises from Trumponomics materialize in the economic data.

Yesterday we talked about the consumption component of GDP. Today, we’ll take a look at investment.

Businesses invest when they’re confident about the outlook. And that was anything but the case for the decade following the global financial crisis.

Why? Because the politicians spent their time playing politics in Washington, instead of addressing an economy that was in desperate need of fiscal stimulus and structural change. Instead, they swung the regulatory pendulum too far in the opposite direction. And they played political football with debt and deficits, instead of acting to restore growth and stability. They stifled growth, just as the Fed was desperately throwing everything at the economy to keep it going. And it was all coming to a head by mid-2016 when global interest rates started turning negative.

But with the election came optimism. There was at least a chance of a return of good economic times (not just domestically but globally). We had a President with an aggressive economic stimulus plan, and a Congress in place to approve it. With that, small business optimism popped and has soared to record highs.

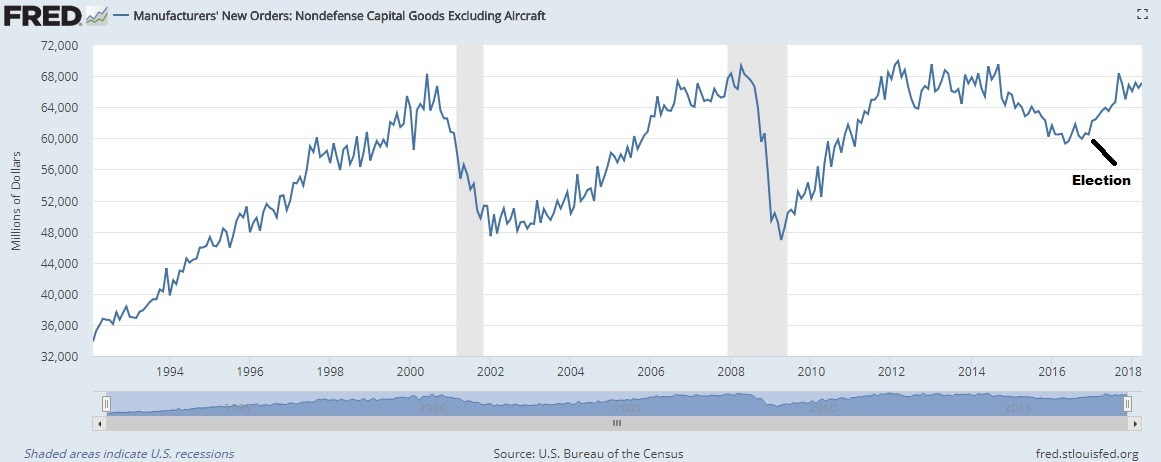

And companies are now investing again. Capital goods orders (the chart below) are nearing record highs again.

Get this: An ISM survey shows businesses were forecasting just 2.7% capital spending growth for 2018 when they were asked back in December. When they were asked again last month, they revised that number UP to 10.1% growth. A big positive surprise coming down the pike.

Again, as with the consumption picture we talked about yesterday, not only is the back drop solid, but we have stimulus that is still in the early stages of feeding through the economy, which is setting the table forpositive surprises in the economic data as we head toward the second half of the year.

And with that, we finally have the pieces in place for the aggressive bounce back in growth that is characteristic of post-recession recoveries. And that should continue to fuel stocks.

We’ve talked the past couple of days about economic growth and the likelihood that we’re just beginning to see the positive surprises from Trumponomics materialize in the economic data.

The formula for GDP is consumption + investment + government spending + net exports. So you can see in these components, the direct targeting of economic stimulus in the Trump economic plan to drive growth: tax cuts, deregulation, repatriation, infrastructure and trade negotiations.

Now, consumption makes up about two-thirds of GDP. Let’s look at consumption today, and we’ll step through the other contributors to GDP over the next few days.

First, what is the key long-term driver of economic growth over time? Credit creation. When credit is used to buy productive resources, wealth goes up. And when wealth goes up consumption tends to go up. With that in mind, in the chart below you can see the sharp recovery in consumer credit (in orange) since the depths of the economic crisis (this excludes mortgages). And you can see how closely GDP (the purple line, economic output) tracks creditgrowth.

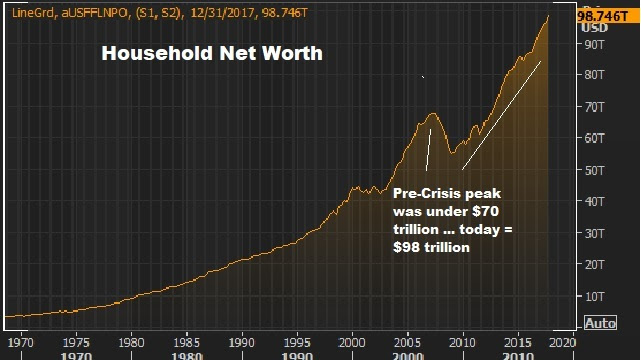

And we have well recovered and surpassed pre-crisis levels in householdnetworth — sitting at record highs now (up another $2 trillion since we last looked at it) …

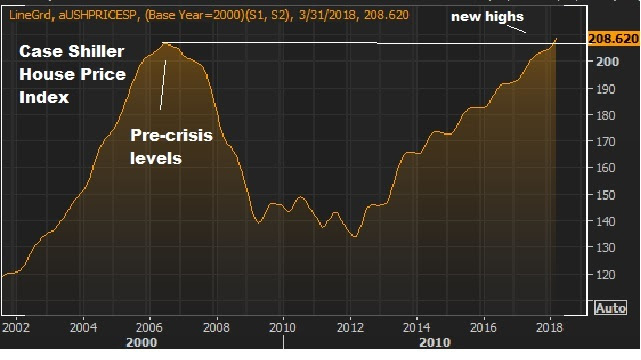

A large contributor to the state of consumption is the recovery and stability in housing. We are now back to new highs on the broad housing index …

When we consider this solid backdrop, remember, we’ve yet to have a return of ‘animal spirits’ — a level of trust and confidence in the economy that fuels more aggressive hiring, spending and investing.

And with that, as we discussed yesterday, while we are in the second longest post-War economic expansion, we’ve yet to have the aggressive bounce back in growth that is characteristic of post-recession recoveries.

But we now have the pieces in place to see the return of animal spirits and a big pop in economic growth. And that should continue to fuel for much higher stock prices. And there are stocks that will do multiples of what the broader stock market does.

On Friday, we talked about the building momentum in the economy. We’ve already had huge positive surprises in corporate earnings for the first quarter. And we’re probably just beginning to see the positive surprises on economic data roll in.

Remember, despite the execution success on Trumponomics over the past year (deregulation, repatriation, tax cuts and $400 billion in new government spending approved), the Fed is still expecting growth to come in well below trend (3%), at 2.7%. That’s just 20 basis points higher than they projected prior to the execution of massive tax cuts in late December.

The good news: Positive surprises are fuel for confidence and fuel for stocks.

Remember, we’ve yet to have a return of ‘animal spirits’–a level of trust and confidence in the economy that fuels more aggressive hiring, spending and investing. We should see this reflected in wage growth. Wage growth has been the missing piece of the economic recovery puzzle.

On that note, we’re now near the best wage growth in nine years, and that tax rate cut is still in the early stages of working through the economy.

Don’t underestimate the value of confidence in the outlook (and the return of “animal spirits”) to drive economic growth higher than the number crunchers in Washington can imagine. Remember, these are the same experts that couldn’t project the credit bubble, and didn’t project the sluggish ten years that have followed.

Remember, while we’re in the second longest post-War economic expansion, we’ve yet to have the aggressive bounceback in growth that is characteristic of post-recession recoveries. We now have the pieces in place to finally get it.

So, as we’ve discussed throughout the year, the backdrop continues to get better and better for stocks.

As we head into the long holiday weekend, let’s look at some key charts.

First, just a week ago, the U.S. interest rate market was spooking investors, as 10-year yields were hanging around 3.10%. The fear was, would 3% yields quickly turn into 4% yields, and hit economic activity.

As of today, we’re trading closer to 2.90% again, back below 3%.

But you can see, we run into this big trendline that represents this ascent in rates for 2018, which also reflects the outlook of a hotter economy, thanks to tax cuts (fiscal stimulus).

Bottom line here: The concern in interest rates is speed, not trajectory. The trajectory should continue to be UP, which is a signal that the economy is improving, and finally gaining the tracking to perform at trend, if not better than trend growth. The concern about ‘speed’ should be far less than it was a week ago.

Next, here’s a look at the S&P 500.

You can see in the chart above, we’ve broken the downtrend of this correction cycle. The longer-term trend is UP. And this bull trend started, not coincidentally, at the bottom of the oil price crash in 2016, when global central banks stepped in with measures to stem the slide in confidence.

So, we’ve had a healthy 12% correction in stocks, we’ve held the 200-day moving average, we’ve maintained the longer-term trend, and we’ve broken out of the downtrend of the correction. Small cap stocks have already returned to new record highs. And we have an economy on pace to grow at 3% this year or better, with corporate earnings expected to grow at 20% for the year. So, the second half of the year should be very good for stocks.

We have a lot of geopolitical noise surrounding markets.

Let’s step through them:

1) Yesterday, we discussed the Trump trade threats with China:

How is it playing out?

We have an economy that is leading the global economic recovery. China wants and needs to be part of it. Trump’s bark, with the credibility to bite, is creating movement. It’s creating compliance. That’s becoming a very positive catalyst for global economy and for geopolitical stability (the exact opposite of what the experts have predicted these tactics would produce).

2) We’ve talked about the shock-risk developing in Europe. A coalition government forming in Italy, with an “Italy first” approach to the social and economic agenda, has created some flight of Italian bond market capital toward safety. This has people skittish about another blowup threat of the euro zone.

How is it playing out?

The last time Italy was on default/blow up watch, the 10 year yields were 7% (unsustainable levels). At those levels, the ECB had to intervene.

This recent move in the Italian bond markets leaves yields at just 2.4% …

This looks like Grexit, Brexit and the Trump election. It creates leverage for the third largest economy in the European Union (excluding Britain). In this case, we may see it result in a loosening of fiscal constraints in the European Union – and an EU wide fiscal stimulus plan to follow the lead of the U.S.

3) The North Korean nuclear threat …

How is it playing out?

Eight months ago, North Korea launched a missile over Japan. Markets barely budged, and the world continued to turn. Now, we’ve quickly gone from an imminent threat to potential denuclearization. And now a meeting has been cancelled. With that, on the continuum of this relationship, I’d say it’s closer to its best point, rather than its worst.

Bottom line, these risks should do little to stop the momentum of the economy and the stock market.

There has been a lot of attention over the past couple of days on China and trade relations.

China has moved down tariffs on auto and auto parts imports. And a source today said the government has “encouraged” China’s largest oil refiner to buy more U.S. crude oil. Based on the reports, China is now taking about 8 times the daily volume of U.S. crude imports, compared to averages a few months ago.

These are concessions! This is a distinct power shift. Not long ago, the world was afraid to rattle the cage of China. They (global trading partners) tiptoed around touchy matters like Chinese currency manipulation prior to the global financial crisis a decade ago, and even more so after the crisis.

But now, you can see the leverage that has been created by Trump. This is exactly what we talked about the day after the election.

Here’s an excerpt from my November 9, 2016 ProPerspectives note, back when the experts were predicting Draconian outcomes for poking the China giant: “As we’ve seen with Grexit and Brexit, the votes came with dire warnings, but have resulted in creating leverage. Trump’s complaints about China are right. And a threat of slapping a tariff on Chinese goods creates leverage from which to negotiate.”

Now, we have an economy that is leading the global economic recovery. China wants and needs to be part of it. And we have a President that has a loud bark, and the credibility to bite. And that is creating movement. Let’s revisit, also from one of my 2016 notes, why this China negotiation is so important …

TUESDAY, SEPTEMBER 27, 2016

China’s biggest and most effective tool is and always has been its currency. China ascended to the second largest economy in the world over the past two decades by massively devaluing its currency, and then pegging it at ultra-cheap levels.

Take a look at this chart …

In this chart, the rising line represents a weaker Chinese yuan and a stronger U.S. dollar. You can see from the early 1980s to the mid-1990s, the value of the yuan declined dramatically, an 82% decline against the dollar. China trashed its currency for economic advantage—and it worked, big time. And it worked because the rest of the world stood by and let it happen.

For the next decade, the Chinese pegged its currency against the dollar at 8.29 yuan per dollar (a dollar buys 8.29 yuan).

With the massive devaluation of the 1980s into the early 1990s, and then the peg through 2005, the Chinese economy exploded in size. It enabled China to corner the world’s export market, and suck jobs and foreign currency out of the developed world. This is precisely what Donald Trumpis alluding to when he says ‘China is stealing from us.’

China’s economy went from $350 billion to $3.5 trillion through 2005, making it the third largest economy in the world.

This next chart is U.S. GDP during the same period. You can see the incredible ground gained by the Chinese on the U.S. through this period of mass currency manipulation.

And because they’ve undercut the world on price, they’ve become the world’s Wal-Mart (sellers to everyone) and have accumulated a mountain for foreign currency as a result. China is the holder of the largest foreign currency reserves in the world, at more than $3 trillion dollars (mostly U.S. dollars). What do they do with those dollars? They buy U.S. Treasurys, keeping rates low, so that U.S. consumers can borrow cheap and buy more of their goods—adding to their mountain of currency reserves, adding to their wealth and depleting the U.S. of wealth (and the cycle continues).

This is the recipe for big trade imbalances — lopsided economies too dependent upon either exports or imports. And it’s the recipe for more cycles of booms and busts … and with greater frequency.”

Again, China has to be dealt with. And we’re starting to see signs of progress on that front. Good news.