Stocks continue to recover from the wreckage of December. From December 3rd to December 26th, the S&P 500 collapsed 16%. That was over just 15 trading days.

We’ve since had a 12% bounce over 15 days. But we need another 7% to recoup the losses from December 3.The good news: The catalysts for a big recovery are in place — not only to recover the December 3rd levels, but to print new all time highs in the stock market.

Remember, major turning points in markets are often driven by some form of intervention. In this case, we’ve had it. We had intervention from the U.S. Treasury on December 23/24, 1) calling out to the six largest U.S. banks, and then 2) calling a meeting with the President’s Working Group (which includes the Fed).

Just days later, the Fed sent a clear message to markets that they were there to promote market stability (that means higher stock prices).

Add to this, we’ve entered Q4 earnings season, and we’re getting plenty of positive surprises already, on expectations that were already dialed down substantially in the wake of the stock market decline of the fourth quarter. As of last Friday, 90% of the companies that had reported beat Wall Street’s expectations.

So, where can stocks go from here?

Even with the sharp recovery over the past several weeks, the P/E on this year’s earnings estimate is just 15. That’s cheap relative to history. It’s very cheap relative to historical low interest rate environments.

If we apply Wall Street’s estimate on earnings for the S&P 500 (which is $172), to a P/E of 18 we get 3,096 on the S&P by the end of the year. If we apply a 20 P/E, we get 3,440. That’s argues for anywhere from 18% to 31% higher for 2019.

Keep in mind, that’s if Wall Street hasn’t undershot on its estimate. But they tend to undershoot often (to the tune of about 70% of the time).

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

We now have Q4 earnings in from three of the country’s four largest banks. Yesterday it was Citi. Better earnings were driven by cost cuts not growth. Still, the stock is up 8% in two days.

Today it was Wells Fargo and JP Morgan. Wells, too, had soft revenues but beat on earnings driven by cost cuts. JP Morgan missed on earnings and revenues.

Now, Jamie Dimon runs JP Morgan — the largest U.S. based global money center bank. And he has been publicly positive on the economy and the market outlook, in the face of a lot of broad negativity and fear late last year.

Let’s take a look at what he had to say about JP Morgan’s earnings and the operating environment…

JP Morgan generated record earnings and record revenues for full year 2018. And Dimon says they would have done it even without the tax cuts. He says his business shows the U.S. consumer to be healthy and engaged. Consumers are spending, saving and investing. And Dimon said they opened Chase branches in new states for the first time in nearly a decade.

This all in a year where the chatter about an impending recession grew by the month, for no other reason than the economic expansion has been running long.

According to the biggest bank in the country, things sound pretty good.

Importantly, last year, the blowout earnings were often met with selling in the broad stock market. It’s looking like that dynamic is changing. Stocks are rising, even on less than impressive numbers (thus far). That a good sign for the sustainability of the rebound.

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

And it was driven by: 1) the central bank in China stepping in with an injection of over $100 billion in liquidity into the economy through a cut to the bank reserve requirement ration, and 2) the three most powerful central bankers in the world (over the past 10 years) sitting on stage together and massaging market sentiment on the path of interest rates.

We entered the year with the idea that the Fed would need to walk back on its rate hiking path this year (possibly even cutting, if the stock market environment persisted). And today, just days into the new year, we get the Fed Chair Powell, former Fed Chairs Yellen and Bernanke telling us that the Fed is essentially done of the year, unless things improve.

Remember, last year was the first since 1994 that cash was the best producing major asset class (among stocks, real estate, bonds, gold). The culprit for such an anomaly: An overly aggressive Fed tightening cycle in a low inflation recovering economy. The Fed ended up cutting rates in 1995 and spurring a huge run up in stocks (up 36%). Now, we’re getting the Fed standing down, and committing to “responsiveness to the data and markets.”

Yellen voluntarily drew the comparison to today to early 2016 – where the Fed had to respond to sour markets that were beginning to feed into the economy.

In 2016, the oil price crash prompted a coordinated response by global central banks to avert another financial crisis. For the Fed’s part, they took two of the four projected rate hikes they had guided for 2016 off of the table (effectively easing). This coordinated easing from global policymakers put a bottom in stocks and oil in early 2016. Oil doubled by the end of the year. Stocks finished 2016 up 25% from the oil-price crash induced lows.

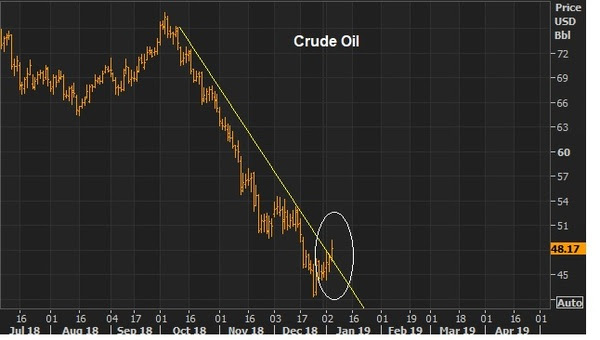

Here’s a look at the chart on oil today…

You can see this big trendline that represents the plunge from $76 has broken today.

And here’s a look at stocks …

We broke a big level today on the way up in the S&P 500 (2520) and it looks like a V-shaped recovery is underway, to take us back to where stocks broke down on December 3rd. That would be 12% from current levels.

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

One of the spots weighing on the market has been the Fed’s persistent increase in interest rates. With that, and with some soft spots showing in the global economy and a more challenging policymaking environment ahead in Washington, we were watching Fed Chair Powell’s remarks very closely late yesterday (after the market close) for some signalling that a pause on rate hikes might be coming.

Unlike past Fed heads, Powell is a plain spoken guy. And he tends to be very clear in his messaging. With that, he didn’t seem to have an agenda for sending a clear signal to markets yesterday. But he did have some dovish takeaways. He said they are at the point where they have to take seriously the risk of moving too far and stifling the recovery and not moving far enough to manage inflation. On that note, he acknowledged that the level of interest rates are weighing on the house market. And he said signs of a global slowdown are concerning. So, he tells us they’re watching the data closely for next moves, and then he tells us some data is suggesting slowing.

Now, it’s common for other Fed governors to be out talking, between meetings, in an effort to set market expectations. With that said, the bigger signalling came today. The Atlanta Fed President and a voting Fed governor on monetary policy (Bostic), had a prepared speech in Madrid today. He said the Fed is in the final steps of getting to the neutral rate (which means neither accommodative nor restrictive). He said that’s where they “want to be” and then said he thinks the neutral rate is between 2.5% and 3.5%. Rates are currently 2%-2.25% (almost the low end of his neutral range). And he said they should proceed cautiously with rate increases. Bottom line: These statements suggest the Fed could be done with the ‘normalization’ process of rates after one or two more hikes.

So, we were looking for the Fed to use the weakening global growth data this week (from Japan and Europe), some softer global inflation data, and the changes in Congress, as an excuse to dial down the market’s expectations for the path of rates. It was subtle, but I think we’ve seen it.

Indeed, stocks ripped higher on Bostic’s comments this afternoon. The Dow jumped about 1.5% today as the comments hit the news wires.

Moreover, we’ve had some more uncertainty removed from marketsin the past 24-hours. We now have trade discussions re-opened between China and the U.S. And today, the U.S. Treasury has named the individuals that will be sanctioned in Saudi Arabia, regarding the murder of Khashoggi. To this point, the Saudi Crown Price isn’t one of them, which means the Saudi government is not being sanctioned.

It’s been a violent six weeks for stocks, but the lows from late October remain well intact. And we may now be clear for another recovery leg of this recent broad market correction.

Join me here to get all of my in-depth analysis on the big picture, and to get access to my carefully curated list of “stocks to buy” now.

In my note yesterday, we talked about the probable outcomes for the elections.

Whether we see the Republican’s retain control of the house, or lose it, both scenarios should be a greenlight for stocks.

Why? Because the cloud of uncertainty will be lifted. Even if we were to have gridlock in Washington, from here forward, the economy has strong momentum already, and the benefits of fiscal stimulus and deregulation are still working through the system.

Now, given today’s midterm elections are feeling a bit like the Presidential election of 2016 (as a referendum on Trump, this time), I want to revisit my note from election day on November 8, 2016.

As I said at that time, central banks had been responsible for the global economic recovery of the prior nine years, and for creating and maintaining relative economic stability. And creating the incentives to push money into the stock market (i.e. push stocks higher) played a big role in the coordinated strategies of the world’s biggest central banks. With that, I said “neither the economic recovery, nor the stock market recovery can be credited much to politicians. In this environment, in the long run, the value of the new President for stocks will prove out only if there’s structural change. And structural change can only come when the economy is strong enough to withstand the pain. And getting the economy to that point will likely only come from some big and successfully executed fiscal stimulus.”

It turns out, Trump has indeed executed on fiscal stimulus. And he’s gone aggressively after structural change too (perhaps too early, and with some success, but at a price he may pay for politically). Still, he’s been able to execute ONLY because he’s had an aligned Congress.

Importantly, the economic policies out of Washington have allowed the Fed to bow-out of the game of providing life support to an economy that was nearly killed by the financial crisis. That’s good!

We talked about the potential bottom in stocks on Monday, based on this big trendline we had been watching. That, of course, also coincided with a similar line in the Dow, which represented a 10% correction on the nose.

That indeed does look like the bottom.

You can see in the chart of the S&P 500 above, this big line dating back to the oil price crash lows of 2016 held beautifully, and we are now up more than 5% from just Monday of this week.

And today we have this …

We’re getting a break of this sharp downtrend of the past month (circled).

And we have a very similar pattern in Japanese stocks (the Nikkei).

Most importantly, the biggest mover of the day in global stock indices (and nearly all markets) was emerging market stocks. The MSCI Emerging Markets Index was up 3.3% today. And the strength in emerging markets was well underway before the news today that the U.S. (Trump) and China (Xi) has some constructive talks on trade.

What gets hit first and hardest when global risk elevates? Emerging markets. EM was down 21% on the year earlier this week. But this is also where the biggest gains can come as the dust settles, and people realize that a hotter U.S. economy, will translate into hotter growth in emerging markets. As I’ve said, this market decline has been a gift to get involved.

As we discussed yesterday, it’s very dangerous to let political views influence your perspective on markets and investing.

And I suspect we are seeing plenty of people make that mistake.

That means many will be left behind on a stock market recovery, again. That probably means the bull market for stocks still has a ways to run. John Templeton, know to be one of the great value and contrarian investors of all time, said “bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.”

Incredibly, after a more than four-fold run from the financial crisis bottom, the stock market continues to have a LOT of skepticism. Does this mean we are only half way through this cycle? Maybe.

The arguments for the stock market bears and pessimists on the economy have many holes, but the biggest is the lack of context. That context: the global economic crisis, and the aftermath (up to present day).

You can’t evaluate anything about this economy without taking into account where we’ve been over the past decade, the role central banks have played throughout, the coordinated intervention that has taken place globally (along the way) to avoid a global depression, and the interconnectedness of global economies that continues.

Without this context, the skeptics like to call it “late in the cycle” for an economy that (on paper) is in the second-longest expansion in U.S. history. With context, we’re probably closer to “early cycle,” given that the decade of ultra-slow growth was manufactured by central banks.

This violent repricing of the tech giants came with clear warnings (i.e. the tightening of regulatory screws).

Now that we have it. And it is very healthy, and needed.

As we discussed yesterday, I would argue we are seeing regulation priced-in on the tech giants, which can create a more level playing field for businesses, more broad-based economic activity, and a more broad-based bull market for stocks. This is a theme we’ve been discussing in my daily note here for quite sometime.

And I suspect now, we can see the areas of the stock market that have been beaten down, from the loss of market share to the tech giants, make aggressive comebacks.

On that note, here’s another look at the big trendline we’ve been watching in the Dow …

Again, this line holds right at the 10% correction mark. And we’ve now bounced more than 700 dow points.

As I’ve said, it’s easy to get sucked into the daily narratives in the financial media, and it’s especially easy and dangerous (to your net worth) when stocks are declining. They tend to influence people to sell, when they should be buying.

And as someone that has been involved in markets more than 20 years, I can tell you that it’s also very dangerous to let political views influence your perspective on markets and investing. And I suspect we are seeing that mistake made in this environment (by pros and amateurs alike).

If you need help with your shopping list of stocks to buy on this dip, join me in my Billionaire’s Portfolio. We follow the world’s bests billionaire investors into their favorite stocks. Click here to learn more.

Yesterday we looked at this big trendline support in stocks (the yellow line).

We had a good bounce today, but experience tells me that we will make a run at that trendline, and things will look a little messy before we bottom.

We still have seven trading days before the mid-term elections. A stock market in correction is not as easy to promote as one at record highs (as we had just earlier this month). With that, I suspect there are plenty of interests (China among them) to keep the pressure on stocks in hopes of dividing U.S. Congress come November 6th.

When the dust clears from the elections, market folks will realize that stocks are incredibly cheap at 15 times next year’s earnings estimates, in an economy growing better than 3%.

On that note, we have our first look at third quarter GDP tomorrow. The market is looking for 3.6% growth, which would give us 3.22% annualized growth averaged over the past four quarters. That would be the best growth since 2006.

If you need help with your shopping list of stocks to buy on this dip, join me in my Billionaire’s Portfolio. We follow the world’s bests billionaire investors into their favorite stocks. Click here to learn more.

Since stocks dipped last week, I’ve heard the chatter (again) about how a 3% 10-year note has suddenly created a high appetite for Treasurys over stocks (i.e. people are selling stocks in favor of capturing that whopping 3% yield).

But in this post-crisis environment, a rise toward 3% promotes the exact opposite behavior. If you are willing to lend for 10-years locked in at a paltry rate, you are forgoing what is almost certainly going to be a higher rate decade than the past decade. If you need to exit, you’re going to find the price of your bonds (very likely) dramatically lower down the road.

Coming out of a zero-interest rate world, bond prices are going lower/not higher. Here’s the chart of the 10-year Treasury note (price). You can see we’ve now broken the three and a half decade bull market in bonds (yields go up, as bond prices go down) …

stocks

Bottom line: The bond market is the high risk-low reward investment in this environment. And there continues to be plenty of fuel for stock prices as money exits bonds.