As we know, inflation has been soft. Yet the Fed has been moving on rates, assuming that they have room to move away from zero without counteracting the same data that is supposed to be driving their decision to increase rates.

Thus far, after four (quarter point) increases to the Fed funds rate, the moves haven’t resulted in a noticeable tightening of financial conditions. That’s mainly because the interest rate market that most key consumer rates are tied to have remained low. Because inflation has remained low.

A key contributor to low inflation has been low oil prices (though the Fed doesn’t like to admit it) and commodity prices in general that have yet to sustain a recovery from deeply depressed levels (see the chart below).

But that may be changing.

Commodities have been lagging the rest of the “reflation” trade after the value of the index was cut in half from the 2011 highs. Remember, we looked at this divergence between the stocks and commodities last month. Commodities are up 6% since.

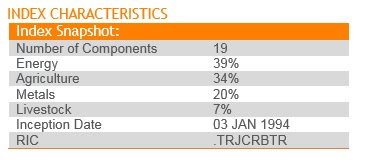

Things are picking up. Here’s the makeup of the broadly followed commodities index.

You can see, energy has a heavy weighting. And oil, with another strong day today, looks like a break out back to the $50 level is coming.With today’s inventory data, we’ve now had 12 out of the past 14 weeks that oil has been in a draw (drawing down on supply = bullish for prices). And with that backdrop, the CRB index, after being down as much as 13% this year, bottomed following the optimistic central bank commentary last month, and is looking like it may be in the early stages of a big catch-up trade. And higher oil (and commodity prices in general) will likely translate into higher inflation expectations.

Join our Billionaire’s Portfolio and get my most recent recommendation – a stock that can double on a resolution on healthcare. Click here to learn more.

Last week we talked about how a visit to Trump Tower was becoming a good predictor of a success for your stock.

Goldman continues to build representation in the Trump administration with the latest addition, Gary Cohn (current COO and President of Goldman Sachs) as the National Economic Council Director. And hedge funder Anthony Scaramucci, a Goldman Sachs alum and current member of the Trump transition team, is rumored to be in the running for a role in the administration. Goldman’s stock continues to rise, as the best performer in the Dow Jones Industrial average since Election Day (up 31%).

And remember, we talked about the visit last week of Masayoshi Son, the Japanese billionaire and majority stake holder in Sprint. Sprint is up 32% since election day.

So now we have the latest, and one of the most important cabinet appointments, Rex Tillerson, who will be Secretary of State. He’s the Chairman and CEO of Exxon Mobil, the biggest energy company in the country and one of the largest publicly traded companies. Exxon was up 2% today, and is up 9% since the election — better than the broader market, but not quite as good as the stocks of some other Trump Tower visitors.

This is a very interesting pick. Given that the President-elect has openly talked about using oil as an economic weapon (on Iraq… “we should have taken the oil”). We now have one of the world’s most respected experts in oil, and in negotiating around oil, charged with stabilizing the middle east and relations with Russia (to name a few). And given that the hot spot of global instability surrounds countries (or regimes) that are highly dependendent on oil revenue (funded by oil revenue), we have a guy that could credibly utilize leverage emerging U.S. supply, and global demand of the developed world, as a bargaining chip. His appointment/presence may also end up yielding a stable oil price environment going forward (tempering the manipulation of price extremes by OPEC).

Follow me and look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio is up more than 27% this year. You can join me here and get positioned for a big 2017.

Back in early June I talked about the building story for a breakout in natural gas prices.

Oil had doubled off of the bottom, but natural gas had lagged the move. This created really compelling opportunities for the natural gas stocks that had survived the downturn–and for those that had emerged from bankrupcy positioned to be debt-free cash machines in a higher price environment.

We looked at this chart as it was setup for a big trend break …

It was trading at $2.60 at the time and, as I said, “it looked like the bounce was just getting started” and “could be looking at the early stages of a big run in nat gas prices,” especially given that it was trailing the double that had already taken place in oil.

That break happened in October. And natural gas traded above $3.70 today. Four bucks is near the midpoint of the $6.50-$1.65 range of the past three years. And we’re getting close.

Remember, I said natural gas stocks are a leveraged play on natural gas prices. And back in June I noted the move in Consol Energy (CNX), which had already quadrupled since January. It sounds like you missed the boat? It’s nearly doubled since June!

We have 15% exposure to natural gas related companies in our Billionaire’s Portfolio. Follow me and look over my shoulder as I follow the world’s best investors into their best stocks – they tend to be in first, before stocks like Consol make their moves. Our portfolio is up more than 27% this year. You can join me here and get positioned for a big 2017.

As we headed into the holiday weekend, stocks were sitting near record highs, yields were hanging around near record lows, and oil had been sinking back toward the danger zone (which is sub $40).

In examining the relationship of those three markets, each has a way of influencing the outcome and direction of the others.

First, the negative scenarios: A continued slide in oil would soon sink stocks again, and send yields (the interest rate outlook) falling farther. Cheap oil, in this environment, has dire implications for the energy business, which has a cascading effect, starting with banks, which effects credit and the dominos fall from there.

What about stocks? When stocks are falling, in this environment, it’s self-reinforcing. Lower stocks, equals souring sentiment, equals lower stocks.

What about yields? As we’ve seen, lower yields are supposed to promote spending and borrowing. But, in this environment, it comes with trepidation. Lower yields, especially when much of the world’s government bond markets are in negative yield territory, is having a stifling effect on economic activity, as many see it as a signal of another recession coming, or worse.

Now, for the positive scenarios. Most likely, they all come with intervention. That shouldn’t be surprising.

We’ve already seen the kitchen sink thrown at the stock market. From a monetary policy standpoint, the persistent Fed jockeying through much of the past seven years has now been handed over to Japan and Europe. QE in Europe and Japan continues to promote stability, which incentivizes the flow of capital into stocks (the only liquid alternative for return in a zero and negative interest rate world).

And we’ve seen them influence oil prices as well, through easing, currency market intervention, and likely the covert buying of oil back in February/March of this year (through China, ETFs via the BOJ or an intermediary Japanese bank). Still, OPEC still swings the big ax in the oil market, and it’s been OPEC intervention that has rigged oil prices to cheap levels, and it looks increasingly likely that they will send oil prices higher through a policy move. The news that Russian and Saudi Arabian might coordinate to promote higher oil prices, sent crude 5% higher on Monday.

As for yields, this is where the Fed is having a tough time. They want yields to slowly climb, to slowly follow their policy guidance. But the world hasn’t been buying it. When they hiked for the first time in December, the U.S. 10 year yield went from 2.25%, to 2.30% (for a cup of coffee) and has since printed new record lows and continues to hang closer to those levels than not (at 1.53% today). Lower yields makes it even harder for them to hike because it’s in the face of weaker sentiment.

Last week, we looked at the U.S. 10 year yield. It was trading in this ever narrowing wedge, looking like a big break was coming, one way or the other, following the jobs report on Friday. It looks like we may have seen the break today (lower), following the week ISM data this morning.

What could swing it all in the positive direction? Fiscal intervention.

As we discussed on Friday, the G20 met over the weekend. With world government leaders all in the same room, we know the geopolitical tensions have been rising, relationships have been dividing, but first and foremost priority for everyone at the table, is the economy.

Even those opportunistically posturing for influence and power (i.e. Russia, China), without a stable and recovery global economy, the political and domestic economic outlook is bleak. So we thought heading into the G20 that we could get some broader calls for government spending stimulus was in order.

The G20 statement did indeed focus heavily on the economy. They said, “Our growth must be shored up by well-designed and coordinated policies. We are determined to use all policy tools – monetary, fiscal and structural – individually and collectively to achieve our goal of strong, sustainable, balanced and inclusive growth. Monetary policy will continue to support economic activity and ensure price stability, consistent with central banks’ mandates, but monetary policy alone cannot lead to balanced growth. Underscoring the essential role of structural reforms, we emphasize that our fiscal strategies are equally important to supporting our common growth objectives.”

Keep an ear open for some foreshadowing out of Europe to promote fiscal stimulus – the spot it’s most needed. That would be a huge catalyst for “risk assets” (i.e. commodities, stocks, foreign currencies) and would probably finally signal the top in the bond market.

After a fairly quiet August, we have a full docket of central meetings in the weeks ahead, starting this week. The European Central Bank meets on Thursday.

Join us here to get all of our in-depth analysis on the bigger picture, and our carefully curated stock portfolio of the best stocks that are owned and influenced by the world’s best investors.

This time last month, the famed oil trader—and oil bull—Andy Hall was dealing with a sub-$40 oil market again. And he was again explaining losses to investors in his multi-billion dollar hedge fund.

A guy that has made a career, and hundreds of millions of dollar in personal wealth, picking tops and bottoms in oil, had entered 2016 coming off his worst year ever. And 2016 started even worse.

I’ve talked about the oil price bust extensively, at the depths of the decline in January and February. While most were glorifying the benefits of a few extra bucks in the pockets of consumers from low gas prices, we walked through the ugly outcome of persistently low oil prices. It would be another global financial crisis, as failing energy companies and defaulting oil producing countries would crush banks, and the dominos would fall from there. Unfortunately, the central banks don’t have the ammunition to pull the world back from the edge of disaster for a second time.

With that, central banks stepped in with more easing in the face of the oil price threat, and oil bounced sharply.

Hall’s fund bounced sharply too, running up nearly 25% for the year, by the end of June. But he gave a lot of it back by the time July ended. And now, again, oil is closer to $40 than $50. Thanks to a report yesterday, that oil supplies were bigger than expected, the price of crude has fallen 10% since Friday of last week.

Hall was the CitigroupC +0.13% oil trader who made billions of dollars for the bank energy trading arm, Phibro, in the early-to mid-2000s. He was one of the first to load up on oil futures in 2002, when oil was sub-$30, on the thesis that a boom in demand was coming from China.

He reportedly made $800 million in profits for Citi in 2005 from his original bullish bet. He then made more than $1 billion in 2008 for the bank, as oil prices soared to $147 a barrel and then abruptly crashed. He profited handsomely from both sides, earning a payout from Citi of more than $100 million.

So he’s a guy that has been very right about turning points, and big trends. And he’s been pounding the table for much higher oil prices. He thinks oil prices are in for a “violent reversal” (higher). With an important OPEC meeting scheduled for later this month, Hall, in a past investor letter, reminded people how powerful an OPEC policy shift can be. In 1986, the mere hint of an OPEC policy move sent oil up 50% in just 24 hours.

In our Billionaire’s Portfolio, we’re positioned in deep value stocks that have the potential to do multiples of the broader market—all stocks that are owned and influenced by the world’s smartest and most powerful billionaire investors. Join us today and get yourself in line with our portfolio. You can join here.

When housing prices stalled in 2006 and then collapsed over the next three years, the subprime lending schemes quickly became exposed.

Mortgage defaults led to a banking crisis. Due to the highly interconnectedness of banks globally, the problems quickly spread to banks around the world. A banking crisis led to a global credit freeze. When people can’t access credit, that’s when it all hits the fan. Companies can’t meet payroll, don’t have the liquidity to make new orders. Jobs get cut. Companies go bust. Finally, the microscope on overindebtedness of consumers and corporates, turns to countries. Deficits leads to debt. Debt leads to downgrades. Downgrades leads to defaults.

For the most part, defaults were averted because central banks and governments stepped in, in a coordinated way, to backstop failing banks, failing companies and failing countries. From that point, continued central bank stimulus has 1) enabled banks to recapitalize, 2) foiled additional shock events, and 3) restored confidence to employers (to hire), to investors (to invest) and to consumers (to spend again).

As we’ve discussed in the past two weeks, persistently low oil prices represent a risk on par with the housing bust. And in recent days we’re seeing the signs of another global financial and economic crisis creeping uncomfortably closer to a “part two.”

As we’ve said, this time would be much worse because governments and central banks have exhausted the resources to bailout failing banks, companies and countries. But central banks, namely the Bank of Japan and/or the European Central Bank do have the opportunity to step-in here, become an outright buyer of commodities (particularly oil), as part of their QE programs, to avert disaster. But time is the oil industries worst enemy and therefore a big threat to the global economy. The longer policymakers drag their feet, the closer we get to the edge of global crisis — a crisis manufactured by OPEC’s price war.

Unfortunately, there are the building signs that the market is beginning to position for the worst outcome…

Key bank stocks in Europe are trading at levels lower than in the depths of both the global financial crisis (2009) and the European sovereign debt crisis (2012).

Source: Reuters, Billionaire’s Portfolio

The credit default swap market for key industries is sending up flares. This is where default insurance can be purchased against a company or country – and the place speculators bet on a company’s demise. Billionaire John Paulson famously made billions betting against the housing market via credit default swaps. Now the fastest deteriorating companies in Europe are banks. And the fastest deteriorating companies in North America are insurance companies (a sector that tends to have investments in high yield debt … in this case, exposure to the high yield debt of the oil and gas industry).

Source: Markit

The early signal for the 2007-2008 financial crisis was the bankruptcy of New Century Financial, the second largest subprime mortgage originator. Just a few months prior the company was valued at around $2 billion.

On an eerily similar note, a news report hit this morning that Chesapeake Energy, the second largest producer of natural gas and the 12th largest producer of oil and natural gas liquids in the U.S., had hired counsel to advise the company on restructuring its debt (i.e. bankruptcy). The company denied that they had any plans to pursue bankruptcy and said they continue to aggressively seek to maximize the value for all shareholders. However, the market is now pricing bankruptcy risk over the next five years at 50% (the CDS market).

Still, while the systemic threat looks similar, the environment is very different than it was in 2008. Central banks are already all-in. On the one hand, that’s a bad thing for the reasons explained above (i.e. limited ammunition). On the other hand, it’s a good thing. We know, and they know, where they stand (all-in and willing to do whatever it takes). With QE well underway in Japan and Europe, they have the tools in place to put a floor under oil prices.

In recent weeks, both the heads of the BOJ and the ECB have said, unprompted, that there is “no limit” to what they can buy as part of their asset purchase program. Let’s hope they find buying up dirt-cheap oil and commodities, to neutralize OPEC, an easier solution than trying to respond to a “part two” of the global financial crisis.

The legendary billionaire investor, Warren Buffett, lost 12.3% in 2015. That was his worst year since 2008.

Meanwhile, the average hedge fund lost 3%. The average mutual fund lost 2.7%. And stocks broadly finished the year down too (before dividends), for the first time since 2008. Even most of the biggest and best known professional investors had a bad 2015. Still, one of the lesser known, but one of the best in the world, defied the gravity of stocks and posted an 8.3% gain for the year.

It was billionaire Andreas Halvorsen. He runs Viking Global, the ninth largest hedge fund in the world at $31 billion in assets under management.

Halvorsen started his fund in 1999, after training under the legendary billionaire investor Julian Robertson. He’s a former Norwegian Navy Seal and a Stanford MBA.

Halvorsen extracted more than $2.5 billion from the markets in 2015, as a stock investor, in one of the more difficult stock picking environments in a long time. And last year was not an anomaly. Viking has one of the best track records of any hedge fund over the past 16 years. Since inception in 1999, the fund has returned 23% annualized (before fees) vs. a 4% annualized return for the S&P 500.

Halvorsen’s stock picking abilities have produced returns at a factor of 3.5 times better than Buffett’s since he’s been at the helm of Viking. And he’s done it with much smaller drawdowns. In fact, Viking has only had two losing years since 1999. The fund lost 0.9% in 2003 and lost just 0.9% in 2008, a year when almost all stock investors were crushed. Buffett lost 31.5% that year.

The following are Viking’s top positions: Allergan (AGN), Walgreen’s (WBA), Google/Alphabet (GOOGL), Amazon (AMZN) and Broadcom (BRCM).

In addition, in Halvorsen’s most recent investor letter, he said his fund had doubled down (added more) on a very controversial stock in their portfolio. At Billionaire’s Portfolio we curate a portfolio of the best stock picks of the world’s best billionaire investors – our subscribers follow along. To find out what stock Viking Global is adding to after a big decline, subscribe today.

Stocks, Markets, Stock Market, Investing, Billionaires, News, Finance, Financial, Apple News, Economy, Oil, Interest Rates, Politics, Trading, ETFs, Business, International, Forex, business, Fed, European Central Bank, Bank of Japan

At Billionaire’s Portfolio we study the buying patterns of the world’s greatest billionaire investors and hedge funds. So when two of greatest billionaire investors in the world, Carl Icahn and Warren Buffett, are adding more to their large, beaten down stakes in energy companies, we pay close attention.

We know two things about Buffett and Icahn: 1) they have made billions throughout their careers buying when everyone else is selling, and 2) they have a knack for picking the winners, the stocks and sectors, and marking the bottom when they enter.

Their respective records are especially remarkable in times when widespread fear and doubt is in the air. For example, Icahn marked the bottom in technology stocks in the fall of 2012 with his 10% position in Netflix. He made $2 billion in profits on the trade, a nearly 1,000% return. Buffett marked the bottom in bank stocks in the fall of 2011 when he initiated a $5 billion position in Bank of America. That investment has almost tripled in price since, producing nearly $10 billion in open profits for Buffett.

Now, it’s typical in market environments like this to hear from experts that warn against picking tops and bottoms. But contrary to the Wall Street adages against market timing, the two best investors of all-time have amassed two of the largest personal fortunes in the world by (as Buffett says) “being greedy while others are fearful.” And they are using the new lows in oil and energy markets to add more to their stakes. Historically, that tends to be a profitable signal. There is a Harvard study that shows when hedge funds “double down” on losing positions, on average those tend to be their biggest winners.

Let’s look at the investments from this billionaire duo where they have been adding to their losers:

1) Phillips 66 (PSX) – Buffett revealed last September he had taken a $4.5 billon position in the energy stock Phillips 66. This is a typical Buffett stock. It sells for just 9 times earnings, a huge discount to the S&P 500’s P/E of 21, and the stock pays nearly 3% in a dividend. Furthermore, the company has a pristine balance sheet, with very little debt – a classic Buffett stock, cheap and safe. Buffett has added another $700 million to this stock just in the past two weeks. He’s the largest shareholder.

2) Chesapeake Energy (CHK) – Carl Icahn owns doubled his stake last spring when he bought 6.6 million shares of CHK for about $14. Icahn now owns 11% of Chesapeake. If the stock returns to the price where Icahn doubled down it would represent an almost 300% return for today’s levels. With the sharp fall in the stock price this past week, I wouldn’t be surprised if we find in the coming days that Icahn added more into the recent slide.

3) Cheniere Energy (LNG) – Carl Icahn also initiated a $1.3 billion position in energy stock LNG in August of last year, taking an 8% ownership in the company. Cheniere is on track to become the first U.S. company able to export liquefied natural gas. This makes LNG a classic “wide moat” (no competition) stock. Icahn has already secured two board seats on Cheniere’s board. Icahn’s “board seat effect” has proven to be a huge predictor of success for the legendary activist. According to an essay Icahn penned last year, when he gets a board seat in a company, his stock returns averages 27.5%. Since his initial stake in August, Icahn has added to his stake several times into the end of the year. He now owns 13.8% of LNG — the largest shareholder.

This morning, the European Central Bank primed global stocks by telegraphing more action (more stimulus) to respond to the recent shake up in global economic activity and sentiment.

It had to happen. In the grand scheme of things, the ECB’s sentiment manipulation this morning was the bare minimum of what had to be done.

The global central banks (led by the Fed) have spent, committed and promised trillions of dollars to manufacture the tepid recovery that’s underway, in hopes that they can bridge their way to the point where economies begin to organically grow again. That bridge has not yet reached the point of organic growth. And it’s not even that close. With that said, the recent collapse in oil prices, and the threat to an implosion of the energy sector was getting narrowly close to undoing what the central banks have done to this point. And, not only is another downturn unpalatable, but it’s apocalyptic. The bullets have all been fired. Fiscal and monetary policy would have no shot to ward off another global destabilization.

The plan for the continuation of the global central bank-led (and manufactured) economic recovery has been clear. And the evolution, where the U.S. economy began leading global growth, while Europe and Japan were just embarking on big and bold stimulus is likely the reason Bernanke felt comfortable enough to exit. Think about it, the Fed hands off of the QE baton to the ECB (Europe) and the BOJ (Japan). Meanwhile, the Fed can make the first step in moving away from emergency policies. Europe and Japan have all of the ingredients to execute on their big QE promises to continue providing fuel for global growth and stability (they need a weaker currency).

The Fed’s exit from emergency policies shows their confidence in the economic recovery. And the ECB and BOJ can “print away”, suppressing global market interest rates (which helps the Fed), fueling higher global stock prices (which helps everyone), and fueling capital flows into the U.S. to further bolster U.S. recovery.

The question is often asked, when referring to QE, “what is the transmission mechanism?”

Here’s the answer: 1) Stability – QE assures people that the central bank(s) are there, acting, and ready to do more, if needed, to defend against any further shocks to the global economy and financial system. That creates stability. And with that stability backdrop, major central banks promote incentives for people to borrow again, to spend again, to hire again. 2) Risk-Taking – Ultra-low interest rates and a stable environment promotes the rebirth of housing activity, and encourages investors to reach further out on the risk curve for more return. That means more demand for stocks, and higher stock prices. Higher stocks and higher housing prices create paper wealth. Paper wealth gives people comfort to borrow again, to spend again and to hire again.

That has been the recipe. And it has worked! The key ingredients continue to be higher stocks and higher housing prices (even if at a modest growth rate).

Central Banks Need You To Buy Stocks

With the ECB doubling down on their commitment to do “whatever it takes” and with the architect of the massive

QE program in Japan, Prime Minister Abe, uttering those same words in the past month, the pressure valve on the Fed has been released and should clear the path for the Fed to make its first move on interest rates in nine years this coming December.

When we consider where we’ve been (fighting back from what was potentially the Great Apocalypse of economic crises), and how the economy is performing now, the fact that the Fed thinks the economy is robust enough to remove emergency policies is, indeed, a time for celebration.

And with that, there are plenty of reasons to buy stocks, not just because central banks need you to. But frankly, most people don’t seem to understand this central bank dynamic anyway. And that’s precisely why sentiment has been gloomy on stocks for the entire recovery, dating back to the 2009 bottom.

Given this negative sentiment, with respect to the economic outlook and the outlook for stocks, it’s not surprising that the declines in stocks along the way have been sharper and more slippery because of this pervasive fear in the investment community. Along the way that has created great buying opportunities. This recent decline is no different. Often market sentiment tends to over emphasize events. And it tends to be wrong (contrarian). Nonetheless, when events pass, as we’ve seen along the way, regardless of the outcome, the fog lifts, and the underlying fundamentals return to dictate performance.

From a valuation standpoint, when rates are “low,” historically, the P/E ratio of the stock market tends to run north of 20. And, of course, we are not just in a low interest rate environment; we are in the mother of all low interest rate environments, even with the Fed ready to begin moving. North of 20 is precisely where the valuation on stocks has gone in the past year. Now, based on next year’s earnings estimate, the market is valued at just 15x. A move to 20x earnings would mean an S&P 500 around 2,600 by next year. That’s 30% higher than current levels.

Why would a low rate environment tend to mean higher valuations for stocks?

Economics are about incentives, and when rates are ultra-low, people are incentivized to switch out of bonds and into stocks, to seek higher yield/higher returns. When we think about the direct implications of this incentive dynamic, we look no further than the amount of cash that big funds are holding, and where that might find a home.

Historically, one of the most predictive indicators of stock market bottoms is how much cash fund managers are holding. Right now, cash is at levels only seen during the 2008-2009 Great Recession period. Fund managers are holding 5.5% of their portfolio in cash and their allocation to stocks are at the lowest levels since 2012. Furthermore, 35% of all funds are now overweight cash.

When you see fund managers so pessimistic on stocks, while holding so much cash, it has historically been a signal for a huge move in stocks. These managers are paid to invest, and cash has always been the dry powder that’s fueled every rally in stocks throughout history. When fund managers are not holding cash and are fully invested, they have no powder left to buy stocks. The only way they can buy a stock is to sell another stock, which usually occurs at market tops.

The last two times fund managers held this much cash while being so underweight stocks was 2009 and 2012.

What happened? A huge rally! Between 2009 and 2011, the S&P rose 41%. Between 2012 and 2014, the S&P 500 rose 46%.

Sign up for our Free ebook, The Little Black Book of Billionaire Secrets, and learn how to follow the “best ideas” of the world’s top billionaire investors. You don’t have to be rich to take part. You don’t have to pay the hefty 2% management fee and 20% profit share to a hedge fund. You can follow the lead of powerful billionaire investors by simply buying the same stocks they do, in your own brokerage account.

Most energy stocks are trading at historical lows, and many have been priced like stocks in the pipeline for bankruptcy. Even valuations on the major oil companies are trading at a 35-year low relative to the broader market. And it all has to do with the weakness in the price of oil.

But that may be changing, and very soon.

The self-made billionaire energy trader, Boone Pickens, has recently called for $70 by year-end. If he misses, he says it will be because oil is “over $70, not under $70.” He’s not the only oil bull. Another famous and very wealthy energy trader has called a bottom in oil too, and is looking for much higher prices. His name is Andy Hall.

Hall was a Citigroup oil trader who made billions of dollars for the bank energy trading arm, Phibro, in the early-to-mid-2000’s. He was one of the first energy traders to load up on oil futures in 2002, when oil was sub-$30, on the thesis that a boom in demand was coming from China.

Hall reportedly made $800 million in profits for Citigroup in 2005 from his original bullish energy bet. He then made over $1 billion in 2008 for the bank, as oil prices soared to $147 a barrel and then abruptly crashed. Hall profited handsomely from both sides of the trade and earned over $100 million for himself that year.

Hall now runs a $3 billion energy hedge fund, Astenbeck Capital Management. He’s made fortunes pegging bottoms in tops in oil over the past 15 years, and he’s expecting a big bounce back in oil. In a recent letter to investors, he laid out an extensive fundamental case for higher oil prices and suggested a cut from OPEC could be coming as well. On that front, he noted that merely a hint of an OPEC policy change in August of 1986 spiked oil prices by 50% in just 24-hours.

So we have two of the greatest and wealthiest oil traders in the world that are long oil and have called for a return to much higher prices sooner rather than later.

If they are right about the future direction of oil, there will be a lot of money to be made in energy stocks on this bounce. Warren Buffett has famously said a simple rule dictates his buying: “Be fearful when others are greedy, and be greedy when others are fearful.”

This statement shows the mindset of great investors and how they react when markets fall. Instead of running in fear, great investors welcome market corrections as opportunities to buy on the cheap. You don’t get rich buying into a high market or selling into a falling market. You can get rich though, buying into market corrections and beaten-down markets.

At Billionairesportfolio.com we love opportunities like those presented in the energy sector right now. But, we like to have the added protection of investing alongside a billionaire investor that has a lot of money at stake, and the power to influence change.

In this case, not only does billionaire oil magnate Boone Pickens have his money where his mouth is on his oil call, but each of the five energy stocks below are owned by at least one of the world’s great billionaire investors, and each has the potential to double (or more) if Pickens is right about oil at $70 by year-end:

1) SandRidge Energy (SD) – Billionaire investor Prem Watsa owns almost 11% of SandRidge. This stock traded above $4 last November, when oil was $70. That’s 788% higher than its current share price today.

2) Oasis Petroleum (OAS) – Billionaire hedge fund manager John Paulson owns nearly 7% of this stock. Additionally, SPO Advisory, a $7 billion activist hedge fund, owns almost 15% and has been buying the stock on almost every dip. When oil was last $70, OAS was trading $25, or 150 % higher than current levels.

3) Whiting Petroleum (WLL) – Billionaires John Paulson and Andreas Halvorsen, of the hedge fund Viking Global, own a combined 10% of WLL. And the company has officially put itself up for sale! This stock traded at $52 when oil was last at $70. That would be a 205% return from its share price today.

4) Chesapeake Energy (CHK) – Billionaire investor Carl Icahn owns 11% of CHK and recently added to his position around $13. Chesapeake has halted their dividend and said they are looking at selling assets, all of which is bullish for the stock. The last time oil was $70, Chesapeake was $25. That would be a 203% return from its price today.

5) Transocean Energy (RIG) – Billionaire Carl Icahn also owns almost 6% of Transocean. RIG recently reported better than expected earnings this month. The last time oil was $70 Transocean was $24 or almost a 50% return from its share price today.

At Billionairesportfolio.com, we follow the “best ideas” of the world’s top billionaire investors. You don’t have to be rich to take part. You don’t have to pay the hefty 2% management fee and 20% profit share to a hedge fund. You can follow the lead of powerful billionaire investors by simply buying the same stocks they do, in your own brokerage account.