|

|

|

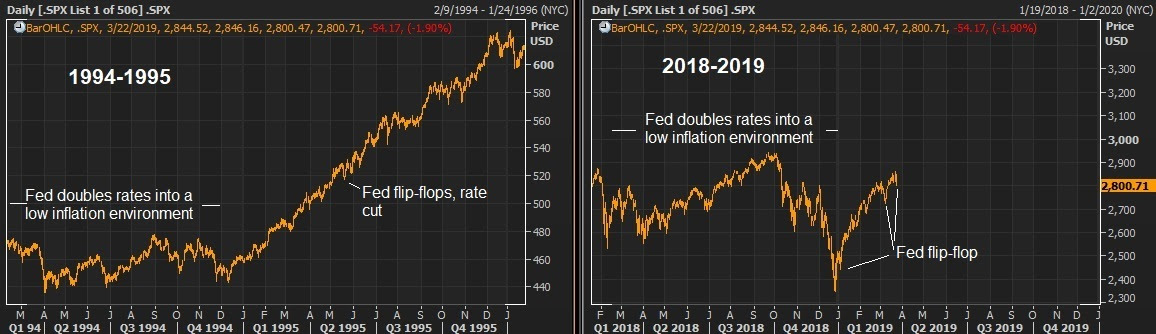

April 11, 5:00 pm EST As we came into the week, the economic, political and corporate calendar was relative light. With that, I suspected markets would be relatively quiet. Of course we have had an ECB meeting and minutes from the Fed. Often, these would be market moving events. Not this week. As we discussed yesterday, we clearly know where they stand. So, what’s next? Earnings. First quarter earnings season kicks off next week. We’ll hear from the major banks. Earnings will be the catalyst for where stocks go from here – and banks will set the tone. The building theme has been “earnings recession.” After 20%+ earnings growth in 2018, following a historic corporate tax cut, anyone would expect earnings growth to be less hot than last year. Some were even predicting that the hot numbers of last year would be a peak in earnings growth. After all, under ordinary circumstances (in a stable economic environment) we’re very unlikely to see the U.S. stock market grow earnings by excess of 20%. That’s not much of a story . But the media loved the shock value of the phrase “peak earnings” last year, and ran it in headlines, conveniently excluding the word “growth.” Peak earnings is very different than peak earnings growth. Still, the broad market sentiment on future corporate earnings eroded through the end of 2018, and has continued to erode through 2019. And both Wall Street and corporate America are more than happy to ride the coattails of lower sentiment by lowering the expectations bar on earnings. When sentiment is leaning that way already, there is little-to-no penalty for lowering the bar. That just sets the table for positive surprises. They did it for Q4 2018 earnings. And they beat expectations. And they have set the table for positive surprises for Q1 2019 earnings. Just how low has the bar been set for Q1? Before stocks unraveled in December, Wall Street was looking for 8.3% earnings growth for 2019. Now they are looking for less than half that. Moreover, they have projected earnings to contract in Q1 compared to the same period a year ago (i.e. at least a short-term peak in earnings).

Will they be right?

Well, the Atlanta Fed’s real-time model for estimating GDP has Q1 GDP coming in at 2.3%. The economy added on average 173,000 jobs a month over the first quarter. Both manufacturing and services PMIs expanded in the quarter, and stocks fully recovered the losses from December. That’s a formula for earnings growth, no contraction.

|

|

If you haven’t signed up for my Billionaire’s Portfolio, don’t delay … we’ve just had another big exit in our portfolio, and we’ve replaced it with the favorite stock of the most revered investor in corporate America — it’s a stock with double potential. Join now and get your risk free access by signing up here. |

|

July 23, 5:00 pm EST

We have a big earnings week. The tech giants report, along with about a third of the S&P 500. And we get our first look at Q2 GDP.

As we’ve stepped through the year, we’ve had a price correction in stocks, following nearly a decade of central bank policies that propped up stocks. This correction made sense, considering central banks were finally able to make the hand-off to a U.S. led administration that had the will and appetite (and alignment in Congress) to relax fiscal constraints and force the structural reform necessary to promote an economic boom.

From there, for stocks, it became a “prove-it to me” market. Let’s see evidence of this “hand-off” is working — evidence the fiscal stimulus is working. That came in the form of first quarter earnings. This showed us clear benefits of the corporate tax cut. The earnings were hot, and stocks began a recovery.

The next steps, as fiscal stimulus works through the economy, we’ve needed to see that the uptick in sentiment (from the pro-growth policies) is translating into better demand and economic activity. So, with Q2 earnings we should start seeing better revenue growth, companies investing and hiring. And we should see positive surprises beginning to show up in the economic data.

We’re getting it. Almost nine out of ten companies reporting thus far have beat (lofty) earnings expectations. And about eight out of ten have beat on revenues. This week will be important, to solidify that picture. And though many of the economists all along the way of the past year didn’t see big economic growth coming, it has been steadily building since Trump was elected, and the Q2 number should push us to over 3% annual growth (averaging that past four quarters).

Now, let’s talk about the big mover of the day: interest rates. The 10-year yield traded to 2.96% today, closing in on 3% again.

We’ve discussed, many times, the role that Japan continues to play in our interest rate market. Despite 7 hikes by the Fed from the zero-interest-rate-era, our 10 year yield has barely budged. That’s, in large part, thanks to the Bank of Japan.

As I’ve said in the past, “Japan’s policy on pegging its 10-year yield at zero has been the anchor on global interest rates. Forcing their benchmark government bond yield back to zero, in a world where there has been upward pressure on interest rates, has meant that they can, and will, buy unlimited amounts of JGBs to get the job done. That equates to unlimited QE. When they finally signal a change to that policy, that’s when rates will finally move.”

With that in mind, there were reports over the weekend that the Bank of Japan may indeed signal a change in that “yield curve control” policy at their meeting next week. And global rates have been moving!

April 23, 6:00 pm EST

We’re getting into the heart of Q1 earnings now, with about a quarter of the companies in the S&P 500 now in, and many more reporting this week. And we’ll get the first look at Q1 GDP this Friday.

Remember, as we went through the price correction in stocks, we’ve been waiting for the data to “prove it” to the market that fiscal stimulus and structural reform are indeed fueling a return to trend growth.

On that note, the performance of companies in Q1 have NOT disappointed. As of Friday, 80% of the S&P 500 companies that have reported have beat earnings estimates. And 72% have beat revenue estimates.

Now we have the build up to the big Q1 GDP number at the end of this week. We were already heading into the first quarter, with the economy growing at better than 3% for the second half of 2017. And then the fire was fed with the tax bill.

So what are the expectations going into the GDP report?

The Atlanta Fed attempts to mimic the model used by the BEA on their GDP forecast. They are looking for 2% for Q1 growth. And as you can see in their chart above, the forecasted number has been on a dramatic slide as we’ve seen more and more economic data through the period. More importantly, Reuters has the consensus view of economists at 2%.

The New York Fed’s model is predicting 2.9% growth (closer to that important trend growth level).

As with earnings, a low bar to hop over tends to be very good for stocks. And at a 2% consensus, we’re setting up for a positive surprise on GDP.

As we’ve discussed, despite the move higher in global rates over the past week, and the coming break of the 3% barrier in the 10-year yield, it will be hard to dispute the signal of economic strength and robustness from the combination of a huge earnings season and a positive surprise in GDP. If we get it, that should kick the stock market recovery into another gear.

February 19, 8:00 pm EST

With the big decline and wild swings in the stock market, earnings season has gotten little attention.

We’ve now heard from 80% of the companies in the S&P 500 on Q4. According to FactSet, 75% of the companies have beat on earnings. And 78% have had positive revenue surprises.

Now, earnings estimates are made to be broken. And they tend to be beaten at a rate of about 70% of the time. But the same cannot be said for revenues. This has been a key missing piece in the economic recovery. Companies have been cutting costs, refinancing and trimming headcount, all in an effort to manufacture margins and profitability. But revenues, the true gauge of business activity and demand, had been dead for the better part of the past decade.

It was just last year that we finally saw some decent revenue growth coming in from the earnings reports. And this most recent quarter, revenue growth is running at the hottest rate since FactSet has been keeping records. That’s a very good sign for the economic outlook.

And corporate earnings are running 15.2% higher than the same period the year prior. That’s the hottest earnings growth we’ve seen since 2011. More importantly, that’s four percentage points higher than analysts were projecting at the end of the year–with knowledge of the tax cut legislation.

With that said, remember, just last Friday, we had a moment during the day when the forward P/E on the S&P 500 hit 16.2. But if the fourth quarter is any indication, those forward earnings (estimates) will likely get ratcheted UP over the coming quarters, but will still undershoot. That will keep downward pressure on the P/E. Stocks are cheap.

If you are hunting for the right stocks to buy, join me in my Billionaire’s Portfolio. We have a roster of 20 billionaire-owned stocks that are positioned to be among the biggest winners as the market recovers. You can add these stocks at a nice discount to where they were trading just a week ago.

February 13, 2017, 3:30pm EST Invest Alongside Billionaires For $297/Qtr

First, as we know, the most powerful underlying force for stocks right now is prospects of a massive corporate tax cut, deregulation, a huge infrastructure spend and trillions of dollars of corporate repatriation coming. But quietly, among all of the Trump attention, earnings are also driving stocks. More than 70% of S&P 500 companies have reported. About 2/3rds of the companies have beat Wall Street estimates. And most importantly, earnings in Q4 have grown at 3.1% year-over-year. That’s the first consecutive positive growth reading since Q4 2014/ Q1 2015.

Meanwhile, yields have remained quiet. And oil prices have remained quiet. That’s positive for stocks. Take a look at the graphic below …

You can see, stocks and most commodities continue to rise on the growth outlook. Yields and energy should be rising too. But the 10 year yield has barely budged all year — same for oil. Of course, higher rates, too fast, are a countervailing force to the pro-growth policies. Same can be said for higher oil too fast. With that, both are adding more “fuel” to stocks.

On the rate front, we’ll hear from Janet Yellen this week, as she gives prepared remarks on the economy to Congress, and takes questions.

She’s been a communications disaster for the Fed. Most recently, following the Fed’s December rate hike, she backtracked on her comments made a few months prior, when she said the Fed would let the economy run hot. She denied that in December. Still, the 10-year yield is about 10 basis points lower than where it closed following that December press conference. I wouldn’t be surprised to see a more dovish tone from Yellen this time around, in effort to walk market rates a little lower, to take the pressure off of the Fed and to continue stimulating optimism about the economy.

On Friday we looked at four important charts for markets as we head into this week: the dollar/yen exchange rate, the Nikkei (Japanese stocks), the DAX (German Stocks), and the Shanghai Composite (Chinese stocks).

With U.S. stocks printing new record highs by the day, these three stock markets are ready to make a big catch-up run. It’s just a matter of when. And I argued that a positive tone coming from the meeting of U.S. and Japanese leadership, under the scrutiny of trade tensions, could be the greenlight to get these markets going. That includes a stronger dollar vs. the yen. All are moving in the right direction today.

On the China front, we looked at this chart on Friday.

As I said, “Copper has made a run (up 10% ytd). That typically correlates well with expectations of global growth. Global growth is typically good for China. Of course, they are in the crosshairs of Trump’s fair trade movement, but if you think there’s a chance that more fair trade terms can be a win for the U.S. and a win for China, then Chinese stocks are a bargain here.”

Copper is surged again today on a supply disruption and has technically broken out.

This should continue to spark a move in the Chinese stock market.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.

February 9, 2017, 3:00pm EST Invest Alongside Billionaires For $297/Qtr

Stocks are hitting new record highs today. That includes the Dow, the S&P 500 and the Nasdaq.

We’ve now seen about 60% of the earnings for Q4, and earnings are very good. As we’ve discussed, earnings guidance and consensus views are made to be beaten. Factset says that, on average, about 67% of S&P 500 companies beat the consensus view on earnings. For Q4, that number, as of last Friday, was 65%.

More importantly, the earnings growth rate for Q4 is +4.6% thus far. That’s better than the 3.1% that was predicted, coming into the earnings season. And that’s the first two consecutive quarters of year-over-year positive EPS growth in a couple of years.

So we have positive earnings surprises driving stocks higher. And finally, revenue growth is coming. After six consecutive quarters of revenue contraction, earnings for U.S. companies had a second consecutive quarter of growth. And the quarters ahead should be much better.

Clearly, in the weak growth environment, the focus has clearly been cutting costs, refinancing debt, selling non-core assets, and buying back shares. That’s all a recipe for juicing EPS, even though revenue growth is sluggish, if existent.

So for all of the people that are constantly hand wringing about the levels of the stock market, ask them this: What happens when you take these companies that are growing earnings by optimizing margins in a 1% growth world, and you give them 3%-4% economic growth? Earnings go up. What happens when you take a profitable company and cut the tax burden by 15 to 20 percentage points? Earnings go up.

When earnings go up, price to earnings goes down. And valuations can become very, very cheap.

We have companies that have been forced to streamline to survive. And now we’re in the early days of a regime shift, where tax cuts will work for them, deregulation will work for them, and a big infrastructure spend will pop demand, to actually fuel some revenue growth.

Below is a nice chart from Yardeni. You can see the flattish revenue growth, but earnings divergence over the past five years.

On the right hand axis, next year’s earnings on the S&P 500 are expected around $133. That doesn’t take into account the impact of a corporate tax cut, which Standard & Poors research has suggested could bump that number up to the mid $150s ($1.31 added for every 1% cut in the corporate tax rate). That would dramatically widen the revenue, earnings divergence — or make the closing of this gap that much more aggressive.

For help building a high potential portfolio for 2017, follow me in our Billionaire’s Portfolio, where you look over my shoulder as I follow the world’s best investors into their best stocks. Our portfolio more than doubled the return of the S&P 500 in 2016. You can join me here and get positioned for a big 2017.