|

January 7, 5:00 pm EST

The Fed sent a message to markets on Friday that they will pause on rates hikes, if not stand ready to act (i.e. cut rates or stop shrinking the balance sheet), unless market conditions improve.

With that support, stocks continue to rebound. But as the market focus is on stocks, the quiet big mover in the coming months might be commodities.

Over the weekend, the President confirmed that the $5 billion+ border wall would be made of steel — produced by U.S. steel companies. Add to that, it’s fair to expect that the next item on the Trumponomics agenda, will be a big trillion-dollar infrastructure spend (an initiative believed to be supported by both parties in Congress).

Trump has also threatened to move forward with the wall under an executive order, citing national security. With that, the execution on the wall, regardless of the state of negotiations on Capitol Hill should be coming sooner rather than later.

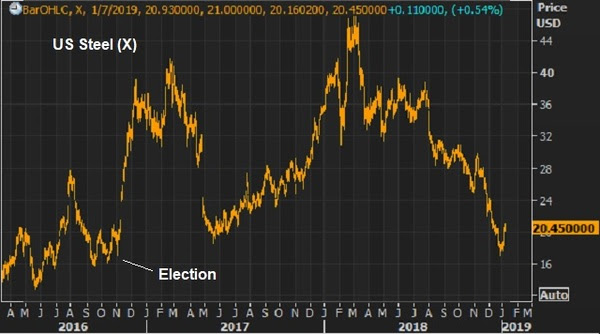

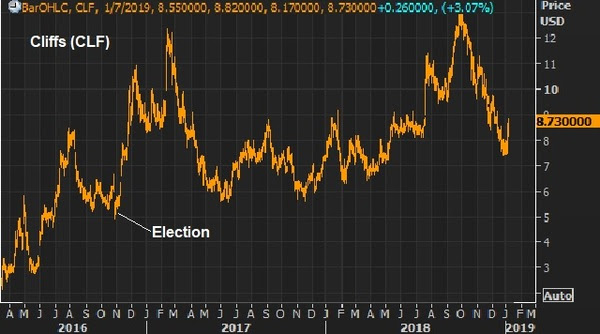

Let’s take a look today at a few domestic steel companies that should benefit.

Nucor Corp (NUE)

Nucor corp is the largest steel producer in the United States.

As you can see, these stocks all benefited early on (post election) on the prospects of Trump’s America First economic plan. But, like the broader market, these stocks are all well off of the 2018 highs now — driven by the intensified trade dispute with China over the past year, the uptick in global economic risks, and the concern over Trumponomics policy execution with a split Congress. They look very, very cheap considering the outlook for domestic steel demand.

Disclosure: We are long Cliffs (CLF) in our Billionaire’s Portfolio.

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

June 29, 5:00 pm EST

Last week, we talked a lot about oil, as OPEC was meeting to deliberate on the status of their agreement to cut production.

While oil prices have been rising aggressively over the past year, the markets haven’t been paying a lot of attention — distracted by Trump watching.

But then Trump put it on the front burner, with another jab at OPEC on Twitter. And the media and Wall Street began trying to deduce the OPEC outcome. In the end, they misinterpreted. OPEC’s agreement to go from overcutting to complyingwith the initial levels of production cuts, means they are still cutting.

So, the market is still undersupplied in a world where demand has proven to be underestimated. That’s a formula for higher prices.

That’s what we’ve had for the past year, and that’s what we’ve gotten since OPEC’s official statement on Friday. In my note last Friday, I said “the lack of enough action from OPEC may serve as a catalyst to push oil much higher from here. That, of course, serves OPEC’s interests.”

Oil prices have exploded! We’ve seen a $10 pop since Friday morning. That’s 15% in a week. And I suspect it’s going to keep going.

Remember, we’ve talked about the prospects for $100 oil this year. Leigh Goehring, one of the best research-driven commodities investors on the planet has been telling us that since last year. And he’s looking spot-on at the moment.

Bottom line: This script is precisely what we’ve been talking about, here in my daily Pro Perspectives note, since the price of oil was in the $40s. We’ve talked about the prospects for a return to $80 oil, and maybe even as high as $100 oil. And it looks more and more possible, given the surging demand and the supply shortfall.

How can you play it. On this thesis for oil, in my Billionaire’s Portfolio, we added SPDR Oil and Gas ETF (symbol XOP) and Phillips 66 (symbol PSX) back when oil prices were deeply depressed (in 2016). We followed the activism of policymakers (both central banks and OPEC). And in the case of PSX, we also followed Warren Buffett.

Both are up big, but have a lot more room to run. Oil and gas stocks (which comprise the XOP) have yet to reflect the supply shortfall in the oil market, much less the booming demand that is coming from an improving global economy (which many have underestimated).

If you haven’t joined the Billionaire’s Portfolio, where you can look over my shoulder and follow my hand selected 20-stock portfolio of the best billionaire owned and influenced stocks, you can join me here.

June 20, 5:00 pm EST

We’ve talked about the case for much higher oil prices since I started writing this daily note back in January of 2016. And we’ve since had a triple off of the February 2016 bottom.

The crash in oil prices from 2014 to 2016 was induced by OPEC as an effort to crush the competitive U.S. shale industry. While they nearly succeeded, these oil producing countries nearly killed their own economies in the process. So, in effort to drive oil prices higher, to salvage oil revenues, they had to flip the switch in late 2016, cutting production for the first time since 2008. And they did so, in a market that was already undersupplied. And in a world where demand has been underestimated, and growing.

So now, we’ve had this big recovery – nearly a round trip back to those 2014 levels.

The problem? The oil price crash was a threat to the global economy, as bankruptcies were lining up and deflationary forces were returning in the global economy. But now, current oil prices (and higher) are threatening to the recovery too, specifically the economic gains from fiscal stimulus.

And that’s on the wrong side of Trump. So, we’re seeing pressure on OPEC from the White House.

Will OPEC comply?

They are meeting now to determine whether or not they stick with current policy, or make an increase to production.

The expectations have been set for an increase. But there is dissension in the ranks at OPEC. If they surprise markets and maintain current output (i.e. no increase), we could see oil move much higher, and quickly. That would throw a wrench in almost everything. Remember, Trump’s tough positioning has a lot to do with the leverage he gets from a strong economy. $100 oil would threaten the economic outlook, and change the face of trade negotiations and the geopolitical environment.

We will likely hear leaks on Friday and probably hear a decision from OPEC on Saturday.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click her

November 24, 2017, 12:00 pm EST

As we head into the Thanksgiving day weekend, let’s talk about oil and Saudi Arabia.

As we head into the Thanksgiving day weekend, let’s talk about oil and Saudi Arabia.

On Thanksgiving night three years ago oil was trading around $73, when the Saudis blocked a vote on an OPEC production cut. Oil dropped 10% that night, and that set off a massive oil price bust that ultimately bottomed out early last year at $26.

The goal of the Saudis was to put the emerging, competitive U.S. shale industry out of business–to force oil prices lower so that these shale companies couldn’t product profitably. The plan: They go away, and Saudi Arabia retains its power on global oil. It nearly worked. Shale companies started dropping like flies, with more than 100 bankruptcies between 2015 and 2016.

But cheap oil had broader implications for the global economy, following the Great Recession. It exposed the global banks that had lent the shale industry hundreds of billions of dollars.

Additionally, collapsing oil prices directly weighed on inflation measures and the inflation expectations. That was bad news for the central banks that had committed trillions of dollars to avert a deflationary spiral and promote a normalization of inflation. High inflation is bad. Deflation is worse. Once a deflationary mindset takes hold, it feeds into more deflation. Central banks can raise rates to kill inflation. They have few tools to fight deflation (especially after the financial crisis).

So cheap oil became bad news for the fragile global economic recovery. With that, central banks stepped in early last year and responded with coordinated easing (which included direct asset purchases, which likely included outright oil and oil-related ETFs). Oil bottomed the day the Bank of Japan intervened in the currency market, and prices jumped 50% in a month as other major central banks followed with intervention.

Now, the other piece of this story: cheap oil damaged the shale industry and the global economy, but it also damaged the same folks that set the collapse into motion–Saudi Arabia and other oil producing countries. These countries, which are heavily reliant on oil revenues, have seen their budget deficits balloon. So, with all of the above in mind, in November of last year, the oil producing countries (led by Saudi Arabia) reversed course on their plan, by promising the first production cuts since 2008.

Oil prices have now recovered to the mid-$50s. And since OPEC announced production cuts last year at this time, U.S. petroleum supply has drawn down 5%. Meanwhile, global demand is running far hotter than forecasts of last year. Yet, OPEC is extending their production cuts into this market and may get even bolder next week at their November meeting. Why? Because now it suits them. Remember, Saudi Arabia’s next king has been cleaning house over the past two weeks, in the process of seizing hundreds of billions of dollars from his political foes. Higher oil prices help his efforts to reshape the Saudi economy.

As liquidity dries up into the end of year and holidays, we may see oil find its way back up toward those November 2014 levels (low $70s)–where the whole price-bust debacle started.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

November 23, 2017, 7:00 pm EST

Yesterday we talked about the comeback underway in Wal-Mart and the steps it has made to challenge Amazon, and to challenge the idea that Amazon will crush everyone.

Yesterday we talked about the comeback underway in Wal-Mart and the steps it has made to challenge Amazon, and to challenge the idea that Amazon will crush everyone.

It’s beginning to look like the “decline of the retail store” may have bottomed too.

And it so happens that it may have bottomed precisely when a new ETF launched to capitalize on that story. ProShares launched it yesterday, and that is the name of it –ProShares Decline Of The Retail Store ETF. It gives you short exposure to bricks and mortar retailers.

It’s off to a bad start–down 3% in the first day of trading.

For retail, the week started with a big earnings beat for Advance Auto Parts (the stock was up as much as 20% on Tuesday). Then it was Wal-Mart. And today we had earnings beats in Foot Locker and Abercrombie and Fitch.

With this, while the Dow and S&P 500 were down on the day, the small-cap (Russell 2000) was up nicely. Here’s why …

As bad as retail has been, the energy sector remains the worst performing for the year–down 11% year-to-date as a sector and the only sector in the red. This, as oil has reversed from down 22% on the year, to up around 5%, with a very bullish outlook.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

|

All eyes continue to be on U.S. stocks. But the bigger opportunities are elsewhere.

All eyes continue to be on U.S. stocks. But the bigger opportunities are elsewhere.

|

|

|

|

|

|

By Bryan Rich

October 12, 2017, 7:30 pm EST Invest Alongside Billionaires For $297/Qtr

For much of the summer, while the world has been obsessed with Trump tweets, we’ve talked about the sharp but under-acknowledged move in copper and the message it was sending about the global economy and China (the biggest consumer of commodities), specifically. As I’ve said, people should Stop Watching Trump And Start Watching Copper.

Why copper? It is often an early indicator of economic cycles. People love to say copper ‘has a Ph.D. in economics’ because it tends to top early at economic peaks and bottom early at economic troughs. And it tends to lead a bull market in broader commodities.

Well, copper bottomed on January 15. Fast forward to today; the most important industrial metal in the world is up 24% on the year and sniffing back toward three-year highs. While the world continues to focus on Washington drama, this continues to be the proverbial “bell” ringing to signal a pop in economic growth is coming, and a big run for commodities investors is ripe for the taking.

With that in mind, we’ve talked in recent days again about the research from the top minds in commodities investing, Leigh Goehring and Adam Rozencwajg (managers of the commodities funds, ticker GRHIX and GRHAX). We know they like oil. In fact they think we see triple-digit oil prices by early next year.

They love the commodities trade in general. They have one of the most compelling charts I’ve seen in my 20-year career, to support the view that there is a generational bull breaking lose in commodities.

Stocks minted billionaires in the 1980s. Currencies minted billionaires in the 1990s. Tech and housing (bust) minted billionaires in the early 2000s. Then it was equity activism (stocks). The next opportunity looks like commodities.

In this chart below you can see, as Goehring and Rozencwajg say, commodities are as cheap today as they have ever been. “Only in the depths of the Great Depression and at the end of the dying Bretton Woods Gold Exchange Standard did commodities reach this level of undervaluation relative to equities.”

With this, they say, for those that can block out the noise, “there is a proverbial fortune to be made if they invest today.”

Here’s an excerpt from their most recent investor letter on their work on the stocks to commodities valuation:

“When commodities are this cheap relative to stocks, the returns accruing to commodity investors have been spectacular. For example, had an investor bought the Goldman Sachs Commodity Index (or something equivalent) in 1970, by 1974 he would have compounded his money at 50% per year. From 1970 to 1980 commodities compounded anually in price by 20%. If the same investor had bought commodities in 2000, he would have also compounded his money at 20% for the next ten years–especially attractive considering the broad stock market indicies returned nothing over the same period.”

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

September 18, 2017, 4:30 pm EST Invest Alongside Billionaires For $297/Qtr

As I said on Friday, people continue to look for what could bust the economy from here, and are missing out on what looks like the early stages of a boom.

We constantly hear about how the fundamentals don’t support the move in stocks. Yet, we’ve looked at plenty of fundamental reasons to believe that view (the gloom view) just doesn’t match the facts.

Remember, the two primary sources that carry the megahorn to feed the public’s appetite for market information both live in economic depression, relative to the pre-crisis days. That’s 1) traditional media, and 2) Wall Street.

As we know, the traditional media business, has been made more and more obsolete. And both the media, and Wall Street, continue to suffer from what I call “bubble bias.” Not the bubble of excess, but the bubble surrounding them that prevents them from understanding the real world and the real economy.

As I’ve said before, the Wall Street bubble for a very long time was a fat and happy one. But the for the past ten years, they came to the realization that Wall Street cash cow wasn’t going to return to the glory days. And their buddies weren’t getting their jobs back. And they’ve had market and economic crash goggles on ever since. Every data point they look at, every news item they see, every chart they study, seems to be viewed through the lens of “crash goggles.” Their bubble has been and continues to be dark.

Also, when we hear all of the messaging, we have to remember that many of the “veterans” on the trading and the news desks have no career or real-world experience prior to the great recession. Those in the low to mid 30s only know the horrors of the financial crisis and the global central bank sponsored economic world that we continue to live in today. What is viewed as a black swan event for the average person, is viewed as a high probability event for them. And why shouldn’t it? They’ve seen the near collapse of the global economy and all of the calamity that has followed. Everything else looks quite possible!

Still, as I’ve said, if you awoke today from a decade-long slumber, and I told you that unemployment was under 5%, inflation was ultra-low, gas was $2.60, mortgage rates were under 4%, you could finance a new car for 2% and the stock market was at record highs, you would probably say, 1) that makes sense (for stocks), and 2) things must be going really well! Add to that, what we discussed on Friday: household net worth is at record highs, credit growth is at record highs and credit worthiness is at record highs.

We had nearly all of the same conditions a year ago. And I wrote precisely the same thing in one of my August Pro Perspective pieces. Stocks are up 17% since.

And now we can add to this mix: We have fiscal stimulus, which I think (for the reasons we’ve discussed over past weeks) is coming closer to fruition.

Join our Billionaire’s Portfolio today to get your portfolio in line with the most influential investors in the world, and hear more of my actionable political, economic and market analysis. Click here to learn more.

February 16, 2017, 6:30pm EST

Stocks were down a bit today, for the first day in the past six days. Yields were lower, following two days of Janet Yellen on Capitol Hill. Gold was higher on the day. And the dollar was lower.

Of the market action of the day, the dollar and yields are the most interesting. The freshly confirmed Treasury Secretary, Steven Mnuchin, held a call with Japan’s Finance Minister last night, early morning Japan time.

What did USD/JPY do? It went down (lower dollar, stronger yen). Just as it did the week leading up to the visit between President Trump and Japan’s Prime Minister Abe.

Remember, the yen has been pulled into the fray on Trump’s tough talk on trade fairness and currency manipulation. The subject has cooled a bit, but with the new Treasury Secretary now at his post, the world will be looking for the official view on the dollar.

As I said before, I think the remarks about currency manipulation are (or should be) squarely directed toward China. And I suspect Abe may have conveyed to the president, in their round of golf, that Japan’s QE is quite helpful to the U.S. economy and policy efforts, even if it comes with a weaker yen (stronger dollar). Among many things, Japan’s policy on keeping its ten-year yield pegged at zero (which is stealth unlimited QE) helps put a lid on U.S. market interest rates. And that keeps the U.S. housing market recovery going, consumer credit going and U.S. stocks climbing, and that all fuels consumer confidence.

Yesterday we talked about the fourth quarter portfolio disclosures from the world’s biggest investors. With that in mind, let’s talk about the porfolio of the man that’s best position to benefit from the Trump administration: the legendary billionaire investor, Carl Icahn.

Icahn was an early supporter for Trump. He was an advisor throughout the campaign and helped shape policy plans for the president.

What has been the sore spot for Icahn’s underperforming portfolio in recent years? Energy. It has been heavily weighted in his portfolio the past two years and no surprise, it’s contributed to steep declines in the value of his portfolio over the past three years. Icahn’s portfolio is volatile, but over time it has produced the best long run return (spanning five decades) of anyone alive, including Buffett. And he’s worth $17 billion as a result.

Here’s a look at what I mean: In 2009 he returned +33%, +15% in 2010, +35% in 2011, +20% in 2012 and +31% in 2013. That’s quite a run, but he’s given a lot back–down 7% in 2014, down 20% in 2015 and down 20% last year.

Even with this drawdown, Icahn doesn’t see his energy stakes as bad investments. Rather, he thinks his stocks have been unfairly harmed by reckless regulation. And he’s been fighting it.

He penned a letter to the EPA last year saying its policies on renewable energy credits are bankrupting the oil refinery business and destroying small and midsized oil refiners.

And now that activism is positioned to pay off handsomely.

The new Trump appointee to run the EPA was first vetted by Icahn–it’s an incoming EPA chief that was suing the EPA in his role as Oklahoma attorney general. Safe to assume he’ll be friendly to energy, which will be friendly to Icahn’s portfolio.

And as we know, Icahn has since been appointed as an advisor to the

president on REGULATION.

To get peek inside the portfolio of Trump’s key advisor, join me our Billionaire’s Portfolio. When you do, I’ll send you my special report with all of the details on Icahn, and where he’s investing his multibillion-dollar fortune to take advantage of Trump policies.

Click here to join now.

Our Billionaire’s Portfolio is the way investing should be. Its top-shelf intelligence, in an easy to understand format, delivered to your inbox. If you can read a weekly note, and push a button, this service is for you whether you’re a novice investor or a Wall Street titan. This is your opportunity to align your portfolio with the world’s smartest and most powerful investors. To learn from the best and ride their coattails to success.

You get access to the full gamut of billionaire intelligence. Join us now, get this special report, and get your portfolio in line with the richest, most powerful investors in the world.