The betting markets have continued to widen in favor of a Trump win.

This pattern is similar across all of the top prediction platforms.

The Republicans are widely expected to win the Senate, and the betting markets are pricing in about a coin flips chance of a fully aligned government (a House win as well).

With that, small cap value stocks outperformed broader stocks today on this outlook of more business friendly, pro-growth policies.

If we look back at 2016, for those reasons, the Russell 2000 doubled the performance of the S&P in the two months following the Trump win (+17% vs. +8%).

This growing probability of a Trump win is bubbling up in a few other areas.

In media, the LA Times didn’t endorse a candidate. Nor did the Washington Post.

And Jeff Bezos just penned this opt-ed in his Washington Post …

This sounds like a mea culpa on a failed influence campaign.

We will see.

It’s a very high stakes election, with a binary outcome on policy path and governance.

On that note, I want to revisit my piece from election day in 2020.

Please take the time to watch the video at the end (foresight was 2020).

November 3, 2020

Big day. And global asset prices are soaring.

Are markets anticipating a Biden win, blue wave and, consequently, a $3 trillion slush fund coming down the pike?

Are markets anticipating a Biden win, and subsequent economic shutdown, for the purpose of forcing Congress to relent on a $3 trillion dollar “relief” package?

Are markets anticipating a Trump win, and the immediate removal of the political noose that has choked off the full reopening capacity of the U.S. economy?

Are markets simply anticipating the end of a very long period of uncertainty, which will ultimately, at minimum, give way to a recovering economy with trillions of dollars of monetary and fiscal stimulus still floating around?

Any way you look at it, the common theme is that the election represents an unlocking of the liquidity deluge from the policy response earlier this year (and possibly even adding to it).

The next question to ponder, just how much inflation is ahead?

With the Fed openly willing to sit on zero interest rates until they see inflation run sustainably north of 2%, if Biden were to come in and pile on a multi-trillion government spending program, on top of the this chart below, inflation would explode higher — and the Fed would be caught well behind, and chasing it. As we’ve discussed for a long time, you don’t want to hold cash in this environment, you want to be long asset prices.

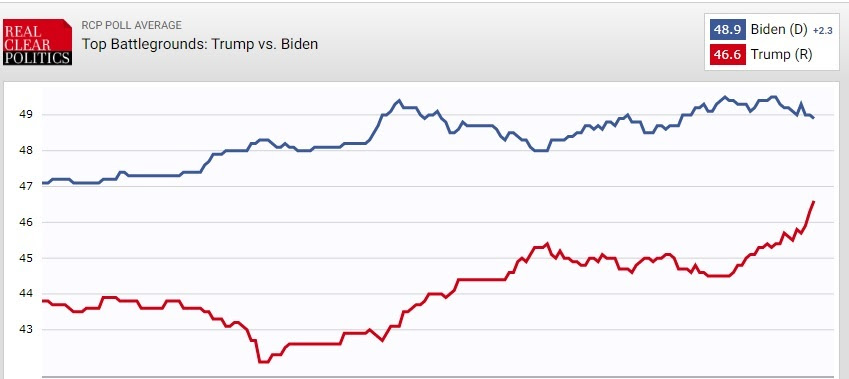

With that said, on the election outcome front, for the states that will determine the winner, the national polls have Biden up by only 2.3 points going in.

Assuming there are no surprises in Florida and Texas, a win for Trump in Pennsylvania would probably get him over the finish line. And the three pollsters that correctly predicted his win in Pennsylvania in 2016 have him winning PA again (Big Data Poll, Susquehanna, and Trafalgar).

On a final note, as we’ve discussed here in my daily notes, the stakes are extremely high in this election. China is on the doorstep of overtaking the United States as global economic superpower, and they won’t be looking to spread democracy – rather, they have a clear goal of world domination.

As we know, Trump has been a wrecking ball for the Chinese Communist Party’s grand plan. And with that, it’s safe to say they would do anything and everything to get rid of him. We’ve seen just that. On the other hand, Biden seems very likely to follow the “humble foreign policy path” that has enabled China’s ascent.

With that above in mind, maybe the most articulate description of – Trump’s role as a wrecking ball, what has taken place over the past four years and amplified in the past 10 months, and what is at stake with today’s vote – is in this speech (click here to view). It’s from a prominent NY money manager, and worth the time.