|

|

January 14, 5:00 pm EST Meaningful fourth quarter earnings kick off this week with the big banks. We heard from Citigroup this morning. They beat on earnings but on lower than expected revenues. The stock finished UP over 4%. We get JPMorgan and Wells Fargo Q4 earnings tomorrow before the open. Bank of America and Goldman Sachs will report on Wednesday. Remember, the turning point for stocks in December started with a call-out to the major banks by the U.S. Treasury Secretary. Not surprisingly, the turn in stocks was led by the banks. |

|

|

You can see the big reversal in this chart of the KBW bank index. The index is now up 16% since December 26th. With the above in mind, one of the best value investors of the past twenty years, Jeffrey Ubben, has thought the timing is finally right for major banks. He has said the U.S. banking system has the lowest risk profile “than any time in our investing lifetime.” In our Billionaire’s Portfolio, we followed him into Citigroup, the highest conviction position in his $16 billion portfolio. It’s the cheapest of the four biggest U.S.-based global money center banks. As for earnings, overall: Remember, we’re coming off of three consecutive quarters of corporate earnings that blew away very lofty Wall Street estimates — 20%+ yoy earnings growth for the first three quarters of 2018. But sliding stocks in the fourth quarter eroded sentiment, and down came earnings estimates for Q4. The market is looking for just 10% earnings growth for the fourth quarter. For 2019, they’re looking for just 7%. This all sets up for positive surprises. Positive surprises are fuel for stocks.

Join me here to get my curated portfolio of 20 stocks that I think can do multiples of what broader stocks do, coming out of this market correction environment.

|

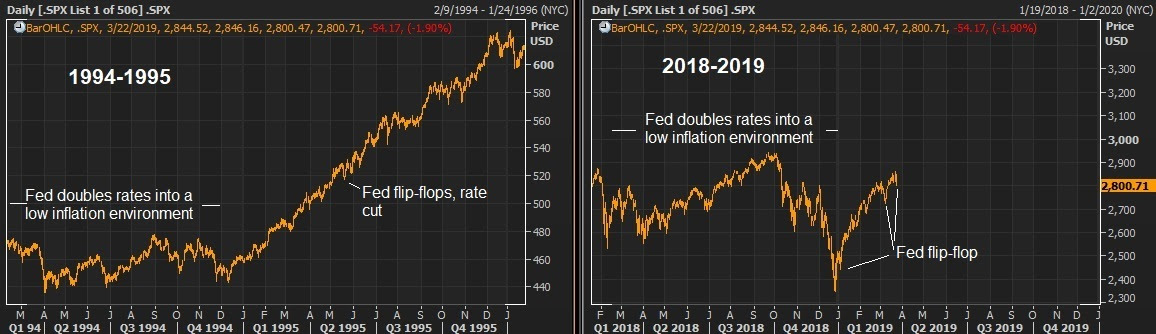

September 19, 2016, 2:00pm EST

We have two big central bank meetings this week–BOJ and the Fed. With that, as we head into the week, let’s look at a key chart.

This chart is from a St. Louis Fed blog post last year. The inflation data, however, is all up-to-date. The Fed says “the chart above shows eight series that receive a lot of attention in the context of policy.”

So according to this chart, last year, as the Fed was building into its first rate hike to move away from emergency level rates and policies, the inflation data was looking soft. The Fed was telegraphing, clearly, a September hike, though six of the eight inflation measures in the chart above were running south of their target of 2% in the middle of last year. The headline inflation number for September, their preferred date of a hike, was zero!

Of course, after markets went haywire following China’s currency devaluation in August of last year, the Fed balked and stood pat. When things calmed, in December, they made their move. And at the same meeting, they projected to hike FOUR times this year. So far it hasn’t happened. It’s been a one and done.

Moreover, as of March of this year, they took two of those projected hikes off the table, and guided lower on growth, lower on inflation and a lower rate trajectory into the future. I would argue removing two hikes from guidance was effectively easing.

But if we look at the chart above, where inflation stands now relative to the middle of last year, when they were all “bulled-up” on rates, the story doesn’t jive. By all of the inflation measures, the economy is clearly running hotter (a relative term). Five of the eight inflation measures are running ABOVE the Fed’s 2% target (the horizontal black line in the chart). Yet, aside from a few Fed hawks that have been out trying to build expectations for a rate move soon, on balance, the messaging from the Fed has been mixed at best, if not dovish.

The Bernanke-led Fed relied heavily on communication (i.e. massaging sentiment and perception) to orchestrate the recovery, but the Fed, under Yellen, has been a communications disaster.

Join us here to get all of our in-depth analysis on the bigger picture, and our carefully curated stock portfolio of the best stocks that are owned and influenced by the world’s best investors.

Gold has been a core trade for a lot of people throughout the crisis period. When Lehman failed in 2008, it shook the world, global credit froze, banks were on the verge of collapse, the global economy was on the brink of implosion – people ran into gold. Gold was a fear-of-the-unknown-outcome trade.

Then the global central banks responded with massive backstops, guarantees, and unprecedented QE programs. The world stabilized, but people ran faster into gold. Gold became a hyperinflation-fear trade.

Source: Billionaire’s Portfolio

In the chart above, you can see gold went on a tear from sub-$700 bucks to over $1,900 following the onset of global QE (led by the Fed).

Gold ran up as high as 180%. That was pricing in 41% annualized inflation at one point (as a dollar for dollar hedge). Of course, inflation didn’t comply. Still eight years after the Fed’s first round of QE (and massive global responses), we have just 13% cumulative inflation over the period.

So the gold bugs overshot in a big way.

Why? The next chart tells the story…

This chart above is the velocity of money. This is the rate at which money circulates through the economy. And you can see to the far right of the chart, it hasn’t been fast. In fact, it’s at historic lows. Banks used cheap/free money from the Fed to recapitalize, not to lend. Borrows had no appetite to borrow, because they were scarred by unemployment and overindebtedness. Bottom line: we get inflation when people are confident about their financial future, jobs, earning potential … and competing for things, buying today, thinking prices might be higher, or the widget might be gone tomorrow. It’s been the opposite for the past eight years.

So, no inflation – what does that mean for gold?

Source: Billionaire’s Portfolio

After three rounds of Fed QE, and now mass scale QE from the BOJ and the ECB, the world is still battling DE-flationary pressures. If gold surged from sub-$700 to $1,900 on Fed/QE-driven hyperinflation fears, and QE has produced little to no inflation, it’s fair to think we can return to pre-QE levels. That’s sub-$700.

We head into the weekend with stocks down 3% for the month. This follows a bad January. In fact, the stock market is working on a fifth consecutive negative month. The likelihood, however, of it finishing down for February is very low. It’s only happened 18 times since 1928. So the S&P 500 has five consecutive losing months just 1.7% of the time, historically.

gold,inflation,banks,fed,boj,ecb,rates,economy,business,finance,investing,stock market,stocks,bonds,bank of america