We get the August inflation report tomorrow.

As we discussed yesterday, after twelve consecutive months of falling year-over-year headline inflation, the trough might be in, for a while.

It ticked up last month. It's expected to tick up again tomorrow, to the mid-3% area.

This should be a comfortable number for the Fed, given they have short-term rates set about 200 basis points higher than headline inflation.

What about oil prices? Crude oil is up 30% since late June. This will start showing up in the headline inflation number in the coming months.

Does that mean the Fed will have to do more (more rate hikes)?

The market is pricing in less than a coin flips chance of a (final) hike next month. But we should be at the stage, when it comes to oil consumption, of "higher prices solve higher prices" (i.e. higher prices resulting in lower demand).

The consumer is getting squeezed, and $4+ gas in the near future is another major pinch.

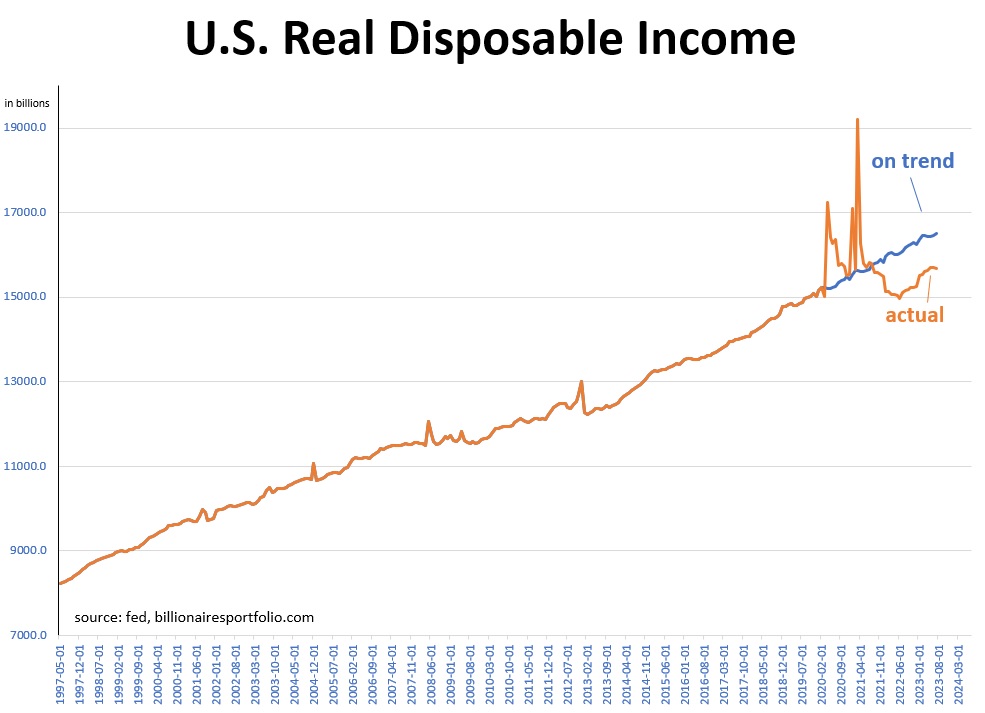

Take a look at real disposable income. Historically it has grown, throughout various cycles, on average at about the rate of real economic growth. As you can see in the chart, it's well below trend (the orange line), if we were to extrapolate out from the pre-pandemic levels.

Consumers are strapped, but government money is flowing (by the trillions).

We talked about this type of environment in my notes more than two years ago, in the midst of the building inflation: "this type of economy is not a 'feel good' economy. In an inflationary economy consumers feel like they are sprinting on a treadmill just to maintain status quo." You can see that May 2021 note here.