As we’ve discussed along the way, this is the equivalent of “skating to where the puck is going.” The price of the products we will be buying in the months ahead, will be determined (in large part) by the inputs into Chinese production.

This year-over-year change in Chinese PPI was at 26-year highs when the Fed was telling us, back in 2021, that there was no inflation.

It led on the way up (for global price pressures). And it has led on the way down.

As you can see in the chart above, the latest year-over-year change in Chinese producer prices (reported over the weekend) is still in deflationary territory (down 3% year-over-year). And that trajectory of prices for Chinese goods has proven to be a good indicator for U.S. price pressures, which, as we know, have fallen sharply from the 9% inflation of a year ago.

That said, producer prices in China have now been rising on a month-over-month basis, for two consecutive months.

Does this mean the disinflation in U.S. prices might be over, at least in the near term?

Maybe. The last headline U.S. inflation number broke a 12-month streak of falling inflation. And Wednesday’s number will likely show another uptick in price pressures from August.

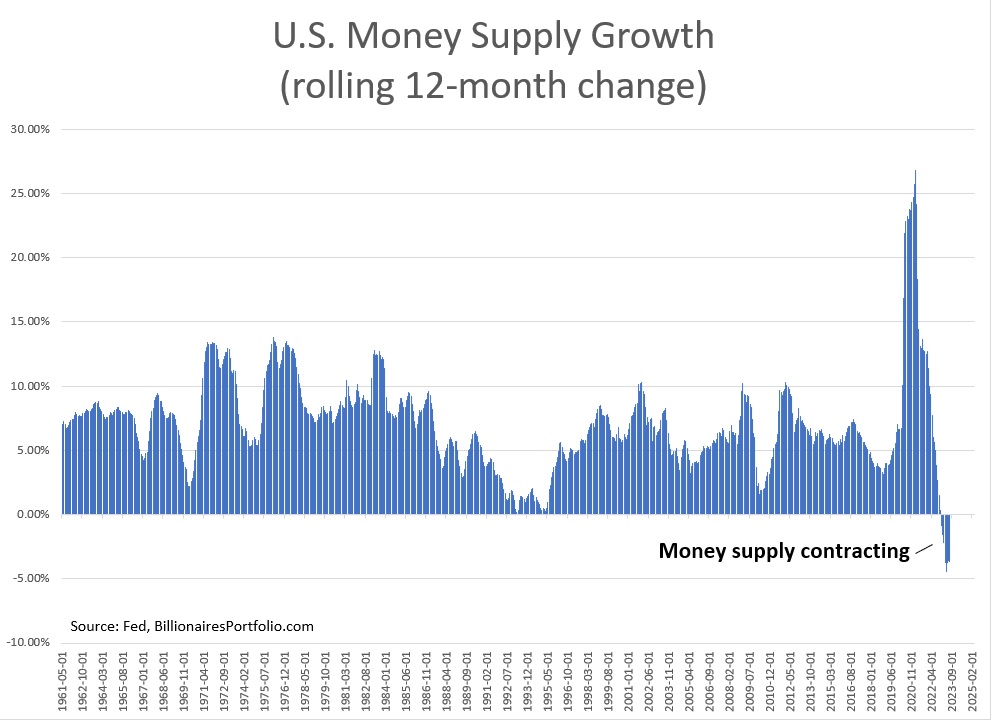

That brings us to our next chart of U.S. money supply growth…

As you can see, the aftermath of the money supply explosion has been a contraction.

And a contraction in money supply has historically been deflationary.

So, we had the inflation catalyst, which was the growth shock in money supply, from the 2020-2021 policy response to the pandemic.

We’ve had the disinflationary effect from the contraction in money supply.

But now, even though the year-over-year change in money supply remains negative (contractionary), the monthly change has been growing for three consecutive months.

A normalization in money supply growth would be a good thing.